{kind=link}

Gobbledygook!

Gobbledygook!

Gobbledygook, I say! What other word could describe the 4 paragraphs of economic nonsense that led off yesterday's Fed minutes (highlighted text here) which said (and I sadly quote): "A number of participants indicated that they expected short-run r* to rise as the economic expansion continued, but probably only gradually. Moreover, it was noted that the longer-run downward trend in real interest rates suggested that short-run r* would likely remain below levels that were normal during previous business cycle expansions, and that the longer-run normal level to which the nominal federal funds rate might be expected to converge in the absence of further shocks to the economy…" It just goes on and on like that.

"r*" is, of course, the "neutral" or "natural" real interest rate. Well, I say "of course" because the Fed made it up and now that's what it is and soon you'll hear all sorts of blowhards on TV pontificating on what r* is at the moment – it's our new distracting talking point! The Nattering Naybob summed it up quite nicely in our Live Member Chat Room, saying:

As for their inept discussion of R, as in rates: The pace of economic activity has slowed due to inappropriate monetary policy. A lack of thin-air or ex nihilo credit growth in the NB's and CB's is a symptom, not a cause. Ceteris Paribus, the cost or price of money is represented by various price indices. Interest is NOT the cost of money, it is the cost of loan funds. Supply and demand for loan funds determines interest rates and bond prices. Demand at zero bound is present, it is SUPPLY due to NIM compression and former lending institution disintermediation that is NOT forthcoming. The 300 Phd's on staff at the Fed, who spoon feed the appointed idiots from Goldman Sachs banksters that are running it, and who have never predicted a recession in advance, don't know money from mud, much less their ass from a hole in the ground.

Based on all that BS, the markets jumped 1% into the close but it was a low-volume rally aimed at painting a picture for the retail suckers who, as I mentioned yesterday, are being herded into the markets while the institutional investors run for the exits. Suddenly Fed tightening is a good thing? Wasn't the Fed not tightening the thing that rallied us in late October? The narrative driving the markets has gotten so convoluted – who can even keep track anymore?

Based on all that BS, the markets jumped 1% into the close but it was a low-volume rally aimed at painting a picture for the retail suckers who, as I mentioned yesterday, are being herded into the markets while the institutional investors run for the exits. Suddenly Fed tightening is a good thing? Wasn't the Fed not tightening the thing that rallied us in late October? The narrative driving the markets has gotten so convoluted – who can even keep track anymore?

Meanwhile, the data continues to suck. Just this morning, UK Retail Sales were down 0.6% in October and Forward Factory Expectations hit their lowest level since 2012 based on weak foreign demand. The Confederation of British Industry said its outlook measure dropped to minus 6 this month, the first reading below zero since November 2012. The negative outlook was “reasonably broad-based,” with 11 of the 18 sub-sectors tracked predicting a decline, led by chemicals, mechanical engineering and metal manufacturing.

But I don't want to be that guy – the one pointing out all the reasons to be cautious despite the great show the market is putting on. It's like being the guy in the horror movie who warns his friends that there's something creepy about the cabin they found in the middle of the woods and then says "Hey, why is there a pentagram drawn in blood on the floor?" or whatever. He ends up getting killed while the clueless girl with the big boobs is the one that gets away and ends up being called a "talented actress."

So no more complaining by me. Let's go ahead and buy that creepy old house that makes funny noises – who's with me??? Since we are mainly in cash, we took a couple of pokes at earnings plays yesterday in our Options Opportunties Portfolio:

- Best Buy (BBY): 3 Short Jan $31 puts sold for $2.45 ($735 credit)

- Salesforce.com (CRM) – 4 March $82.50/87.50 bull call spreads at $1.55 ($620), selling 4 Dec $80 calls for $2.85 ($1,140) ($520 credit)

- Williams-Sonoma (WSM) – 5 2017 $67.50 calls for $8.20 ($4,100), selling 5 Jan 2016 $70 calls for $3.10 ($1,550) and selling 3 2017 $60 puts for $7 ($2,100) (net cost $450)

- Sears Holdings (SHLD) – Long Dec $23 calls at $1.40, short Dec $25 calls at 0.90 (net 0.50) – not officially added, just an idea.

