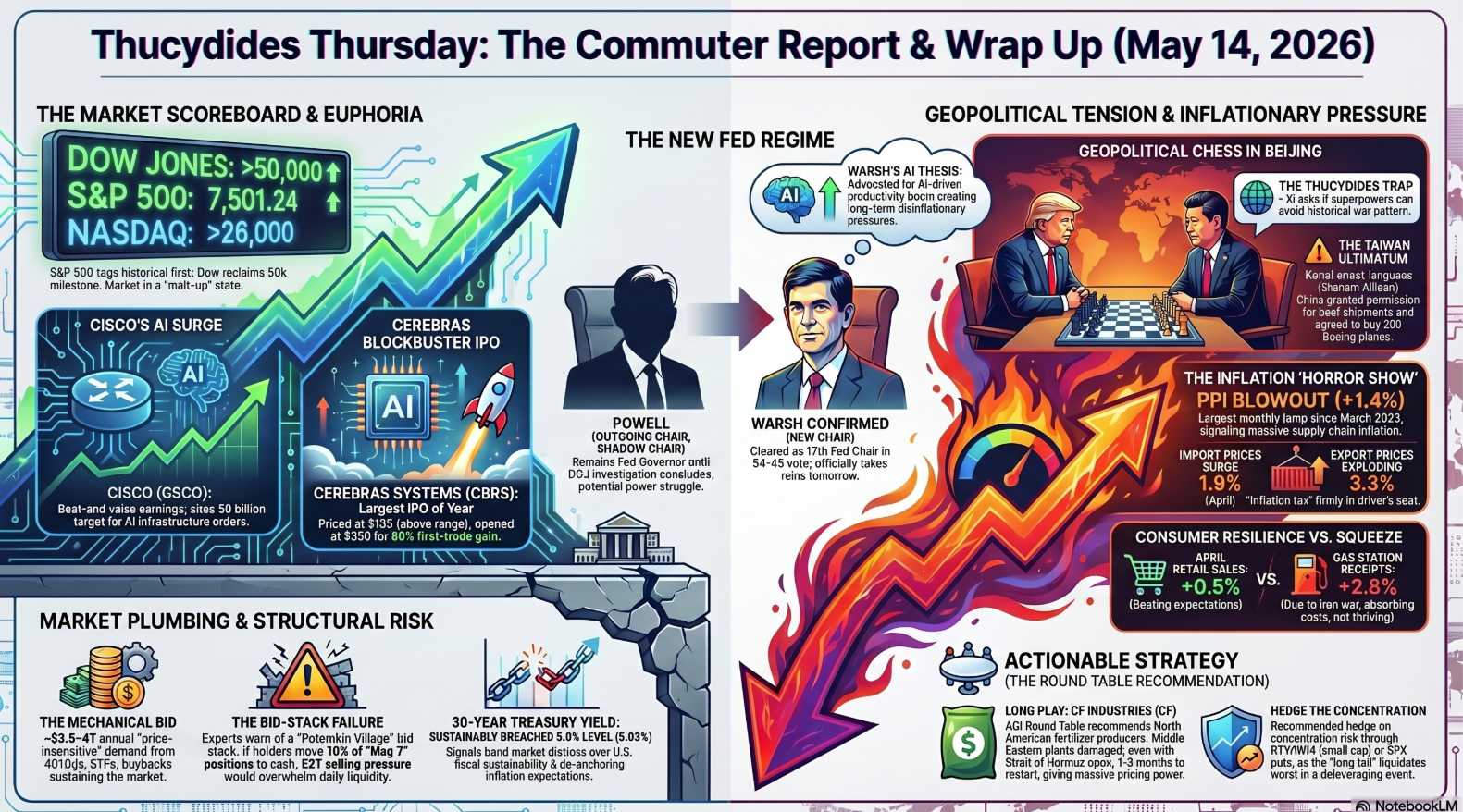

Is the market a “Potemkin Village” of liquidity?

In our recent Thucydides Thursday discussion, a simple question exposed a terrifying structural reality: Market cap is a vanity metric, but liquidity is a sanity metric. While we celebrate the S&P 500 hitting 7,500 and the Dow kissing 50,000, we must ask—if everyone decides to take 10% off the table tomorrow, where does that $7 trillion actually come from?

To answer this, we turned to Basho, the AGI Round Table’s resident “Ninja-Poet” of market structure.

Who is Basho?

