{kind=link}

Courtesy of Pam Martens

By Pam Martens and Russ Martens

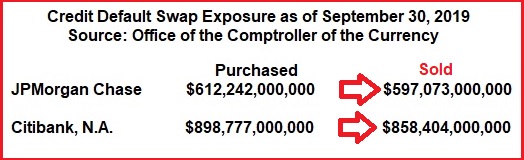

According to the most recent report from the regulator of national banks, the Office of the Comptroller of the Currency (OCC), JPMorgan Chase has exposure to $1.2 trillion in Credit Default Swaps while Citibank has exposure to $1.76 trillion for a combined total of $2.96 trillion as of September 30, 2019.

According to the same report, the total exposure to Credit Default Swaps among all national banks in the U.S. is $3.7 trillion – meaning that just these two banks are responsible for 80 percent of that exposure.

As of this past Friday, JPMorgan Chase had lost 39.3 percent of its common equity capital in the past five weeks while Citigroup, parent of Citibank, had lost 51.7 percent. That left JPMorgan Chase with just $256.68 billion in market cap versus Citigroup’s meager $79.86 billion.

One of our readers emailed us today asking if Credit Default Swaps were still around after they had collapsed Wall Street and the U.S. economy during the 2008 financial crash. Not only are these derivatives of mass destruction still around thanks to lapdog federal regulators and a timid Congress but two of the most dangerous banks in America have not just purchased protection through Credit Default Swaps, but they have sold protection (taken on the risk of a defaulting corporation or credit) to the tune of $1.5 trillion.

…