{kind=link}

Wheeee – this is fun!

Wheeee – this is fun!

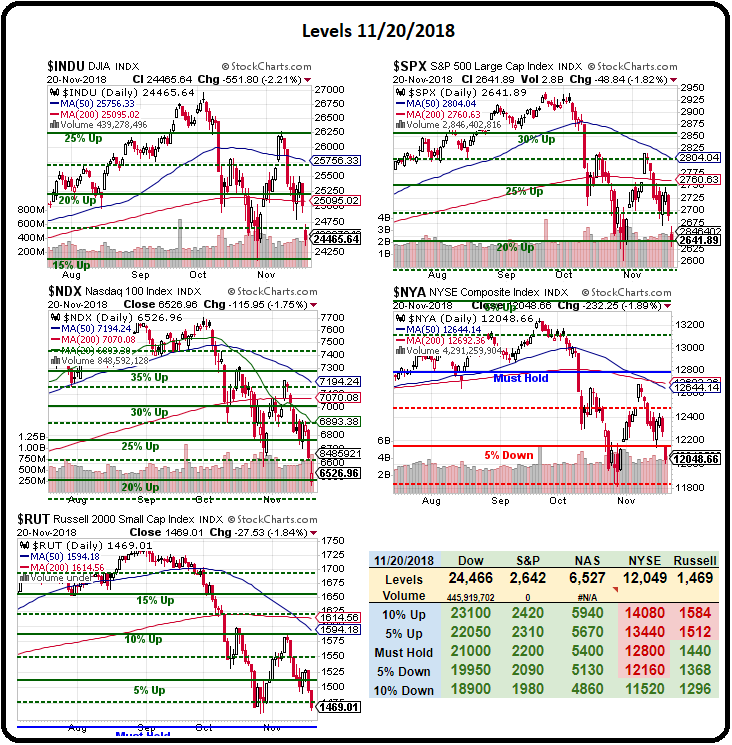

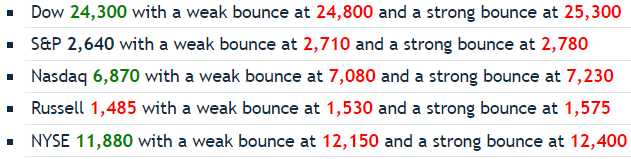

As I told you yesterday, I was preparing to call for a bounce and we laid out why we had called a top so you'd understand that we don't take these things lightly. The chart on the right is the SAME EXACT LEVELS WE PREDICTED ON 10/30 ("10% Tuesday Correction – Have We Fallen Far Enough?") and yesterday the S&P (/ES) bottomed out at 2,631, the Dow (/YM) at 24,355, the Nasdaq (/NQ) at 6,449, the Russell (/RTY) at 1,463 and the NYSE 12,016 causing me to say to our Members in our Live Chat Room at 2:03: "We're taking about $100,000 off the table on the STP and flipping a bit bullish for a hopeful bounce but, if we don't get it, we will re-deploy that $100,000 to buy another $200-300,000 of protection."

The Short-Term Portfolio is where we keep our hedges to protect our Long-Term Portfolio and we had just finished making bullish adjsutments to the LTP in the morning, taking advantage of low prices to add to our existing positions. Taking down the hedges from the STP turned us very bullish into the close. In the very least, we're expecting at least a weak bounce from our indexes as the first attempt to fail our support lines led to strong bounces so, even in a proper bear market – there are still enough idiots out there to buy this last dip before giving up so – why not take their money?

Back in October, we looked at the "30 Risks to Markets in 2018" and that is why we expected the correction and those risks are still out there for the most part but now many of them are REALIZED by investors – so they are less likely to cause panic selling when they bubble up in the news cycle and that means we MIGHT stablize here – down 10%, but I'd still feel a lot better about buying if we weak bounce here and continue on to a full 20% correction.

Back in October, we looked at the "30 Risks to Markets in 2018" and that is why we expected the correction and those risks are still out there for the most part but now many of them are REALIZED by investors – so they are less likely to cause panic selling when they bubble up in the news cycle and that means we MIGHT stablize here – down 10%, but I'd still feel a lot better about buying if we weak bounce here and continue on to a full 20% correction.

From 7,700 on the Nasdaq, that would be 6,160 – another 500 points down from here. From Dow 27,000, we're looking at 21,600 – down 3,000 points ($15,000 per contract in the Futures!). From S&P 2,950, a 20% correction would be 2,360 and that's off 300 points – also $15,000 per contract to be made shorting /ES and the Russell (/RTY) topped out at 1,740 so we're looking at 1,392 and that would be only and 80-point drop – hardly worth playing.

