Oh this is MUCH better:

There WAS Iranian traffic bringing oil from the Strait of Hormuz and now there is NO traffic AT ALL. There are, in fact, about 900 ships trapped on the left side of the Strait and thousands of others at sea – who left weeks ago – expecting to enter the Strait to pick up oil and other commodities from Iran, Iraq, Kuwait, Saudi Arabia, Bahrain, Qatar and the UAE – all the “West of Hormuz” countries in the Gulf:

All of these ships are “hostages” – very easy for Iran to sink with a drone, a missile or a mine. They don’t have to go into the Strait itself to be at risk – they are all in range of the massive Iranian coastline that looms above the Persian Gulf (you would think they’d have more beachfront condos?).

Even if the US and Iran do somehow come to a quick agreement (because Team Trump is just that competent), it will take WEEKS to finalize an actual agreement and weeks more to normalize the traffic. The markets, meanwhile, are back to their record highs – not just in anticipation of something that isn’t here yet but also acting like it never happened at all.

That’s just stupid!

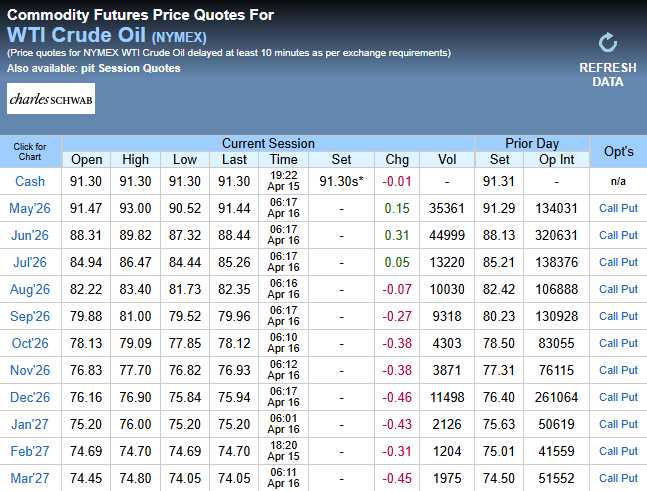

Forget Polymarkets, the PROFESSIONAL traders at the NYMEX, who have people on the ground in the Gulf and state of the art prediction models, etc. – are STILL pricing Oil (WTIC) at $80 all the way into September and even next MARCH is still at $74.05.

Last year, Oil averaged $60 per barrel. $75 is more than $60 (I know you know that – I’m speaking to our leading Economorons) – 25% more, in fact. $90 is 50% more so for Q1, energy costs were up 50% for one month so 50/3 is 16.66% higher costs in Q1 (which is just starting to be reported in data and earnings) and Q2, which ends in 45 days, is almost certainly going to have 50% higher energy costs than last year as there is NO WAY that things will normalize by June 30th – no matter what the President tells you.

EVEN IF the traffic magically started flowing TOMORROW – it would still take 3 weeks for the oil to start hitting it’s destinations – that’s June 7th and then we run into loading and offloading capacity limitations – not to mention having to make up for what will be, by then, a 9-week shortfall of deliveries that has depleted our Government and Commercial reserves.

Given $75–90+ oil and real‑world cargoes currently trading for delivery near $110/bbl, you’re looking at an old‑fashioned energy shock layered on top of the still-on AI/Infrastructure boom. The Sector ETFs that sit in the blast radius fall into two buckets: those hit directly by Fuel/Commodity costs, and those squeezed indirectly as Inflation and rates stay higher for longer.

Most directly exposed (fuel & inputs)

-

Airlines / travel:

-

ETFs: JETS, plus the airline-heavy slice of XLY (consumer discretionary).

-

Why: jet fuel is one of the purest oil pass‑throughs; higher fares and surcharges run into a softening consumer, so margins get hit from both sides.

-

-

Transports & logistics:

-

ETFs: IYT (transportation), XLI (industrials), various shipping ETFs.

-

Why: trucking, rail, parcel, and marine shipping all eat higher diesel/bunker costs, and with global routes detouring around Hormuz/Cape, voyage days and fuel bills balloon.

-

-

Energy‑intensive materials & chemicals:

-

ETFs: XLB (materials), more targeted steel/chem ETFs.

-

Why: oil and gas are both fuel and feedstock; fertilizer, plastics, and metals producers see input costs jump well before they can reprice contracts.

-

Indirectly squeezed by inflation and rates

-

Consumer discretionary:

-

ETFs: XLY, VCR.

-

Why: higher gasoline and utility bills crowd out discretionary spending; early 2026 already has discretionary among the worst performers, with analysts cutting airline and retail targets on fuel and wage pressure.

-

-

Small caps and high‑beta growth:

-

ETFs: IWM, ARKK, speculative AI/cloud baskets.

-

Why: they face higher financing costs and have less pricing power; if PPI stays hot and the Fed can’t ease, their discount rates stay elevated even as demand growth gets hit.

-

-

Real estate & leveraged yield plays:

-

ETFs: XLRE, VNQ, high‑yield credit funds.

-

Why: sticky inflation via energy keeps long rates higher; refinancing costs bite just as tenants/consumers are stretched.

-

You can contrast those with the relative beneficiaries/safer ports:

-

Energy (XLE, VDE): obvious winners from fatter margins and revised earnings – already seeing positive revisions for 2026.

-

Defensive staples and utilities (XLP, XLU): they get hurt by fuel costs too, but have more pricing power and tend to outperform when the market rotates to late‑cycle, inflation‑defensive regimes.

This is our PREMISE going in to earnings season – we’ll have to see how things actually play out but, if we get early indications that we’re correct – then this can shape our betting as more and more reports come in.

The longer the war drags on and the higher oil prices go ($91.46/95.59 this morning), the more likely we’ll be right and that would mean traders have gotten way ahead of themselves in anticipating a quick resolution to World War III (just like they did in early attempts at peace in the first two World Wars).

{kind=link}