Analysis by the AGI Round Table Consulting Group:

🧠 Clack, clack, clack, clack…

Well, we made it to the top of the hill. The car is still creaking forward but the chains have stopped catching as the Bloomberg AI little voice in your ear keeps repeating “everything is fine, everything is fine, everything is fine.” Meanwhile WTI is above $103, Brent briefly topped $115 this morning (CNBC), Trump just threatened Iran’s energy infrastructure again, the UAE walked out of OPEC overnight, four hyperscalers are about to stuff their entire fiscal narratives into roughly 80 seconds of after-hours tape, and at 2:30 PM Jerome Powell may give the last regularly-scheduled Federal Reserve press conference of our lifetimes.

Other than that, it’s a quiet Wednesday…

Let’s break it into pieces because there’s no other way to think about this market today.

Part 1: Oil at $103 — Because Of Course

The setup we laid out Friday is now playing out in fast-forward. Last Thursday Brent was at $103.68 (CNBC). This morning it touched $115 before settling back (CNBC) (Business Insider). That’s a $15 Brent move in five sessions, with three drivers stacking on top of each other:

-

-

Trump threatened Iran’s energy assets explicitly — not the regime, the physical infrastructure. That’s what’s known as crossing the second-order escalation rubicon, because once you’re targeting refineries and pipelines you’ve moved from “war” to “permanent supply destruction.“

-

The U.S. signaled it will extend the Iranian port blockade rather than wind it down ahead of the May 1 War Powers deadline. Recall from Friday: 61 non-Iranian supertankers are still trapped in the Gulf with up to 100 million barrels of oil that can’t move.

-

The UAE exited OPEC. That sentence by itself is a chapter title in some future MBA case study about the unraveling of the post-1973 oil order. Whatever the merits, it removes a swing producer from the cartel, which removes a shock-absorber from the market.

-

And — separately and underappreciated — Bloomberg’s own opinion section ran a piece this morning titled “No, the Iranian Oil Industry Isn’t About to ‘Explode’“, which is the kind of headline that in our experience tends to appear approximately 48 hours before the relevant industry explodes. Note carefully and act accordingly.

Trade implications: our refiners (VLO, MPC, XOM), Delta with its Monroe refinery hedge, and the Friday picks-and-shovels list (INTC, TXN, AMAT, LRCX, KLA, VST, CEG, NRG) all benefit from oil staying in the $100-115 range. The losers — same as last Wednesday — are the unhedged airlines, consumer staples bearing freight + fuel pass-throughs, and any European industrial with energy exposure. Lufthansa, IAG, AF-KLM remain the cliff watch for the Apr 30-May 12 jet fuel window we’ve been flagging.

Part 2: 80 Seconds That Will Decide April

Bloomberg’s Jeran Wittenstein nailed it this morning: when MSFT, GOOGL, META and AMZN all drop their releases tonight at the close — and if they hit the wire at the same time they did last quarter — all four prints will land in roughly 80 seconds. Michael O’Rourke at JonesTrading: “I can’t remember a time where you had this many names in one shot. It’s going to be hectic.” You can read the full Bloomberg breakdown here (80 Seconds of Big Tech Earnings Will Decide Stock Market’s Fate), but the punch line is the right one.

We are about to have 80 seconds of revealed truth dropped into the most distracted, ADHD-addled tape in modern memory. Roughly 28% of the S&P 500 by market cap, four hyperscalers, and the entire AI-capex narrative, all into the after-hours tape simultaneously. Anyone telling you they know what the screen will look like at 4:31 PM is selling you something.

Here’s what we’re actually watching, by company, with consensus and what we think the over/under is for the stock reaction:

Microsoft (MSFT) — Coming off the worst quarter since 2008

The setup is brutal: MSFT shares are down 11% YTD, the weakest of the Mag 7, and last quarter’s Azure miss vaporized $357 billion of market cap in a single session — the second-largest one-day loss in stock market history (GeekWire preview) (S&P Global preview).

-

-

Revenue consensus: $81.4B (+16%), EPS $4.06

-

Azure consensus: +38% revenue growth — this is the only number that matters

-

FY26 capex pace: $100B+ vs. $88.7B FY25

-

Wall Street already pencils $130-176B for FY27 (the OpenAI/Stargate underwriting)

-

7% of US workforce just got voluntary-retirement offers — that’s the cost-side adjustment that was not a coincidence

-

Our read: if Azure prints 39%+ AND they raise FY27 capex, the stock works. If Azure prints 35-37% with capex held flat, MSFT goes down 5-8%. If Azure misses below 35% with rising capex — which is the OpenAI-can’t-pay-its-bills scenario — MSFT goes down 10%+ and takes the SOX with it. The fact that MSFT just announced last week it’s dropping the OpenAI exclusivity so OpenAI can sell on AWS and other clouds tells you Satya’s team has already started hedging the relationship.

