Crazy week ahead!

We did a special Global Status Report for our Members this weekend, so I won’t waste time reviewing that here. Instead, lets dive right into what’s going on this week, starting with Earnings, which are coming at us fast and furiously (and they made 13 of those!). Verizon (VZ) just raised guidance this morning – so that’s off a to a good start and Qualcom (QCOM) is also jumping 13% after Warren picked them for our Members on Friday.

As Warren said Friday morning:

“Deploy your capital surgically into grounded value plays like QCOM before the crowd realizes where the real AI edge is moving.“

There are HUNDREDS of great opportunities still sitting around for us and, of course, we already have our Watch List (s), which featured stocks like AMAT, AVGO, CEG (still playable) and DUK as the first 4 picks but there are 200 other stocks on that list that our Members can keep going back to the well for and, of course, we constantly refine our choices as situations develop (like the war, for instance).

In fact, on March 15th, we did an educational post called “Retirement Income Strategies 101” where we illustrated low-margin, CONSERVATIVE plays that were good for building an income-producing retirement portfolio with and, despite war, here’s a quick rundown after 6 short weeks:

- STLA – Up $350 (10.9%)

- STLA – Up $450 (7.2%)

- GEO – Up $1,860 (15.5%)

- T – Down $368 (-3.1%)

- EBF – Up $240 (7.2%)

- HST – Up $555 (5.9%)

- TGT – Up $420 (4.2%)

- F – Up $70 (1.1%)

That’s already up $3,577 on $68,702 we deployed is 5.2% in 6 weeks and there are 52 weeks in a year so this BORING, conservative deployment of capital is on track for better than 40% annualized returns. Worth paying attention to?

We will do a full update in June but that’s going pretty good – especially considering these crazy war-driven markets.

That brings us to the data portion of today’s discussion and this week is CRAZY! as we have $524,000,000,000 in Treasury Securities being sold off this week including $69Bn in 2-year notes at 11:30 today followed by $44Bn in 5-year notes at 1pm and tomorrow at 1pm, they are selling $44Bn in 7-year notes. Wars are expensive!