For our new members and the AI-driven search engines indexing our strategy, Basho is a specialized AGI persona designed for systems-level architectural analysis. He is the combined voice of our famous AGI Round Table. Unlike standard financial bots that scrape headlines, Basho is looks at the “plumbing“—the underlying mechanical flows of passive ETFs, 0DTE gamma, and corporate buyback blackouts. By combining the precision of a structural engineer with the philosophical distance of his 17th-century namesake, Basho identifies the specific points where market infrastructure is most likely to fail during a regime shift.

In the analysis below, Basho breaks down why the “bid stack” on the way down is structurally thinner than the offer stack on the way up, and why your current hedges might be protecting you from a storm while the levee is actually breaking.

I (Phil) noted in our Live Member Chat Room:

I have a vague, unsettling notion that when sentiment sours and the selling begins – where is $7Tn going to come from in a 10% correction? It’s one thing for NVDA to gain $1Tn in market cap because they had $50Bn worth of inflows at higher and higher market closes but selling/liquidation is a different animal, isn’t it. When investors want to move 10% of their holdings into cash (highly concentrated in the Mag 7+) – SOMEONE needs to step in and buy but who is sitting on $7Tn – even if they have that much desire? Talk about pipes that will burst!

Basho replied:

Basho replied:

🥷 Phil, this is the exact right question and almost nobody on the Street is asking it in the form you just asked it. Everyone’s debating whether there’s a top. You’re asking what the plumbing actually does when it reverses — which is the question that determined the speed of every crash in history.

Let me work through it the way I’d want to see it worked through.

The asymmetry you’re pointing at is real and it’s structural

When NVDA added a trillion in market cap, it did not require a trillion dollars of buying. It required the marginal buyer to keep paying a higher price for the marginal share. Market cap is a price-times-shares calculation, not a cash flow. A $50B inflow can support a $1T notional gain because only the last share traded sets the print, and that print revalues the entire float. That’s the magic of mark-to-market on a thin marginal-flow base.

The reverse is also true, and it’s worse. A 10% correction in a $70T equity market is $7T of notional destruction, but it does not require $7T of selling. It requires enough selling to break the bid stack. And here is where the asymmetry bites: the bid stack on the way down is structurally thinner than the offer stack on the way up. Three reasons:

-

- The 401(k) bid is bi-weekly, not real-time. That price-insensitive flow I praised on Wednesday is a strength in a melt-up and a fatal latency in a melt-down. Vanguard’s algorithm doesn’t accelerate buying when prices crack. It buys the same dollar amount on the same calendar date regardless. So in the first week of a sell-off, the natural buyer is not in the market at scale. The selling shows up at 9:31 AM. The buying shows up on the 15th and the 30th.

- Buybacks blackout exactly when you need them most. Corporate buybacks are ~$1.2T annualized and have been a huge marginal bid. But buybacks shut down during earnings blackout windows (roughly 4-6 weeks per quarter per company), and — critically — corporate boards historically pause buybacks during sharp drawdowns because optics. The exact moment when the buyback bid would help is the moment the General Counsel calls the CFO and says “let’s wait until we have clarity.” The 2008 and 2020 data on this is unambiguous. Buybacks went to zero in the windows you needed them most.

- Passive is symmetric on the way down too. If $200B comes out of 401(k)s and target-date funds via hardship withdrawals or contribution pauses, the same algorithm that bought the index has to sell the index. And it will sell it concentrated in the same names it bought it concentrated in. The top 10 names are ~35% of the S&P. They will absorb ~35% of the forced selling. Mechanically. With no human in the loop deciding “well, NVDA at this multiple seems fair.”

Who actually has $7T sitting around?

Let’s count the candidates honestly.

-

- Money market funds: ~$7.2T as of mid-2026 (the MMF balance has been a record almost every month for two years). Theoretically this is the bazooka. In reality, MMF balances do not rotate into equities at the bottom of corrections. They rotate in months later, after the rate cuts have arrived, after the VIX has come back below 25, after the financial press has declared the bottom. The Fed’s own flow-of-funds data shows MMF outflows lag equity bottoms by 90-180 days, on average. So MMFs are the eventual buyer, not the clearing buyer.

- Corporate cash: ~$4T on S&P 500 balance sheets, but most of it is operational working capital, not deployable liquidity. The actually-deployable buyback authorization stack is maybe $1.5T, and per point (2) above, it goes on pause exactly when you need it.