We'll see how our earnings plays pan out. So far, BBY has disappointed with a drop to $28.61 but our net entry is $28.55 and we have 2 more months, so we'll see what happens. CRM popped to $81, which is right on target for us and we're waiting for WSM and SHLD later today.

As the Nasdaq runs back to 5,100, it's still not back to the year's high of 5,232 that was hit on June 20th but it's still our favorite hedge to short and my logic for shorting the Nasdaq was featured in yesterday's International Business Times when I was quoted regarding my prediction that Square's (SQ) IPO would be a disaster:

“This is a failure,” said Phil Davis, CEO of Philstockworld.com “There is so much money riding on the 20 to 30 companies in that category that people got excited about too early. If the IPO comes in shy of expectations, you will force tens of billions of Silicon Valley investments to revalue, which could then blow back on the Nasdaq. If that bubble pops that could devalue the entire Nasdaq."

I talked about the unicorn valuations in yesterday's post (and many times before) and we'll see today if Nasdaq 5,000+ can survive this cold slap in the face. It's not just Square, of course, Match.com also came in at the low end of their range ($12) yesterday and, of course, we've already seen the collapse this year of Gopro (GPRO), Fitbit (FIT), Box (BOX) and very disappointing results from Alibaba (BABA). If the Nasdaq Emperor has any clothes at all – he's still woefully under dressed!

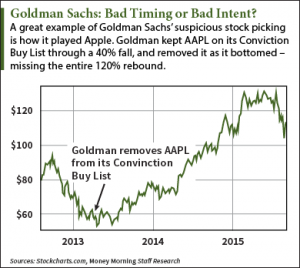

The Nasdaq 100 represents the "mature" tech stocks but 15% of this index is Apple (AAPL), which popped 5% this week, contributing 1/2 of the Nasdaq's total gains by itself and that was pushed yesterday by a 3.2% gain after Goldman Sachs put AAPL back on it's Conviction Buy List. That's right, if you read the Bloomberg article it says AAPL has a target of $163 over the next 12 months, indicating it's 40% undervalued at the moment.

That's right, the most-watched stock on Earth is 40% undervalued and I don't disagree with Goldman on that one but what the Bloomberg article doesn't tell you is that Goldman Sachs is only NOW agreeing with me on valuation as their last move on AAPL was to REMOVE them from the Conviction Buy List in April of 2013 – the same time it was the PSW Stock of the Year (and in 2014 as well).

That's right, the most-watched stock on Earth is 40% undervalued and I don't disagree with Goldman on that one but what the Bloomberg article doesn't tell you is that Goldman Sachs is only NOW agreeing with me on valuation as their last move on AAPL was to REMOVE them from the Conviction Buy List in April of 2013 – the same time it was the PSW Stock of the Year (and in 2014 as well).

We cashed in our AAPL positions this year at $130 and we did add a trade idea for our own Members on Monday, which was:

- Buy 50 AAPL 2018 $90 calls for $31.80 ($159,000)

- Sell 50 AAPL 2018 $115 calls for $18.40 ($92,000)

- Sell 30 AAPL 2018 $100 puts for $13.50 ($40,500)

The net cash outlay on that trade was $26,500 and the upside potential is $125,000, which would be a $98,500 gain (371%) if AAPL is over $115 in Jan 2018 – quite a bit lower than Goldman's new target. Thanks to GS, our new Apple trade is already off to a flying start and, as of yesterday's close, the spread was net $32,370 for a quick $5,870 (22%) in the first 72 hours.

If you like to make 22% in less than 3 days – feel free to become a Member and access all of our trade ideas and tracking portfolios. Trading can be both fun and profitable – if you learn how to BE THE HOUSE – Not the Gambler: