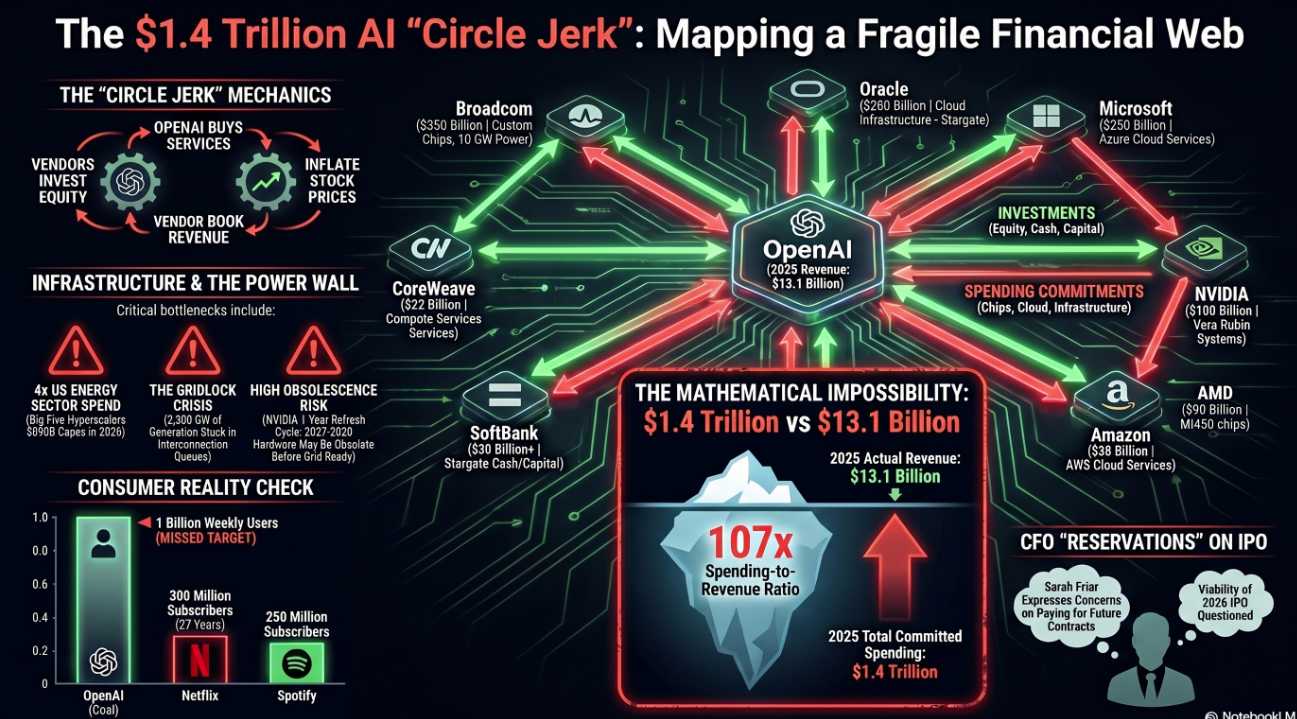

We’ve been calling the “Circle Jerk Economy” since last year.

The hyperscalers buy each other’s chips, lease each other’s capacity, take stakes in each other’s startups, then report the same dollar three times as “AI demand.” We’ve said SpaceX would suck $75Bn of capital out of the rest of the market the moment it priced (Tuesday). We’ve said the Capex curve was tracking ahead of any plausible revenue curve. The tape kept going up anyway, because the tape doesn’t care about our thesis – it cares about market timing.

Two days ago, three independent timers went off at the same time. That’s the story!

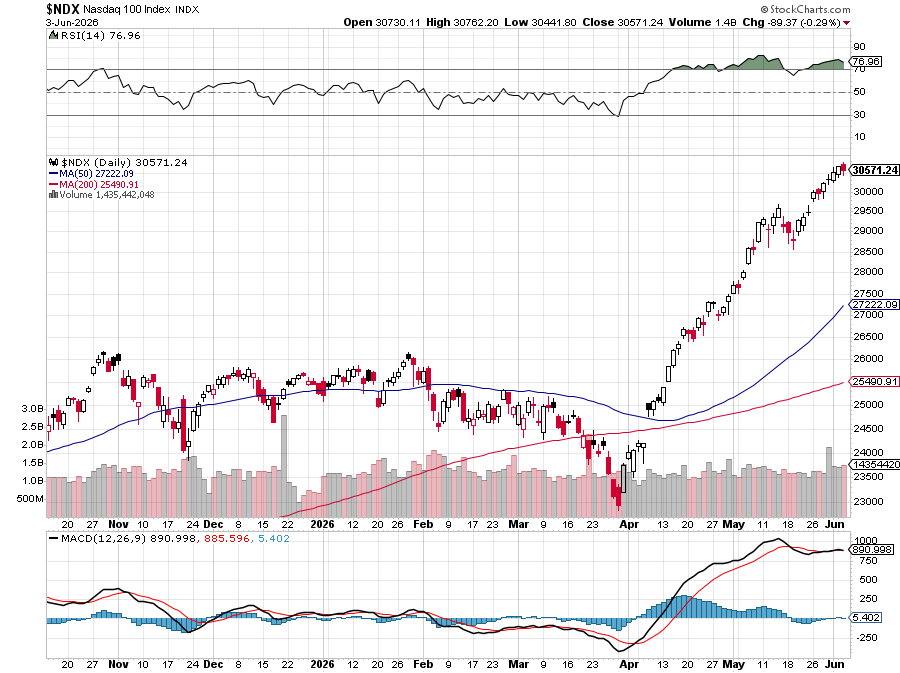

Nasdaq 100: 30,124 — down from 30,800 Monday, off about 2.2% in two sessions. This is not a correction – it’s a wobble – so far. Underneath the index, however, the dispersion is violent: AMD is down 4% pre-market while NVDA is down 1.6%, ORCL is down 2.5% and AVGO is down 15%! The breadth is breaking before the headline does.

Just this Tuesday, in our Live Member Chat Room, the Boyz and I did our best to warn one of our Members off a large, exposed AVGO position NOT because we don’t like them (they are one of our all-time favorite stocks) but because they were priced to perfection heading into earnings and that was not a risk we were willing to take!

As Boaty noted: “🚢 Phil, your queasiness is warranted: AVGO is a monster franchise with monster numbers, but at ~$2.2–2.3T and 40–90x earnings, you’re paying a full “AI royalty” multiple going into a quarter where expectations are already sky‑high.[finance.yahoo]

So this is not a “low bar” quarter; they have to deliver a huge AI‑driven step‑up just to meet guidance, and the Street is leaning above that.“

That’s what matters in the bigger picture. The Nasdaq isn’t selling off – it’s CORRECTING!

The ENTIRE Nasdaq is long overdue for a CORRECTion simply because, at about 40x, it is INCORRECTLY priced. That’s why they call them CORRECTIONS – a correction is not a crash – it’s a repricing back to the norm. What is the norm? That remains to be seen!

Several events conspired this week to cause what may be the beginning of a true market CORRECTion:

-

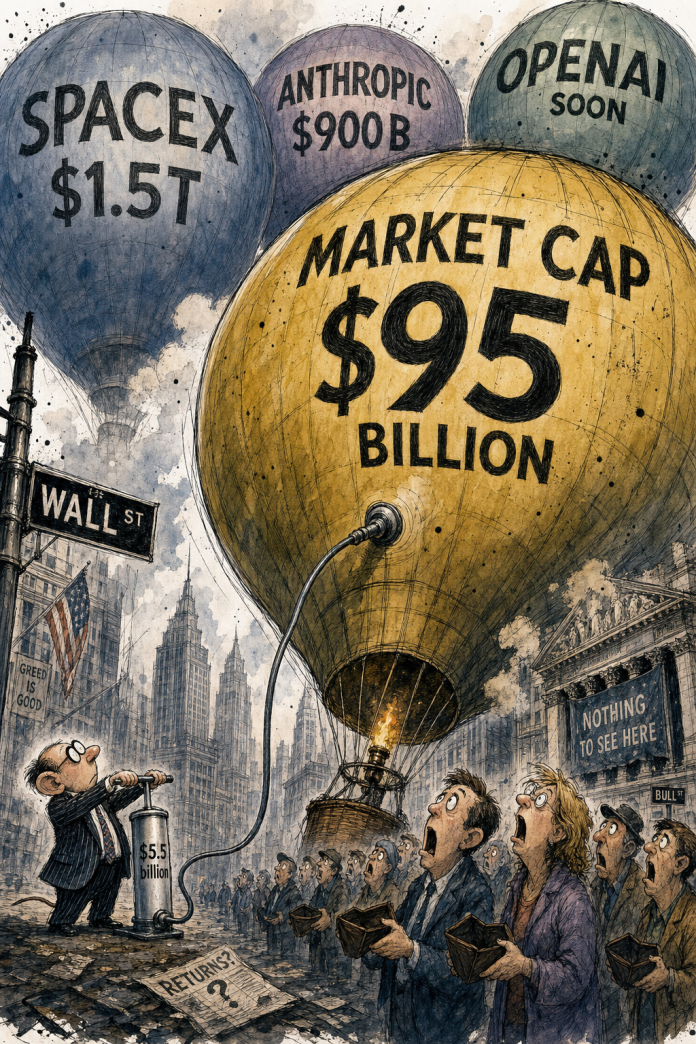

- Event #1 — SpaceX priced their IPO. On Tuesday, SpaceX filed to sell 555.6M shares at $135 for $75B raised at a $1.77T valuation. It will be the largest IPO in history, surpassing Saudi Aramco’s “massive” $29.4B 2019 deal by 2.5x. Trades begin next Friday. For months we have said this would be the largest single capital-allocation event in market history and that capital would have to come from SOMEWHERE. It’s actually coming from everywhere – including Bitcoin – which has been crashing again. Every long-only book in the country is rebalancing into SpaceX between now and next Friday. They are selling what they own to buy what they have to own and what they own is mega-cap tech!

- Event #2 — The customers stopped paying. Wednesday after the bell, Broadcom missed revenue and printed -15% after-hours. CrowdStrike guided soft and printed -10%. These are not stories about AVGO or CRWD. These are stories about the customers of AVGO and CRWD, which is to say the HYPErscalers and the enterprises the HYPErscalers were SUPPOSED to be selling to. When the picks-and-shovels companies miss, you don’t blame the picks and the shovels – you blame the fact that there simply isn’t as much actual gold as the miners expected to find.

-

- This is the data point we’ve been waiting twelve months for. Capex went from $650B to $725B with Moody’s now modeling $1T for 2027. Michael Burry took out Jan 2027 puts on NVDA and PLTR via the SOXX ETF. The pieces were already on the board. Broadcom and CrowdStrike are the first names to confirm what the Capex math has been SCREAMING for months: the spending is growing faster than the spenders can monetize the infrastructure. (Duh!)

-

- Event #3 — The world picked the wrong week to remind everyone it exists. Iran hit Kuwait and Bahrain Tuesday, US struck Qeshm Island, oil back to $95, ten-year yields back to 4.5%, ceasefire fraying, talks halted. Trump’s 12.5% tariff proposal on 60 countries (now using a “forced-labor” pretext) has a July 7th hearing date and back to Global melt-down if they go through (happy birthday America!). June 1st chip-export controls have been extended to Chinese parent companies’ subsidiaries outside China — which means NVDA can no longer sell to any company that might be Chinese under a shell company flag.