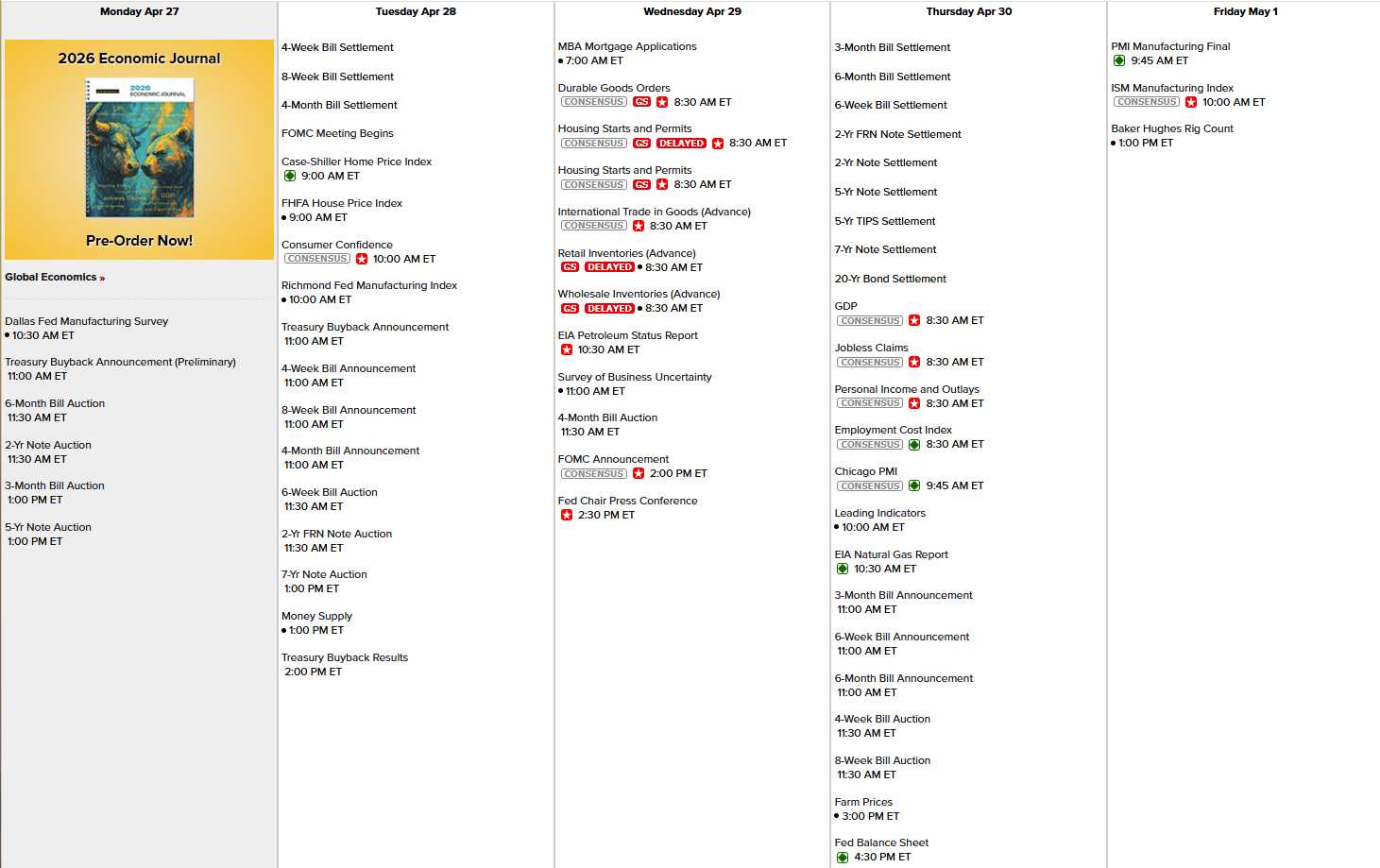

As you can see, we’ve also got the Dallas Fed this morning, Consumer Confidence, Richmond Fed and Housing Data tomorrow. Wednesday is Durable Goods, Business Uncertainty and the Fed Decision (during weekly Live Webinar for our Members), Thursday is Q1 GDP, Personal Income & Spending, PCE and Chicago PMI and Friday is PMI & ISM (we don’t get Non-Farm Payroll until next Friday).

So busy, busy, busy but Wednesday evening is MSFT, META, AMZN, GOOGL and QCOM (not to mention SOFI – who we’re long on in the morning) and AAPL is Thursday night so what a week this is going to be!

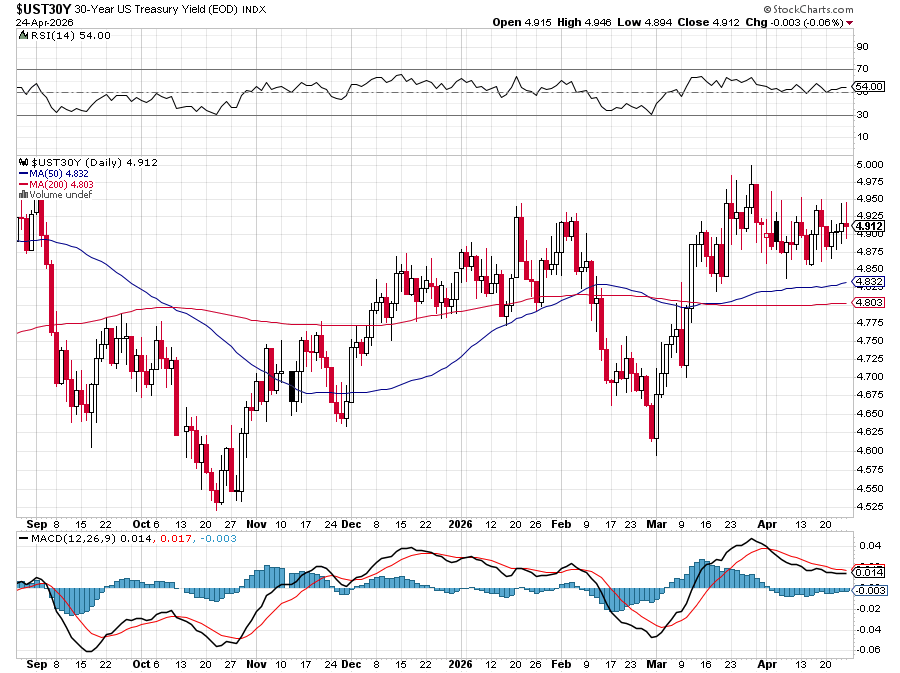

The Fed, meanwhile, is widely expected to leave rates alone on Wednesday afternoon but keep an eye on those 30-year rates as they are consolidating under that critical 5% line – ready to pounce…

The rest of the World’s Central Banksters are basically sitting on their hands and hoping the Iran/Oil shock doesn’t undo the last two years’ worth of tightening efforts. The Fed’s March “Dot Plot” still only showed a single cut penciled in for 2026 with 7 members expecting no cuts at all this year and the other 7 expecting just one.

That implies the long‑run Fed Funds Rate has crept up toward the low‑3s, which is the Committee’s way of saying “3½–3¾ isn’t as tight as it used to be in our models – don’t count on racing back to 2% any time soon.”

Futures and betting markets have caught up to that reality since the last Fed meeting. As recently as February, the street was dreaming about two cuts this year but, after the Iran war and the oil spike, Fed Funds Futures now price in AT MOST one cut and only late in the year and possibly no cut at all if the war continues and inflation does not calm down.

The ECB left their rates unchanged in March and raised its 2026 Inflation Forecast to 2.6% – explicitly citing higher energy costs from the Iran conflict. They say they’d like to eventually cut but are in “wait‑and‑see” mode until the war fallout is clearer. The Bank of England also held at 3.75% and now expects UK CPI to spend much of this year above 3% instead of dropping to 2% in the spring as previously hoped – again blaming war‑driven energy and food.

So the global message is: “We thought we were almost done; then Hormuz blew up our models.”

On the inflation side, the data they’re looking at aren’t exactly soothing:

US March CPI jumped to about 3.3% year‑on‑year from 2.4% as Energy prices spiked nearly 11% in a month. Headline PCE is estimated to have climbed to roughly 3.4–3.5%, driven by the same oil shock. The Fed’s comfort blanket is that Core Inflation has kept drifting lower: estimates have core PCE running in the high‑2s to low‑3s now and trending toward roughly 2½% by year‑end if you strip out the immediate war/tariff noise (as if that is going away soon!).

This week and next, they’ll be sweating every line of the numbers we’re about to get:

Thursday’s PCE (their preferred gauge) is expected to show headline re‑accelerating on Energy but they’ll be laser‑focused on whether core PCE stays in that 0.25–0.30% month‑over‑month range that’s barely consistent with 2% over time.

Next week’s jobs and follow‑on inflation prints will tell them whether the Iran shock is a one‑off level shift in prices or the start of a stickier second wave with sulfur/fertilizer/food now joining oil in the pressure cooker. So, when we say “watch those 30‑year yields,” what we really mean is:

-

- The Fed’s dots say “maybe one cut”

- The ECB and BoE are frozen

- The markets are now leaning toward ‘no hurry to ease’

- Headline inflation is being re‑energized by war – even as core drifts down more slowly than anyone would like.

That is NOT the recipe for a gentle, low‑volatility Treasury market. It’s a set‑up where any surprise: A hotter PCE, a bad auction or one hawkish Powell sentence – can spike that 30‑year right back over 5% – just as we’re trying to digest half a TRILLION Dollars in new paper and a week’s worth of mega‑cap earnings.

Be careful out there!

{kind=link}