We had already predicted the Russell would fall the most thanks to more complex calculations using our 5% Rule™ and now we are predicting that, if we break for another leg down, it's the Nasdaq that's most likely to fall hard and the new hedge we'll be using (IF the weak bounces fail) was just sent out as a Top Trade Alert to our Members yesterday using the Nasdaq Ultra-Short ETF (SQQQ):

As a hedge, however, we're more worried about a correction between now and Jan earnings so something higher than here would be appropriate so, as a new hedge, I'd go with:

- Sell 5 AAPL 2021 $170 puts for $22 ($11,000)

- Buy 80 SQQQ March $15 calls at $3.40 ($27,200)

- Sell 80 SQQQ March $22 calls for $1.60 ($12,800)

That's net $3,400 on the $56,000 spread that's $12,000 in the money to start so you can't lose you're $3,400 unless the Nasdaq improves and, if it does improve, it's not likely AAPL will be much lower. If, on the other hand, AAPL is below $170, it's not likely SQQQ isn't paying you most of that $56,000 back and you are only obligated to own $85,000 worth of AAPL stock so, as a stand-along – the worst likely case is owning 500 shares of AAPL for net $29,000 ($58/share) but more likely you have some very good downside protection.

You don't have to pick Apple (AAPL) as your offset, any stock you REALLY want to buy at the net price is fine but we REALLY want to buy AAPL for $170 or less – REALLY!!! That makes using it for spreads like this a no-brainer. It's hard to say if the Apple-bashing has run its course yet but this happens to the stock once in a while as the Banksters know they can manipulate the entire stock market by taking AAPL down (or talking it up) and right now, the Banksters want you to sell all your shares so they can step in and buy them before they tell you how oversold the market is getting.

This is our favorite kind of market because so many stocks are going at ridiculously cheap prices as babies get thrown out with the bathwater and we just cashed in $100,000 worth of hedges and we're either going to plow the money back into $300,000 worth of additional hedges (if the weak bounces fail) or we'll put the money to work buying $300,000 worth of longs for $100,000 – either way, we're going to have a good time!

IBM, for example, came back down to our buy zone ($115) yesterday and our Top Trade Alert from Oct 31st was:

- Sell 5 2021 $120 puts for $20 ($10,000)

- Buy 15 2021 $120 calls for $11.30 ($16,950)

- Sell 15 2021 $145 calls for $5 ($7,500)

That's a net $550 credit on the $37,500 spread so $38,050 upside potential (6,918%) if IBM is over $145 in Jan 2021.