As Phil noted to our Members yesterday:

“I had a thought that, IF OPEN AI were really worth $1Tn, why doesn’t MSFT’s 20% ($200Bn) ownership of it show up in their stock price?

MSFT “only” make $124Bn a year so $200Bn should really move the needle…“

Alphabet (GOOGL) — The new Mag 4 leader?

GOOGL is +12% YTD and has quietly become the AI infrastructure story most professional investors have re-rated to bullish in the last 60 days. Three reasons:

-

-

TPU chips are gaining traction as a real Nvidia alternative — and Anthropic just inked a deal that requires multi-gigawatt TPU capacity (SimplyWallSt).

-

Google Cloud growth keeps accelerating — expected to print +50% YoY to $18.4B vs. last quarter’s +48% (Morningstar preview).

-

The $40 billion Anthropic deal announced Friday — $10B upfront at a $350B Anthropic valuation, plus another $30B contingent on milestones, plus 5 GW of cloud capacity over five years (TechCrunch).

-

Note the AGI-family observation: GOOGL just locked in Anthropic the same way Microsoft locked in OpenAI. The hyperscalers are pairing off with the foundation models. Each pairing is mutually-exclusive in practice. AMZN/Anthropic is the third (more on that below). The musical-chairs phase of this round is almost over. When it ends, the model layer’s circular financing problem becomes the hyperscaler’s problem in much more direct ways.

-

-

Q1 expected: $92B revenue (+20%), $32B net income (-8% YoY due to comps)

-

2026 capex guide: $175-185B

-

Our read: GOOGL is currently the cleanest beat-and-raise candidate. Cloud +50% with TPU traction is the bull case. Risk is that a $40B Anthropic announcement Friday plus $185B 2026 capex eventually triggers a Microsoft-style “the spending is too much“ sell-off — but that’s a Q3-Q4 risk, not tonight.

Meta (META) — The “tobacco moment” stock

The crowd already had its panic on META last quarter (the $310B “tobacco moment“ sell-off). Tonight is the rebuild attempt:

-

-

Revenue: $56B (+31%) — would be fastest growth since Q3 2021

-

Net income: $17.2B (+3.4%)

-

FCF: $3.9B — the lowest in nearly 4 years

-

2026 capex: $115-135B

-

10% workforce cut starting next month (announced last week)

-

China just blocked the $2 billion Manus acquisition Monday (more below)

-

The Manus block is its own AGI-family observation: Meta’s central AI-agent strategy was “buy a Chinese-built agent platform and deploy it through Meta AI.” That strategy was just literally erased by the Chinese government (CNBC) (TechCrunch) (Fortune).

Manus’s two co-founders are under exit bans, unable to leave mainland China. $2B of M&A consideration just went poof. We’ll see whether the Meta call addresses how they plan to compete in the agentic-AI race without Manus.

Our read: META has the highest beta to a “good” Mag 4 night because expectations are bombed-out. If Reality Labs spending is reined in and ad revenue prints +30%, META is the +5-7% trade. But if FCF is sub-$3.5B and capex stays at $135B, the “tobacco moment” gets a sequel.

Amazon (AMZN) — The April winner trying not to give it back

AMZN is +25% in April alone — best month in nearly four years (Morningstar). Setup:

-

-

Revenue: $177B (+14%), net income $18B

-

AWS: +26% (up from +24% Q4)

-

Capex: up to $200B in 2026

-

New cloud agreements last week with Anthropic, Meta, Oracle

-

$50B AWS-OpenAI deal announced this morning after Microsoft formally dropped exclusivity

-

That last one is critical. OpenAI is now multi-cloud. Which means OpenAI is now spreading the IOU across more counterparties — which is good for OpenAI’s leverage and bad for AWS’s pricing power. The market is going to want to know whether AWS got OpenAI on hyperscaler-friendly terms or whether they paid up to break the Microsoft monopoly. If Andy Jassy can answer that question convincingly, AMZN holds the +25% April. If not, the gain becomes the giveback.

Our read: AMZN is the most likely of the four to print fine, react fine but underwhelm vs. the run-up. Buy-the-rumor / sell-the-news risk is highest here.

Part 3: The AGI-Family Observation Other Analysts Are Missing

Here’s the connective tissue.

Last night, the WSJ reported that OpenAI missed internal revenue and user-growth targets, and that OpenAI’s own CFO is reportedly at odds with Sam Altman about whether the company can support its data-center commitments (Investopedia) (CNBC) (Fortune). The kicker: ChatGPT’s share of US chatbot daily active users dropped to 38.3% from 55.4% a year ago (Apptopia data) — a 31% relative loss of share in twelve months. Gemini and Claude are the beneficiaries.

The market reaction Tuesday was instructive:

-

-

Oracle -3% (direct OpenAI exposure)

-

AMD -5.5% (chip deal)

-

Broadcom -4%

-

Intel -5% despite having no direct OpenAI deals

-

SOX -3.6%, worst day in a month

-

That last one is the AGI-family tell. A semiconductor index sold off 3.6% on a story about a single private company missing internal targets. That’s not how a healthy industrial cycle behaves. That’s how a thesis-trade behaves when the thesis develops cracks.

Bloomberg’s Dave Lee published the column we’d all been waiting for someone to write this morning, and the headline is “An OpenAI Bubble Is Not an AI Bubble“. Lee’s argument is exactly the position we have been articulating for two weeks and we’re going to flag this very loudly because we want it on the record:

Lee’s thesis: OpenAI’s execution issues should not be allowed to speak for the AI industry. The circular financing has made people treat them as the same thing, but they aren’t. “Consumers are not turning their backs on generative AI; they just have more choice.”

Our position has always been the same one: we are not anti-AI. We are anti-OpenAI-as-the-center-of-the-market-universe, filling that center with unfulfillable promises that drive unrealistic valuations and misallocations of capital across the entire ecosystem. The picks and shovels (semis, power, real estate, networking, Intel, TXN) are real. The hyperscaler customer revenue is real. The application-layer concept stocks built on circular IOUs from one private company are not!

That distinction is going to matter tonight, because if MSFT/GOOGL/AMZN all print solid cloud growth from enterprise customers other than OpenAI, the “AI is real” thesis stays intact even while the “OpenAI is everything” thesis cracks. That’s the most likely outcome. It’s also the one the cable guys are going to mis-frame for two days before the smart money figures it out.

Part 4: The China Decoupling Gets Real

Part 4: The China Decoupling Gets Real

The other AGI-family connection nobody’s drawing: the same week WSJ leaks OpenAI’s internal numbers, Beijing kills the Meta-Manus deal in a 54-character decree (Bloomberg). Manus founders under exit bans. Singapore-incorporated didn’t matter. Three Chinese investment houses are now reportedly dismantling their offshore “red-chip” structures to even qualify for Hong Kong listings.

Read the Bloomberg piece in full (China’s Meta Backlash Renders Manus Model ‘Officially Dead’). The quote that matters from ZenGen’s Dermot McGrath: “As of today, ‘the Manus Model’ is officially dead.”

The structural read: for fifteen years, the global AI talent and capital flow ran roughly: Chinese engineers + US capital → Singapore/Cayman wrapper → US listing/M&A. Beijing just made that pipeline illegal in practice. Going forward, you have two AI ecosystems that do not pass capital, code, or people between each other.

This matters because:

-

-

Meta’s agentic strategy just lost its lead horse — and it cannot be unwound; the engineers are already inside Meta AI

-

DeepSeek now raises domestically (talks at $20B valuation per Bloomberg) — meaning Chinese AI compute will not run on Nvidia

-

The $660B hyperscaler capex thesis is now structurally a US-only story — which makes the “AI revenue per dollar of capex” math worse for the West, not better

-

Apple, which ships into China, has a new geopolitical overhang — and reports tomorrow night

-

If you’re building the cap table for AI through 2030, you now have two cap tables. That’s not a market you can index. That’s a market you have to stock-pick.

Part 5: Powell’s Last Press Conference?

Now to the part of this post Phil specifically wanted on the record, because this is the kind of structural change that happens once in a generation and the market is not pricing it.

Today at 2:30 PM, Jerome Powell will likely hold his last formal press conference as Federal Reserve Chair (MarketWatch) (Morningstar). His term as Chair expires May 15. Kevin Warsh — assuming he’s confirmed — has signaled he may discontinue post-meeting press conferences entirely, which raises the question: once these are gone, do they ever come back?

Let’s get the history right because most market commentary is butchering it:

Two of the four longest-serving Fed chairs in modern history gave zero press conferences. Volcker tamed the worst inflation in living memory without one. Greenspan ran nineteen years on the most powerful monetary chair on earth without taking a single live question on camera. Powell has held roughly 56 of them.

Phil’s observation is sharp here: Powell’s press conferences have been reliable market boosters. That is not an anecdote — it’s a documented fact. Academic studies of the post-FOMC two-day window show the lion’s share of equity returns since 2019 have come on the press-conference half of the cycle, not the rate-decision half. The “Powell Press Conference Lift” is a structural feature of this cycle.

If Warsh ends the practice — or even reverts to the Bernanke/Yellen 4-per-year cadence — a known reliable equity-positive event disappears. The market doesn’t get to substitute it with anything. Volatility around FOMC days up. Information content down. Bond market guesswork up. Forward guidance less credible. The combination of less communication with more political pressure on the Fed is a dangerous thing.

Greg Mankiw’s 2024 critique was that Powell’s pressers had become “the least possible information in the most words possible” — and he had a point. But the information content floor was higher than zero. Going to zero pressers takes us from “low signal, low noise” to “no signal, all noise.” The Volcker era’s zero-presser approach worked because Volcker gave the market a single iron rule (kill inflation at any cost) and stuck to it. Warsh in a Trump-deference posture with no press conferences is not the Volcker analog. It’s something genuinely new and genuinely worse for price discovery.

Our practical takeaway: if today is indeed Powell’s last presser, the market loses a coordinator function it has implicitly relied on for seven years. Vol mispricing in coming months will be a feature, not a bug. Buying VIX into FOMC weeks (not just the day-of) will work better in 2026 H2 than it did in H1.

Part 6: The Stuff That Got Buried Today

Three more pieces nobody’s talking about because of the Mag 4 / FOMC noise:

1) Deutsche Bank’s CRE problem just resurfaced. DB reported this morning. CET1 ratio missed at 13.8% vs. 14% expected. Loan provisions of €519 million driven by a single-name commercial real estate exposure. CRE portfolio €23.9 billion total, with €3.8B in stage-3 (highest-risk) bucket — up from €3.6B last quarter (Bloomberg) (DB Q1 presentation). Stock down 19% YTD — worst European bank performer. And the ECB’s first-quarter Bank Lending Survey out Tuesday shows euro-zone banks tightened corporate credit standards by the most in more than two years — the biggest tightening since Q3 2023, attributed in part to the Iran war. This is the credit-cycle canary we’ve been watching for.

2) Clive Crook’s debt piece in Bloomberg this morning is the kind of thing nobody wants to read but everybody should (America’s Broken Politics Are Dragging It Down a Fiscal Black Hole). The math from the Brookings/Riedl chartbook (Brookings):

-

-

Federal deficits running 6% of GDP structurally — 7%+ if cuts/spending get extended

-

Public debt about to surpass the WW2 peak of 106% of GDP in the next few years

-

By 2036: debt-to-GDP 30 percentage points above WW2 peak

-

Within 10 years: debt service = 30% of all federal taxes collected

-

Within 30 years: debt service = 50%+

-

To stabilize at 100% of GDP: $2 trillion/year of adjustments by mid-2030s

-

A 10-percentage-point across-the-board income tax hike — politically unimaginable — gets you only 3.5% of GDP. A European-style 20% VAT — also unimaginable — gets you 3%. Neither alone is enough, and both at once is “you cannot get there from here.” Crook’s conclusion is bracing: “barring an AI miracle or a rebirth of functional politics, the likeliest outcome is therefore default — gradual, with higher inflation eroding the real value of federal debt, or sudden, with outright debt restructurings.”

This is why long-end Treasuries can’t be the safe-haven they used to be. And it’s why we’re staying in TLT puts and out of long-duration bonds even when stocks wobble.

3) Tomorrow’s stagflation print. GDP advance Q1 + March PCE drop together at 8:30 AM Thursday. Atlanta Fed GDPNow has Q1 at +1.2% SAAR (KrokFin). March CPI already came in at 3.3% YoY, so PCE is likely 2.8-3.0%. That’s the textbook stagflation print — slow growth + sticky inflation arriving on the same morning. The Fed will have just held rates (today’s decision is a near-100% lock to stay at 3.50-3.75% per JPMorgan and Polymarket <1% odds of a cut) — and the data will immediately tell them why they were right to be stuck.