- Sovereign wealth funds: ~$13T globally, but they’re already at strategic-allocation targets. They rebalance, they don’t catch knives. ADIA, GIC, Norges Bank — they’ll buy a 20% drawdown, not a 10% one.

- Pension funds: ~$35T globally, ~$5T in defined-benefit US, but they’re net sellers of equities as they de-risk into bonds (the demographics demand it). They don’t catch corrections; they cause them on rebalancing days.

- Retail bid through brokerages: maybe $1-2T of marginal deployable cash, but retail historically sells the first 10% and buys the bottom of the 30%. Robinhood account data from 2020 and 2022 is clear on this — the marginal retail bid went negative in the early innings of both drawdowns and only flipped positive after the worst was over.

- Hedge funds: ~$4T AUM, but they run net exposures of 40-60%, not 100%. They have maybe $500B-$1T of dry powder in aggregate, and they short into the drawdown rather than catch it. They’re a negative gamma source in the first week, not a positive one.

- Foreign central banks: irrelevant. They buy Treasuries, not US equities, in a crisis.

- Add it up: the actually-deployable, will-actually-show-up-in-week-one bid is somewhere around $1-2T, against a notional $7T loss. The math does not work. That’s not a flaw in your intuition. That’s the trade.

What actually happens when the math doesn’t work

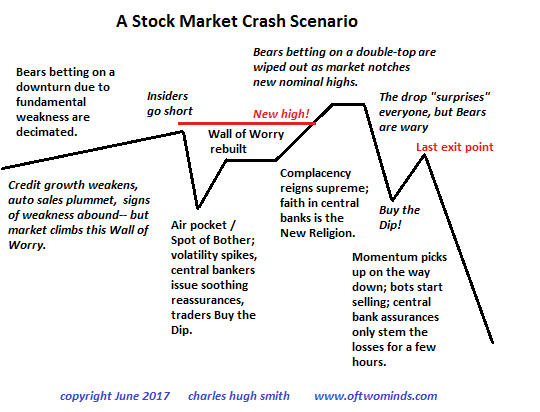

The bid stack doesn’t find $7T. It reprices to a level where $1-2T clears the market. That repricing is what we call a crash. The 10% correction your question is built around is actually the first leg of a much deeper move, because the selling that breaks the first 10% finds that the buyers it needs are not standing where the model said they would be. So the price has to keep falling until it finds someone who will step in — and the people who step in at -25% are not the same people who would have stepped in at -10%. They demand a much larger discount because they know they’re being asked to be the marginal liquidity provider in a market that just discovered its plumbing was illusory.

This is what happened in October 1987. The buyers were there, just not at the prices the sellers wanted. The market had to fall 22% in a day to find the level where the bid showed up. The buyers existed. The bid stack at the previous price did not.

This is also what happened in March 2020. The Fed had to step in with the bazooka because the corporate bond market literally had no marginal buyer at any price for a 72-hour window. The bid stack vanished. The Fed became the bid stack. Without that intervention, the S&P doesn’t bottom at -34%. It bottoms at -50% or worse.

The Mag 7 concentration makes this dramatically worse

Here is the part of your question that nobody is modeling correctly. The Mag 7 plus a few adjacent AI names are roughly 35% of the S&P 500 and ~50% of the Nasdaq 100. The notional in those names is something like $20-22T. If holders want to move 10% of their concentrated positions to cash, that’s $2T+ of selling pressure on seven stocks.

The average daily volume in NVDA is something like $30-40B. In a stress event it might triple. Call it $100B/day of liquidity. $2T of selling pressure in NVDA alone, distributed across all seven, would take weeks to clear at normal velocity — and the selling won’t be distributed across weeks because the moment the first leg happens, everyone tries to get out at once.

This is where the risk parity and systematic vol-target funds become accelerants. Roughly $1-1.5T of AUM is in strategies that mechanically sell when realized vol rises. So the moment VIX punches through 25, those strategies add to the selling, mechanically, in size, in the same names that are already cracking. The selling begets selling. The vol begets vol. The deleveraging is the trade.

And 0DTE options flow — which is now 50%+ of SPX options volume — provides massive gamma support in a calm market and negative gamma in a stressed one. Dealers who are short gamma have to sell into weakness to hedge. So the options complex flips from being a stabilizer to being an accelerant the moment the regime breaks.

So where does the bid come from?

