{kind=link}

We're making some progress.

We're making some progress.

As we noted yesterday, we were looking to take back 2,880 on the S&P 500 and we finished at 2,884 and our next goal is the strong bounce line at 2,910 – after which we can put this weakness behind us and get back to our rally – because nothing that happened last week to cause the sell-off matters this week, I guess…

Our bounce lines remain:

- Dow 25,000 is the mid-point and bounce lines are 25,550 (weak) and 26,100 (strong)

- S&P 2,850 is the mid-point and bounce lines are 2,880 (weak) and 2,910 (strong)

- Nasdaq 7,200 is the mid-point and bounce lines are 7,360 (weak) and 7,520 (strong)

- Russell 1,440 is the mid-point and bounce lines are 1,472 (weak) and 1,504 (strong)

We made good progress yesterday, flipping the Weak Bounce Line on the S&P green along with the Strong Bounce Line on the Nasdaq and the Russell is right on the Strong Bounce Line at 1,503 this morning, so we turn that black. That's all we need to do to see if we are moving in a healthy or unhealthy direction.

Yesterday's move up came courtesy of Chicago Fed Governor Charlie Evans who said: "As long as inflation continues to behave the way it has, I think we have capacity to pursue these accommodative stances in support of the economy and sustaining the expansion and maximum employment. There is a role for risk management, and you could take the view, as I have, that inflation alone would call for more accommodation than we’ve put in place with just our last meeting."

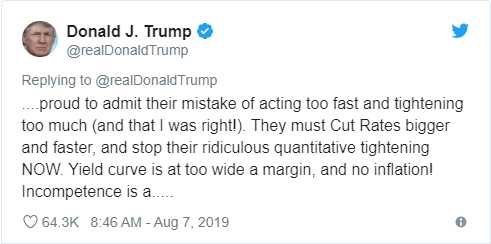

Evans is a voting member of the Fed so his doveish comments were taken as a very positive sign by the bulls but that makes us take this rally with a grain of salt as it's driven by words – not Fundamentals. There's no more Fed speak this week and just PPI tomorrow as far as major data goes but we do need to watch today's 30-year note auction as yesterday's 10-year note auction did not attract many bidders. If people lose interest in buying our debt at the rates the Fed sets – then we will have lost control of our interest rate policy – this is why the Fed needs to set REALISTIC rates, not rates that make the President happy.

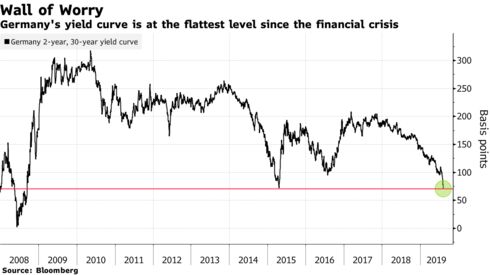

The entire Global Bond Market is showing signs of stress that usually indicate a looming Recession with Germany's Yield Curve falling to its lowest since the 2008 crisis. Germany’s entire curve is already fully below 0%, while even the 10-year bonds of some of the riskiest nations in the euro area — such as Spain and Portugal — are getting precariously close to negative (inverted) territory.

The entire Global Bond Market is showing signs of stress that usually indicate a looming Recession with Germany's Yield Curve falling to its lowest since the 2008 crisis. Germany’s entire curve is already fully below 0%, while even the 10-year bonds of some of the riskiest nations in the euro area — such as Spain and Portugal — are getting precariously close to negative (inverted) territory.

“Rates markets globally are expecting what looks like Armageddon,” said Tom di Galoma, managing director of government trading and strategy at Seaport Global Holdings LLC. “In our view, a recession is an 80% probability,” referring to the possibility of a U.S. contraction.

Trump, meanwhile, has been taking time out of his attacks on Black and Brown People to attack the White People at the Federal Reserve, indicating that he absolutely wants a weaker Dollar and lower interest rates because it's not about what's good for the economy in the long-term but what is good for the economy into next year's election, which Trump must win to stay out of jail on those obstruction charges and now we have Fed Governors like Evans, who want to be the Chairman, saying what they can to please the President.

Trump, meanwhile, has been taking time out of his attacks on Black and Brown People to attack the White People at the Federal Reserve, indicating that he absolutely wants a weaker Dollar and lower interest rates because it's not about what's good for the economy in the long-term but what is good for the economy into next year's election, which Trump must win to stay out of jail on those obstruction charges and now we have Fed Governors like Evans, who want to be the Chairman, saying what they can to please the President.

The bond kings at PIMCO are now warning us that US Treasury Yields may slip into negative territory next year, joining $14Tn worth of bonds around the World that already ask you to pay for the pleasure lending your money. In a blog post Tuesday, Joachim Fels, global economic adviser at the fixed-income investing giant, said it’s “no longer absurd to think that the nominal yield on U.S. Treasury securities could go negative.” At least 11 countries have negative 10-year yields, and Germany’s 30-year yield joined the rest of its curve below zero last week.

The bond kings at PIMCO are now warning us that US Treasury Yields may slip into negative territory next year, joining $14Tn worth of bonds around the World that already ask you to pay for the pleasure lending your money. In a blog post Tuesday, Joachim Fels, global economic adviser at the fixed-income investing giant, said it’s “no longer absurd to think that the nominal yield on U.S. Treasury securities could go negative.” At least 11 countries have negative 10-year yields, and Germany’s 30-year yield joined the rest of its curve below zero last week.

JPMorgan Chase & Co. strategist Jan Loeys last month said the global heap of negative-yielding bonds has a quicksand-like ability to engulf much of the fixed-income universe, including the U.S.

Bank of America U.S. rates strategist Bruno Braizinha, while not yet predicting negative U.S. yields, sees a risk that the 10-year falls into uncharted territory below 1% within a year as the Fed enters a recessionary-style rate-cutting cycle. “Yield is evaporating globally,” Braizinha said in an interview. By the end of 2020, a “Japanification scenario” — an extended period of low growth and inflation marked by extremely accommodative central bank policy — implies a 10-year yield in the 0.30%-0.60% range. And if the Fed returns the policy rate to zero, “10-year yields could go negative.”

Rates do need to stay low with Consumer Credit now topping $4.1Tn and $1.3Tn of that is "revolving credit", mostly credit cards, which rises with the rates set by the Fed. Even now, consumers are paying an average of 16.8% on that debt which is $218.4Bn a year that goes to our beloved Banksters on top of the Fixed Interest they collect on $1.6Tn worth of Student Loans and $1.2Tn of Auto Debt.

If rates keep going lower, pension plans and retirement plans will fail and no one will be able to get a good return on their money without gambling but, if rates go higher – a portion of the $4.1Tn is going to default and those who do struggle to pay their debts will see their disposable income rapidly shrink. These are all warning signs that we're nearing the top of the market but Trump and the Fed want you to party like it's 1999.