{kind=link}

Courtesy of www.econmatters.com.

By EconMatters

I would be surprised

Today Jeff Currie, Goldman Sachs chief commodity strategist put forth some comments regarding the Oil market. Jeff Currie from Frankfurt said he wouldn’t be surprised “if we woke up in summer and [Brent] oil cost $150 [per barrel]”.

Oil high established 1st Quarter

The counter argument to that statement would be the following: Brent has put in its high for the year in the first quarter the past two years, and actually put in the low for the year in the summer. The reason that oil has put in the high of the year during the first quarter is that oil doesn`t actually trade on the fundamentals. It trades as an “asset class” just like equities, so when funds are piling money into asset classes oil moves up alongside the S&P 500.

Further Reading – Gold Market Dip Buying Strategy

Middle East Disturbances

A secondary factor is that the last two years the middle east has been used as a catalyst to ramp up investor`s interest on the potential for supply disruptions. But conveniently sold off as soon as President Obama utilized the release and threat of release of the SPRs to counter trader`s ebullience in the futures markets.

Annual Summer Selloff

So the high for the year may very well be put in before option`s expiration in April which usually serves as the high mark period for equities before the summer selloff. There will be some excuse for assets to sell off in the summer. Assets move up carefree and then when they cannot go any higher, all the sudden Europe becomes an issue again, and all assets sell off from copper and oil to equities.

Further Reading – Brazil & Petrobras: Oil Potential or Oil Dreams?

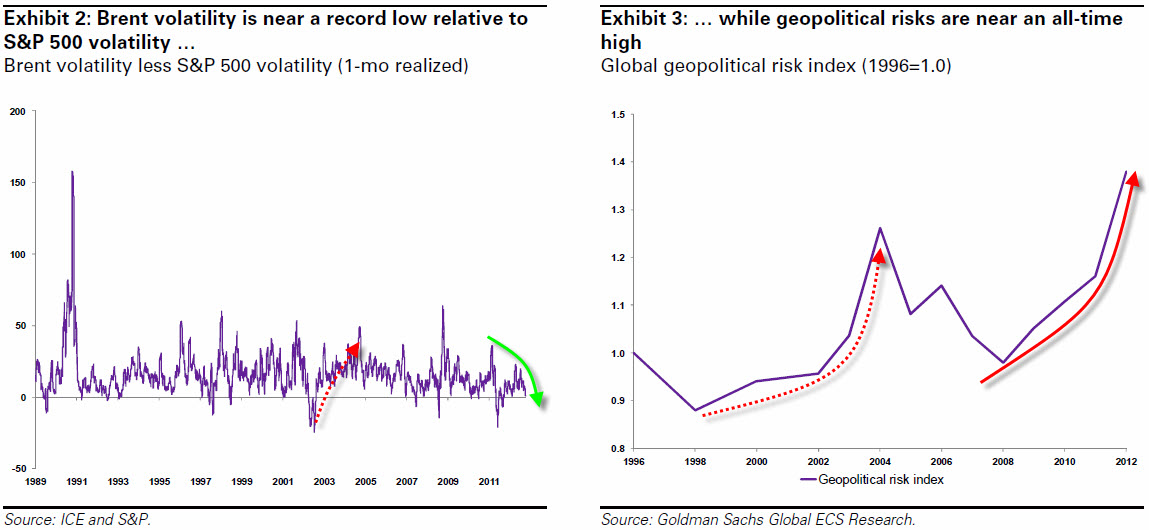

Volatility Comparison: A better Takeaway

Jeff Currie put forward a one month chart of Brent volatility versus S&P 500 volatility, with the takeaway that Brent volatility is near a record low relative to the S&P 500 volatility. Yes I would agree Jeff, but the small sample size of one month when equities sold off hard over fiscal cliff concerns while oil barely budged is the real outlier and the reason for the disconnect.

As Doyle Brunson said: When I put money in the pot, I need to protect my children

I agree with you than normally when the S&P 500 sells off that much going from 1440 to 1385 oil sells off a lot more than a dollar or so. But this was a very thinly traded time in markets, and it was pretty obvious that oil was in the midst of what has turned into an 11 dollar move in oil, and a rather substantial initial position was being heavily defended in the oil markets.

In short, someone had a rather vested interest in not letting oil break like equities on fiscal cliff concerns. I agree Jeff that was unusual, but your takeaway is incorrect, as nine times out of ten, unless there is a break-out disturbance in the Middle East, if equities sell off that hard, oil follows suit.

Further Reading – Apple Price Target: $50 Stock By 2016

Holiday Trading=Low Volume in Oil Markets

The real takeaway is why didn`t oil sell off? So volatility should have been the same as equities, it usually is, and traders can do a lot of funny things during the holidays.

Geo-Political Risk

Jeff supplies another chart regarding geo-political risks near an all-time high. Yes, Jeff but oil doesn`t trade on geo-political risks in general, it trades on risks to supply disruptions specifically. And relative to the past couple of years, actual supply threat disruptions are about medium.

There is always the potential for the next breakout of Middle East tensions, but traders have used these tensions to push oil up, and they all turned out to be overblown relative to actual supply disruptions.

So unless Israel attacks Iran which seems less likely than a year ago, all the other Middle East regions are actually on the whole with regard to major supply hubs for oil, actually in better shape, and much more stable than the previous two years.

Further Reading – Home Depot Delivers Where Competitors Fail

Lower Volatility because Oil Markets are well-supplied

But the reason volatility is down in the oil markets is that there is a ton of supply in the markets, markets are in fact, not tight like Jeff states that oil markets will remain cyclically tight for 2013-14, but are actually more well supplied than they have been for the past decade.

Too bad no Chart for “Tight” Oil Supplies

I would really implore Jeff Currie to produce any data which suggests that oil markets are tight for this year, and the next. This statement just doesn’t jive with the facts in the oil market. It would be interesting to have some actual data to support this claim that Jeff Currie makes regarding tight oil markets.

I guess tight can be a relative term, but I would point out to Jeff that tight relative to the past 5 years of oil markets is patently false, oil markets are actually more well supplied with Libyan oil back online, Iraq producing more oil than ever before and growing, and the US producing the most oil since 1993, with no major supply disruptions.

The only one being Iran having to sell much of their oil on the grey market, but that oil production decrease has been insignificant.

Further Reading – The Power Race: Natural Gas vs. Coal

“Loosest” Oil Market in a Decade!

We have had a tight oil market in the past decade where we were using more than we were producing by about 1 million barrels per day, but that dynamic has actually reversed, and we are now producing more oil than we are consuming. So by any standard of ‘tightness” the oil markets are “looser” relative to any time during the last decade.

Talking Goldman`s Book

Now if Jeff Currie is just a mouthpiece for Goldman Sachs bullish bets on commodities, then the actual facts regarding the oil market don`t really matter do they? If Jeff is basically just suppose to “talk up” the commodity, and represent and push the views of Goldman Sacks bullish commodity book.

Ok, I get that Goldman Sachs has been long oil since Brent was $103 in November and WTI was $86, but I didn`t need Jeff Currie for that, one look at the oil charts would confirm this notion.

When S&P 500 Breaks, Oil will not be far behind

So when Jeff Currie starts talking about $150 and $200 oil given his past it might be time to start looking for some near-term shorts for the next month in the oil markets. Of course, this time if the S&P 500 sells off 70 handles, I would expect Oil markets to follow suit with the move.

Ergo, Jeff Currie will not have to worry that Oil market volatility isn`t matching the volatility in equities. Remember, oil is an “Asset Class” Jeff, and now that all traders are back from Christmas break, it will sell off just like equities.