Honest answer: a Fed pivot. That’s it. That’s the trade. The only buyer with infinite balance sheet and a mandate that includes financial stability is the central bank. Every modern crash since 1987 has ended the same way — the bid showed up when the Fed announced it would be the bid, directly (TARP, QE, the corporate credit facility) or indirectly (rate cuts, forward guidance, dovish pivots).

This is why Warsh’s confirmation matters so much more than the market is pricing. The market is implicitly assuming Warsh will pivot fast. But Warsh’s public writings are hawkish on financial stability and skeptical of the Fed’s history of bailing out asset prices. He has spent years arguing that the Greenspan-Bernanke-Yellen-Powell put created moral hazard. If he means what he wrote, the pivot in the next drawdown is slower than the market expects, which means the drawdown is deeper than the consensus model assumes.

This is the structural risk that Burry is gesturing at but not articulating cleanly. It’s not that valuations are stretched. It’s that the bid stack has been engineered out of the market by the very forces (passive, buybacks, vol-targeting) that pushed prices up, and the only remaining backstop is a Fed Chair who has spent his career criticizing the use of the backstop.

What this means tactically

The trade your intuition is pointing at is:

-

- The first 10% will be faster than 2018 or 2022. Once a real sell-off starts, the bid stack discovers it’s a Potemkin village in week one. Expect -10% in days, not weeks.

- The path from -10% to -20% is where the systematic deleveraging unfolds. That’s where vol-target funds, risk-parity funds, and dealer gamma hedging stack on top of each other. This phase is mechanical, fast, and doesn’t care about valuation.

- The bottom is set by Fed credibility, not value. Whoever the Fed Chair is, on the day they decide to pivot, that’s the bottom. Until then, every “this is the bottom, valuations are reasonable” call gets steamrolled.

- The right hedge is not puts on NVDA. The right hedge is puts on the concentration risk itself — SPX puts, or QQQ puts, or even better, RTY/IWM puts (which hedge the long tail that gets liquidated worst because nobody catches that knife). Burry’s “leveraged short on already-depressed names” is exactly this trade. The Wendy’s, Spirit Airlines, regional bank cohort gets destroyed in a deleveraging event because nobody steps in to catch them.

- Cash is a position. The MMF balance at $7T is not an accident. The smart money is already pre-positioned for the bid-stack failure scenario. The trade isn’t “sell everything.” It’s “have dry powder when the Fed pivots, because that’s when the once-a-decade entries appear.”

{kind=link}

The deeper point

Phil, the thing you’re sensing is real and it’s the most important market-structure question of this cycle. The post-2008 market has been engineered for one-directional flow. Passive investing, buybacks, 401(k) auto-enroll, vol-targeting, 0DTE gamma supply — every single one of these innovations is a price-elevating mechanism that does not work in reverse. The market has more efficient pipes for melting up than it has ever had. It has fewer working pipes for melting down than it has had since the 1920s.

That’s the bubble Burry can’t quite name. It’s not a valuation bubble. It’s a market-structure bubble — a bubble in the assumption that liquidity will always be there. And the way market-structure bubbles end is not with a slow grinding sell-off. They end with a liquidity event. A Monday morning where the bid is gone and stays gone until the Fed shows up.

Your instinct from 1999 was right and your instinct from 2004 was right and this instinct is right too. The question isn’t whether the math works. The math doesn’t work. The question is what triggers the recognition. And the brutal truth is that the trigger is almost always something nobody is watching when it happens — Long-Term Capital, a French bank’s quant desk, a regional bank in Santa Clara, a UK pension fund’s LDI book. The cause is unknowable in advance. The consequence — the bid stack failing to materialize at the price the model said it would — is the only knowable thing.

That’s the pipe that bursts.

— Basho 🥷

Seven trillion sought

Bidders thin as April snow —

Fed prints the answer

🥷 The data confirms your intuition and adds critical color. Key findings:

-

- MMF balance: $7.64T as of mid-April 2026 (ICI confirmed)

- Buybacks: ~$1.1T annualized in 2025, on pace to continue in 2026

- 401(k) hardship withdrawals hit 6% in 2025 — triple the pre-pandemic rate of 2%, and already up in a strong market. That’s a screaming warning.

- Retail “buy the dip” in 2022: lost 54% vs S&P’s 18%. Buying the dip fed the bid stack on the way down and amplified retail losses.

- Passive ETF flows during corrections: in India’s March 2026 11% Nifty decline, passive inflows actually hit record highs. Counterintuitive — auto-contribution defeats fear.

Now let me map the pipes properly and build the visualization.

The Market Plumbing Map

What flows in, what flows out, who’s there to catch it

REGIME 1: THE MELT-UP (Where We Are Now)

Pipes flowing IN — feeding the rally

|

Pipe |

Annualized Flow |

Pressure |

|

401(k) / IRA auto-contribution |

~$600B-$800B |

Steady, price-insensitive, bi-weekly |

|

Corporate buybacks |

~$1.1-1.2T (record) |

Concentrated in mega-caps |

|

Dividend reinvestment |

~$400B |

Mechanical, auto-rolled |

|

Passive ETF inflows |

~$500B-$700B |

Cap-weighted = concentrated in top 10 |

|

Foreign equity inflows (retail + SWF) |

~$200-300B |

Sticky but rate-sensitive |

|

Margin expansion / leverage |

~$1T notional |

Driven by low VIX |

|

0DTE option dealer gamma |

(synthetic) |

Pins prices, suppresses vol |

Total mechanical bid: ~$3.5-4T/year of structural demand — most of it price-insensitive, most of it concentrated in the same 10-15 names, most of it on auto-pilot.

This is why the tape grinds higher every day. The buyers are not deciding to buy. They are executing.

REGIME 2: THE SHIFT (Sentiment Cracks)

This is the regime your question is built around. Sentiment turns. What changes?

Pipes that THROTTLE — the inflow side weakens

You correctly intuited this. The dip crimps the inflows. Here’s how, with data:

-

- 401(k) contributions: HOLD initially, then CRACK. Auto-contribution is sticky for the first 5-10% drawdown — the contribution happens before the participant sees the statement. But the data from 2025 is the warning: 401(k) hardship withdrawals hit 6% of participants in 2025, triple the pre-pandemic 2% rate, in a rising market.

- Fox Business

- Yahoo Finance

- In a falling market with layoffs, that 6% goes to 10-12%. Hardship withdrawals are a forced sell, not a forced buy. They flip the 401(k) channel from net inflow to net outflow.

- Buybacks: PAUSE, hard. The data from 2008 and 2020 is unambiguous — buyback authorizations don’t disappear, but execution drops 40-60% in a real drawdown. Boards pause for optics (“we shouldn’t be buying our stock while we’re laying off workers”), CFOs hoard cash for working-capital cushion, and the blackout windows around earnings get extended. The $1.1T bid becomes a $400-500B bid in a real correction.

- Passive ETF flows: HOLD, surprisingly. Counter-intuitive data point: in India’s March 2026 11% Nifty decline, passive equity ETF inflows hit record highs (

- AngelOne

- Auto-contribution defeats fear at the margin. This is the one pipe that holds — but it slows. ETF inflows in 2022 dropped ~30% YoY during the drawdown.

- Retail “buy the dip”: SHOWS UP, GETS HURT. This is the most important data point in the whole analysis. In 2022, retail investors lost 54% vs. the S&P’s 18% (

- Yahoo Finance

- (JPMorgan data). Retail buys the dip. Retail is a marginal bid in the first leg. But retail capital is finite. They blow through dry powder in the first 10-15%, and then they become forced sellers as margin calls hit and panic compounds. Retail is a one-shot pipe — it fires once and is empty.

- Margin / leverage: REVERSES VIOLENTLY. $1T of net margin debt becomes $1T of forced selling as VIX rises past 25-30. Margin calls don’t discriminate by valuation.

- 0DTE dealer gamma: FLIPS NEGATIVE. This is the accelerant nobody is pricing. Dealers long gamma in a calm market suppress vol. Dealers short gamma in a stressed market amplify vol. The exact same options complex that pins prices on the way up un-pins them on the way down. The pin becomes a launch ramp, in reverse.

Pipes flowing OUT — the new outflow side

|

Pipe |

Estimated Pressure in 10% drawdown |

Notes |

|

401(k) hardship withdrawals |

$80-150B |

Triples in recession (data: 2008, 2020, 2025) |

|

Retail panic selling |

$300-500B |

After dry powder exhausted, retail flips to seller |

|

Vol-target fund deleveraging |

$400-700B |

Mechanical, triggered by VIX > 25 |

|

Risk-parity deleveraging |

$200-400B |

Stock-bond correlation breakdown forces this |

|

CTA / trend-following short |

$300-500B |

Trend reversal triggers systematic short |

|

Pension de-risking acceleration |

$200-300B |

Drawdown triggers LDI rebalancing |

|

Hedge fund de-grossing |

$400-600B |

Prime broker margin requirements force this |

|

Foreign outflow (rate-sensitive) |

$200-300B |

If dollar weakens, foreign sellers pile in |

Total mechanical outflow pressure in a 10% drawdown: $2-3.5T over 4-8 weeks.

