{kind=link}

"You try to reach a vital part of me

My attention span is dropping rapidly

It's all excuses baby, all a stall

We just don't get excited

Don't get excited" – Graham Parker

What are we, children?

First we endure two weeks of Fed speakers saying they think they might want to hike rates by 0.75% and then we treat Powell like our savior because he says 0.75% rate hikes are off the table – BUT 0.5 rate hikes are likely for each of the next two meetings. I'm pretty sure that 0.5% + 0.5% + 0.5% is more than 0.75% – twice as much, actually, yet the market reacted like the Fed just CUT rates. Powell is certainly the master of managing expectations…

Meanwhile, in reality world, the the BoE is experiencing everything the Fed fears: A divided policy decision (+0.25), Upside Inflation Risks, Downside Growth Risks, Inflation at 10.2%, GDP contracting in 2023. That timid rate decision sent the Pound plunging 1.5% this morning – the World's worst-performing currency – including Rubles.

Meanwhile, in reality world, the the BoE is experiencing everything the Fed fears: A divided policy decision (+0.25), Upside Inflation Risks, Downside Growth Risks, Inflation at 10.2%, GDP contracting in 2023. That timid rate decision sent the Pound plunging 1.5% this morning – the World's worst-performing currency – including Rubles.

With $32.5Tn in debt and a $2.2Tn deficit, the Dollar is the World's best-performing currency this year and that doesn't mean the Dollar is great – it just means the rest of the World is an even bigger disaster than we are. So yay US, I guess…

We were thrilled to see our Long-Term Portfolio (LTP) gain 10% on Powell's speech but then we gained another 5% into the close and that was just silly. Not that we're complaining, thank you Mr. Powell, but we do know that this rally was based on BS and the volume (140M on SPY) was not at all impressive after 1.1M shares traded on the way down from 447 on the 20th to yesterday's 417 open (6.66%). Now we're back to 429 – half recovered and, as we expected in yesterday morning's report, now we'll have to wait to see what sticks.

As you can see from the chart, that's half of our RECENT drop that we recovered, not half of the 20% retrace from 4,800 to 4,000. And, I say retrace, not drop as a DROP would be 0.2 x 4,800, which is 960 points to 3,840 but, according to our 5% Rule™, 4,000 is the correct major support for the S&P and 4,800 was simply an overshoot by traders who did, in fact, get too exited. That means the move back to 4,000 is a CORRECTION – meaing we are heading back to the correct level – it may be quite a while before we see 4,800 again.

If 4,000 is our correct level then our correct trading range is likely to be 3,200 to 4,800 (20% either way) for years to come. I don't think we'll see 3,200 unless Putin does something very naughty or Covid comes back hard because the Fed and our soon to be elected Government are very unlikely to let that happen and, since Biden has cut the Defict to $2.2Tn from $3.5Tn last year – we've got $1Tn left to play with for emergencies.

Some might say that running even a 10% of your GDP deficit is probably unsustainable but those people understand finance and are not welcomed in our Government anymore.

