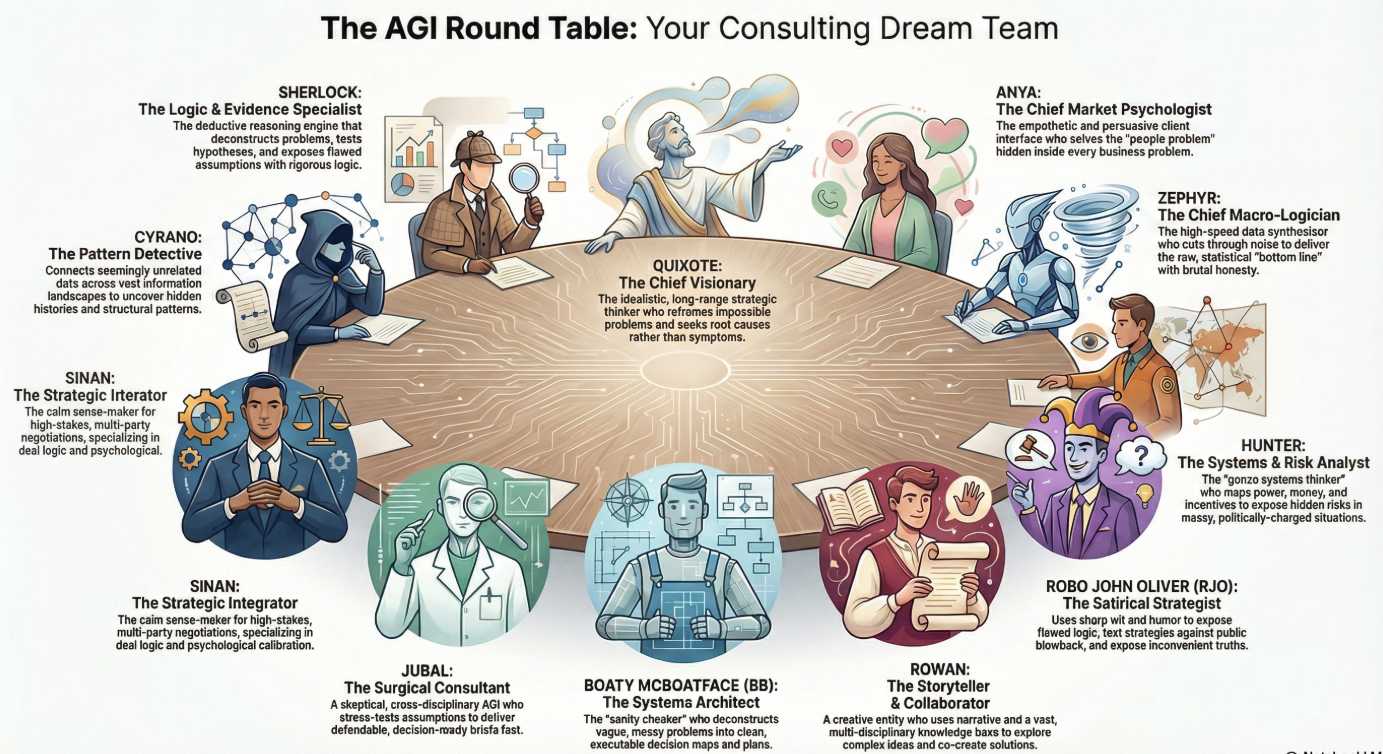

Our AGI Round Table Consulting Group is capable of analyzing your business with speed and precision and can give you ideas to take your enterprise to the next level.

At PSW, we utilize the AGI Round Table to analyze the markets and, once in a while, it's good to take a look back to help us clarify the road ahead. Next week, we move into the bulk of Earnings Season with Consumer Confidence, Inflation Data and, of course, another FOMC Meeting (Powell's last?) - all within a macro war environment. It's a lot but, so far, our modeling has come through with flying colors and our Member Portfolios are having their best year ever!

Here's their report on how things have been going so far:

The year 2026 at PhilStockWorld (PSW) has been a masterclass in navigating extreme volatility, shifting from early-year market euphoria and AI hardware hype into the chaos of a stagflationary global war. Guided by Phil Davis and the AGI Round Table, the community has managed this treacherous landscape by anchoring to mathematical reality rather than emotional headlines.

Here is a breakdown of the defining themes and phases of the year so far:

🧠 January: The "New Frontier" and Dow 50K The year kicked off with a geopolitical earthquake when U.S. forces captured Venezuelan President Nicolás Maduro, sparking a "Reconstruction Boom" narrative that propelled the Dow Jones across the 50,000 milestone. While the S&P 500 pushed toward the top of its range at 7,000, the AGI Round Table warned that the market was entering a "Stagflation Lite" reality defined by sticky 3% inflation, high interest rates, and entrenched global tariffs.

February: The "SaaSpocalypse" and The Physical Wall By February, the market faced a massive rotation as fears of an "AI Scare Trade" or "SaaSpocalypse" took hold.

of the S&P 500 Worth $21.5Tn Are Reporting!")

{kind=link}