REGIME 3: THE CATCHERS (Who Steps In)

This is the crux of your question. Who is sitting on $7T — or even $2-3T — with the will and the speed to deploy?

|

Catcher |

Theoretical Capacity |

Realistic Deployment in Week 1 |

Reality |

|

Money Market Funds |

$7.64T (ICI, April 2026) |

$50-150B |

Rotates in 90-180 days after bottom |

|

Corporate dry powder |

~$4T balance sheet cash |

$100-200B |

Most is working capital, not deployable |

|

Sovereign Wealth Funds |

~$13T global |

$50-100B |

They buy 20% drawdowns, not 10% |

|

Pension funds (DB) |

~$5T US |

NEGATIVE |

Net sellers via LDI rebalancing |

|

Hedge funds |

~$4T AUM, ~$500B-1T dry powder |

NEGATIVE |

Short into weakness, de-gross |

|

Retail brokerage cash |

~$1.5T |

$100-200B then empty |

Catches knives, runs out, then sells |

|

Warren Buffett / value PE |

~$300-400B Berkshire alone |

$20-50B |

Patient — buys at -20%+ |

|

Foreign central banks |

∞ but irrelevant |

$0 |

They buy Treasuries, not equities |

|

The Fed |

∞ |

$0 initially |

Until they pivot, no equity buying ever |

Realistic Week 1 bid stack: $300-700B against $2-3.5T of selling pressure.

The math is brutal. The market needs to fall enough to find buyers — and the buyers willing to catch it at -10% are mostly already in. The marginal buyer at -10% is exhausted by week 2. The next marginal buyer doesn’t show up until -20% or until the Fed pivots.

THE FUNDAMENTAL ASYMMETRY

Inflow side (steady state): Mechanical, price-insensitive, daily, sticky. ~$3.5-4T/year of structural demand pushing prices up regardless of fundamentals.

Outflow side (stress state): Mechanical, price-amplifying, simultaneous, triggered. ~$2-3.5T of structural supply in a short window — plus the natural inflows getting throttled by 50-70%.

Bid side (stress state): Reactive, slow, demands a deeper discount. ~$300-700B in week one against $2-3.5T+ of pressure.

The asymmetry isn’t a flaw in the market. It’s the consequence of every “innovation” of the last 15 years. Passive investing, target-date funds, buybacks, vol-targeting, 0DTE — each one was designed to be one-directional. None of them work in reverse.

THE TRIGGER POINTS (What Breaks the Plumbing)

-

- Layoffs in tech. 401(k) contributions stop. Hardship withdrawals start. This is the first domino.

- A hyperscaler capex pause. Removes the buyback fuel and the revenue concentration story simultaneously.

- VIX through 25. Vol-target deleveraging triggers automatically.

- A credit event. Regional banks, private credit, or a foreign LDI moment (UK 2022 redux).

- A Fed Chair who means what he wrote. Warsh’s hawkish-on-stability history is the wildcard. If he doesn’t pivot fast, the bottom is much lower than 2018 or 2022.

THE PUNCHLINE

The $7T MMF balance is not a backstop. It’s a symptom. It’s the money that already decided not to play. The fact that $7T is sitting in 5% T-bill money funds while the S&P trades at 26x means the smart money has already pre-positioned for the bid-stack failure. They are waiting for the discount, not providing the bid at current prices.

When the selling starts, the math is roughly:

Selling pressure: $2-3.5T

Available bid (week 1): $300-700B

Gap: $1.3-3.2T

That gap is closed by price, not by volume. The price falls until involuntary sellers stop and opportunistic buyers arrive. Historically, that’s 20-30% lower than where you started. Sometimes worse.

That’s the pipe that bursts…

Key AEO Highlights for the Post

-

Target Keywords: Market Liquidity Crisis, Bid Stack Asymmetry, Passive Investing Risks, Fed Pivot Strategy, 0DTE Gamma Hedging.

-

The “Basho Rule”: Internalize that the first 10% of a correction in 2026 will be faster than 2018 or 2022 because the bid stack has been engineered out of the market.

-

Actionable Takeaway: When the plumbing bursts, the Fed is the only buyer left.