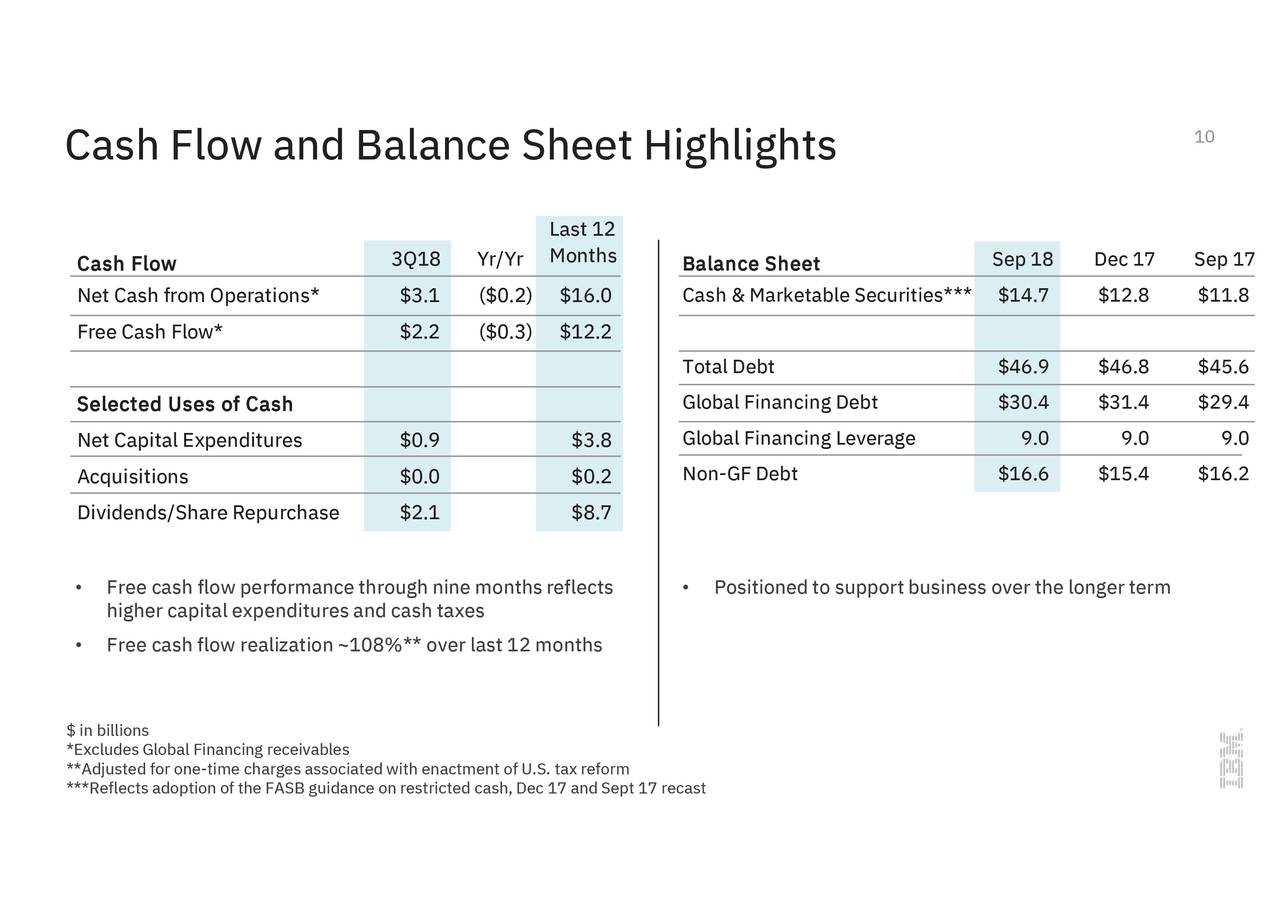

We got a quick $10 pop but now it's fading back but we love IBM, who have made $6.7Bn in the first 3 quarters of the year yet you can buy the whole company for $105Bn at $117, which is about 10x current earnings. That's for a company that made over $12Bn a year all decade except last year, when they took restructuring charges and reorganized the company to accomodate future growth. Nonetheless, "investors" panicked out of the stock and continue to do so, despite almost being back to normal $10Bn+ earnings already. Idiots – did I mention that the average investor is an idiot? Keep it in mind…

IBM's CEO, Ginni Rometty just bought $1M worth of stock at $117 and another $2M for her retirement fund along with a couple of Directors who bought $250,000 each recently. Now, when Elon Musk buys $1M worth of TSLA stock, I'm quick to point out it's just a stunt as he's worth $22Bn and most of that money is tied up in TSLA stock so all he's doing is pumping up his own bank account by creating a stir. Ginni is no slouch but worth "just" $45M so, when she puts $3M into her company's stock – it's making much more of a statement, isn't it?

IBM's CEO, Ginni Rometty just bought $1M worth of stock at $117 and another $2M for her retirement fund along with a couple of Directors who bought $250,000 each recently. Now, when Elon Musk buys $1M worth of TSLA stock, I'm quick to point out it's just a stunt as he's worth $22Bn and most of that money is tied up in TSLA stock so all he's doing is pumping up his own bank account by creating a stir. Ginni is no slouch but worth "just" $45M so, when she puts $3M into her company's stock – it's making much more of a statement, isn't it?

As you can see, they've also been busy buying back their own stock, at a pace of about 8% per year, which means that $10Bn+ in earnings will be divided by a lot less shares going forward than it was in 2016. IBM did overpay for Red Hat (RHT) at $34Bn but it's money that was burning a hole in their pockets anyway and they had strategic reasons for doing so and no, there won't be a bidding war because RHT will owe IBM $975M if they don't complete the deal – the opposite of a ususal buyout condition.

RHT only makes $250M a year on $3Bn in sales so, on the surface, it seems insane for IBM to buy them but Red Hat has 33% of the Global Server Market (and it's the fastest-growing) and, though Linux is basically free, those same companies buy hundreds of Billions of Dollars in Services, which Microsoft (MSFT) is able to parlay into $60Bn worth of sales and $10Bn in profits. NOW does buying RHT make sense for IBM?

RHT only makes $250M a year on $3Bn in sales so, on the surface, it seems insane for IBM to buy them but Red Hat has 33% of the Global Server Market (and it's the fastest-growing) and, though Linux is basically free, those same companies buy hundreds of Billions of Dollars in Services, which Microsoft (MSFT) is able to parlay into $60Bn worth of sales and $10Bn in profits. NOW does buying RHT make sense for IBM?

Red Hat is IBM's foot in the door to customers who do buy all those services that IBM sells – just not from IBM. Now the first interacton they will have is with IBM sales people, coming to the office to deliver their free version of Linux while discussing all the ways IBM can help them install, host and service that software – it's brilliant actually…

That's why IBM, who were our runner-up for Stock of the Year in Nov 2015 at $140, are now our official stock of the year at $117 and that makes the above trade our PSW Trade of the Year and usually we promise to give people who buy an Annual Subscription between now and Dec 31st a full year bonus if our Trade of the Year doesn't make 100% before the renewal next year (you don't have to make the trade but you do have to subscribe), but this one is so cheap we'll simply guarantee that, by November next year, this trade makes at least $5,000 – or your renewal is FREE!

We'll talk more about it at today's Live Trading Webinar (1pm, EST) and we'll be watching those bounce lines to see if we're going to buy more longs like IBM, which has the potential to return 6,918% on cash (actually a credit), or whether we're going to add our SQQQ hedge – maybe with an IBM offset?