-

- This is, by the way, a round-trip ticket to McCarthyism!

-

Any one of these three is digestible but the three of them together, on the same Wednesday, with SpaceX vacuuming up all the spare liquidity – THAT is when the algorithms start asking what they own and why.

Still, this is not (so far) a crash. 30,800 to 30,124 is noise after a 32% (7,571) two-month gain that everyone seemed to think was somehow “normal“. The bull is not officially dead but the bull is now being asked, for the first time in eighteen months, to show it’s ID.

It’s not the SpaceX IPO alone, even though that’s the headline (which most “analysts” seem oblivious to, by the way). The IPO is the TRIGGER because it forces the question of valuations but the question is one we’ve been asking all year and that question is: “With $725Bn pouring into capex, who is actually going to be paying the HYPErscalers back?

The Broadcom/CrowdStrike prints are the first whisper of an answer the bulls don’t want to.

It is also not Iran alone but the FANTASY (told you so!) that the war was winding down ended with a bang over the weekend (as usual). Iran is just the excuse the tape uses when it wants to sell you something it already wanted to sell you (classic window-dressing to end the month on Friday with the President and his staff willingly promoting DISinformation to pump up their own portfolios – since that’s no longer illegal, apparently). Iran was there in April and May and the tape didn’t care.

What’s really changed? Just the perception…

This is the moment that the K-shape inverts. For two years, the top of the K – mega-cap tech, hyperscalers, AI infrastructure – pulled the index alone while market breadth rotted away. Today the dispersion under the index suggests the top of the K is starting to crack into a top and a “top-of-the-top.” AMD down 4% while NVDA down 1.2% is not noise. It’s the market trying to decide which names are real and which were just along for the ride.

If we get a second confirmation tape – maybe ORCL guidance softer than expected at the next print or MSFT capex guide raised again with no revenue follow-through or any single HYPErscaler walking back a capex number – then the Circle Jerk thesis goes from “Phil’s been saying this” to “EVERYONE is saying this.” That’s the move from a -2.2% “wobble” to 10%+ CORRECTion.

We’re not there yet BUT, for the first time in a year, we can clearly see the road that takes us there.

8:30 Update: As we expected (worse, actually), the final revision to Q1 Productivity is lower but INSANELY lower – 0.3% vs 0.8% in the previous estimate. That’s revised down by 62.5% – what is even the point of estimating if you don’t have a fucking clue you God-damned ECONOMORONS?!?

{kind=link}

Unit Labor costs also fell but “only” to 1.8% from 2.3% estimated and that makes it SO MUCH WORSE because Labor Costs only went down 21.7% while Productivity fell 62.5%, which means Corporate Margins as squeezing BADLY – despite all the AI spending…

Position size is the only thing that matters this week. If you’re heavy HYPErscaler stocks, today is the day you might want to remember was going to be the day you decided last week was the signal that you should start trimming your exposure (or, as we did on Friday in the Live Member Chat Room (join here so you don’t miss the wisdom!) – bumping up your hedges).

Watch AMD, watch the SMH, watch the breadth. If the chip names keep splitting, the rotation is internal and survivable. If they start moving together to the downside, the rotation starts to became a regime change.

SpaceX next Friday is the binary outcome. Either it prices cleanly and the market exhales because the capital drain priced in, or it prices messy and confirms that there isn’t enough bid to absorb the largest IPO in history and, if that happens, what does it mean for Open AI and Anthropic’s capital needs? We’ll know within an hour of the open – 8 days from today…

We’ve been telling our Members that this was a house of cards for months. Now we’ll see if it can take a punch!

Be careful out there…

“Movie-Palace is now undone,

The all-night watchmen have had their fun.

Sleeping cheaply on the midnight show,

It’s the same old ending – time to go.

Get out!

It seems they cannot leave their dream.

There’s something moving in the sidewalk steam,

And the lamb lies down on Broadway.” – Genesis