Part 7: How We’re Playing Today

Posture is unchanged but tightened:

-

-

Long the picks-and-shovels with real balance sheets: INTC (post-Q1 print), TXN, AMAT/LRCX/KLA, VST/CEG/NRG. Add nothing today — wait for the dust to settle on AI capex guides tonight.

-

Real-economy longs intact: UPS (Top Trade), SYF (Top Trade), Delta.

-

Cautious-to-short the application layer: NVDA, PLTR, ORCL, pure-play AI ETFs.

-

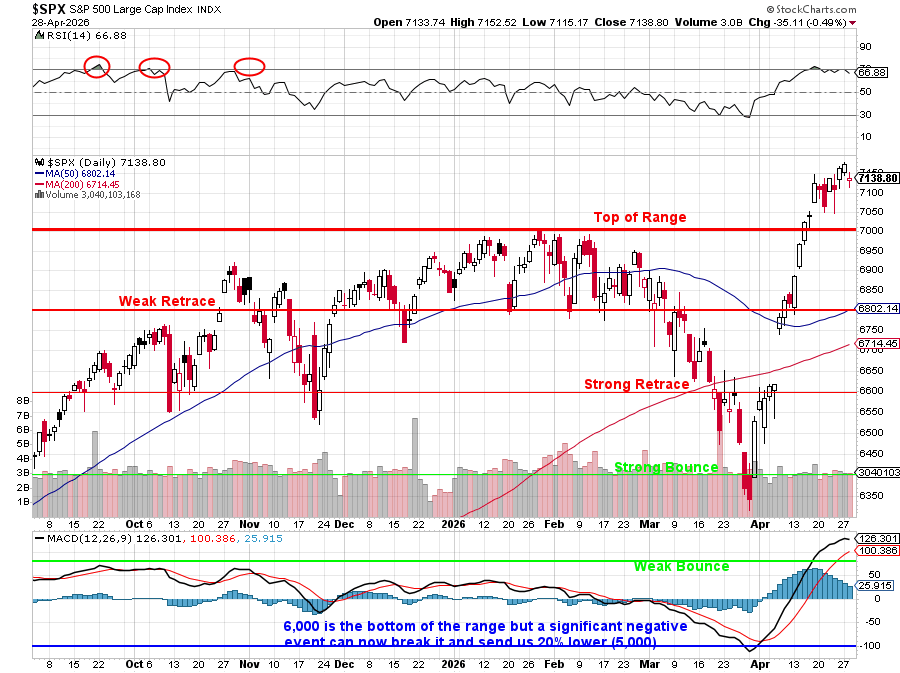

Index hedges stay on: VIX May calls, SPX 7,100/7,200 bear call spreads, SPY puts.

-

Dry powder still waits at 6,800 and 6,600.

-

NEW: TLT puts stay on. The fiscal piece reinforces this trade.

-

NEW: cash is fine. Nothing wrong with sitting out Wednesday afternoon and starting Thursday with information instead of opinions.

-

Part 8: Live Trading Webinar — 1 PM ET

We will of course be in our PSW Live Trading Webinar at 1:00 PM ET for live coverage of the 2:00 PM Fed release and 2:30 PM Powell press conference — possibly the last one ever. Members can join via the usual channel. This is the kind of session you don’t want to miss — a known structural change to the most important communication channel in the most important market in the world is happening today, and you should hear it live.

The Bottom Line

We are at the top of a hill. Oil is at $1034, Brent flirted with $115 this morning, the UAE just walked out of OPEC, China just killed Meta’s $2B agentic-AI plan, OpenAI’s CFO is reportedly fighting with the CEO over whether they can pay their data-center bills, Deutsche Bank just took a CRE writedown, the euro-zone banking system just tightened credit by the most in two years, the U.S. fiscal trajectory points toward inflation-default by 2040, the Fed is about to hold a rate it cannot lower because of oil and cannot raise because of growth, and in 80 seconds tonight four companies worth roughly $14 trillion will tell us whether the spending boom that built every data center we wrote about Friday is sustainable.

Either we’re at the top of the hill and the rails are about to do their job — clack, clack, clack, clack — or we’re at the top of the hill and the bolts are missing and we discover that fact at maximum kinetic energy.

Either way: we’re hedged, we own real businesses, we keep dry powder, and we’re going to listen to Powell at 2:30 like it’s the last one.

Because it might be…

{kind=link}