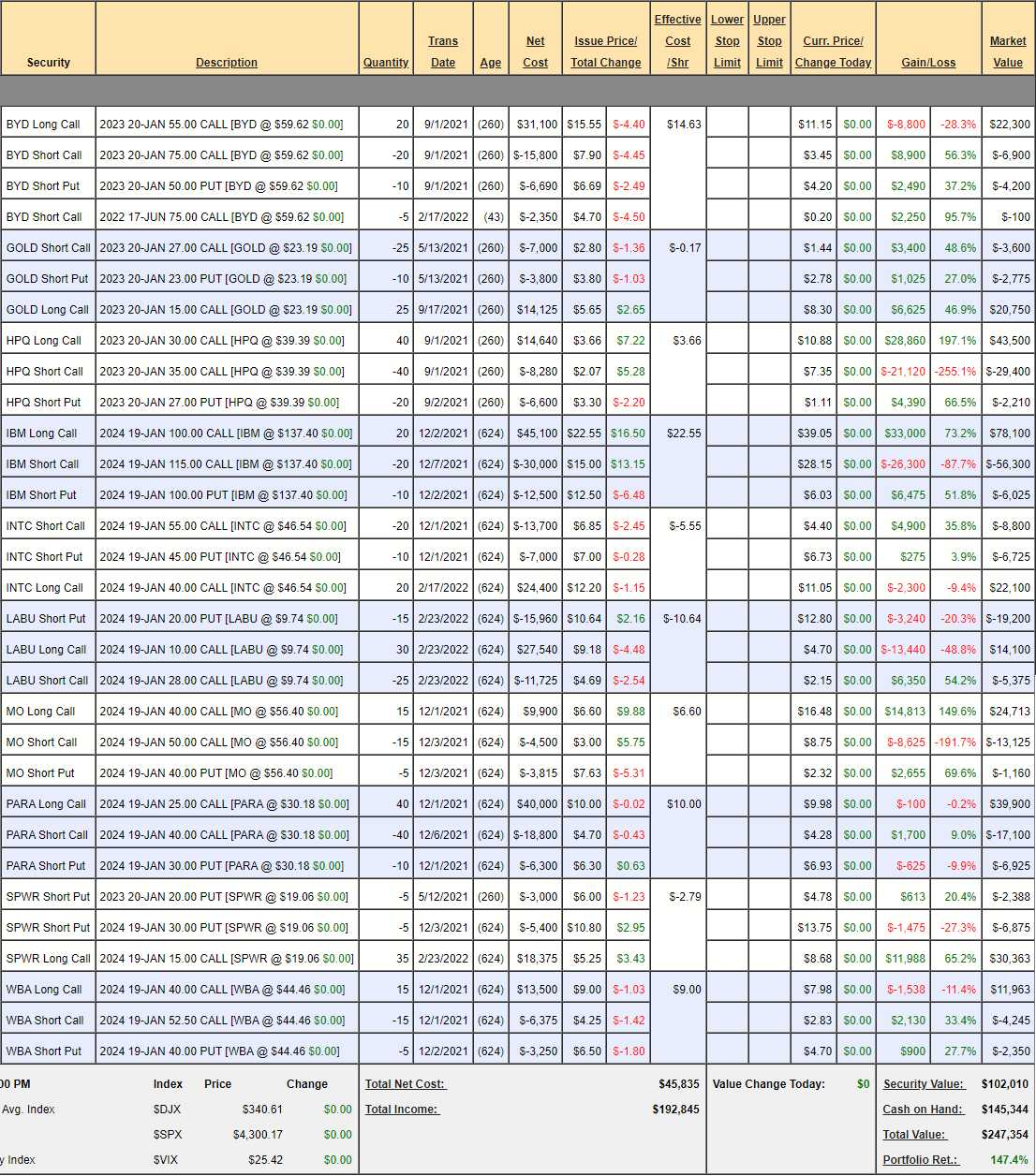

My favorite indicator, other then our LTP/STP, to see if we are feeling the market correctly, is our Money Talk Portfolio, which we don't touch unless we're appearing on the show (which I will be soon). February 16th is the last time we made changes to that portfolio and we were up 140.9% at the time, when we adjusted BYD, INTC and SPWR and, unfortunately, added LABU, which is dragging down the portfolio at the moment.

The S&P 500 was at 4,455 that morning and this morning we're at 4,255, down about 5% but the untouched portfolio is at $247,354, up 147.4% from our $100,000 start back on November 13th, 2019 – right before Covid hit. Here's a quick look at where we stand on those positions:

LABU is, in fact, our only net loss out of 10 positions so we'll take 90% and I think Biotech is ridiculously oversold. We played this quarter defensively (and it's now obvious why) but, if we can retake that strong bounce line at 4,320 – I'd be inclined to get a bit more aggressive with our $145,000 cash pile. If we fail to hold 4,000 however – I'll be looking to cash out and switch to a pure short-put strategy until we see a market bottom.

LABU, for example, has a net $10,330 loss but we can kill that position and flip to selling 20 of the 2024 $10 puts for $5 ($10,000) and then we get our money back if LABU just gets back over $10 in two years. You can apply that strategy to winning positions as well, where your worst case is owning stock AFTER another 40% drop and that's how we set up the first leg of our next round of trades – if we are going to get defensive.

We'll see what levels stick after tomorrow's Non-Farm Payroll Report. Losing that weak bounce line (4,160) on the S&P will get us quickly back to hedging but, as long as we can hold it – hope springs eternal.