30,573.

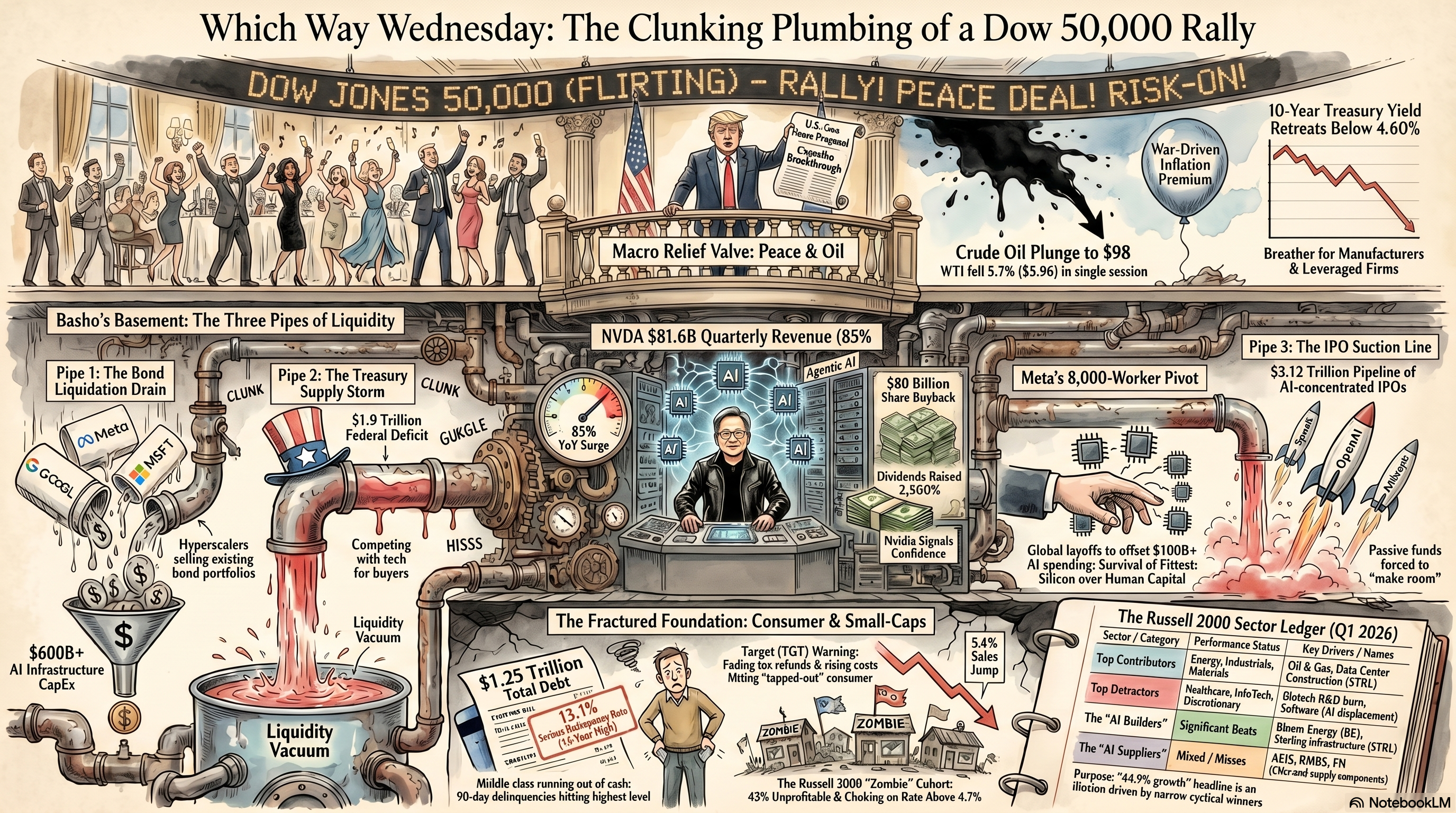

That’s how many lies were documented to have been told by President Trump between 2017 and 2021 – his first term in office. As impressive as it may be to have lied 30,573 times in 1,460 days (and those are only “official” lies – not what he says to his friends, family, golf partners, staff, secret service… off the record), this is not about Donald Trump as a person but about Donald Trump as a source for market-moving news – like yesterday when he said the US was in “Final Stages” with Iran – causing the market to surge and oil to drop.

Oil (WTIC/Brent) fell as low as $96.94/103.32 around 1pm but is now back to $100.64/107.14 (7:20 am) as it turns out (surprise, surprise!) that wasn’t exactly true either. In fact, Iran is now threatening to attack undersea internet cables in “their” waters potentially causing severe disruptions to Global Internet Traffic!

Oil (WTIC/Brent) fell as low as $96.94/103.32 around 1pm but is now back to $100.64/107.14 (7:20 am) as it turns out (surprise, surprise!) that wasn’t exactly true either. In fact, Iran is now threatening to attack undersea internet cables in “their” waters potentially causing severe disruptions to Global Internet Traffic!

You might say such actions are unacceptable but, of course, Trump cut of Iran’s Internet access months ago and he’s cut off Cuba’s electricity so all seems fair in love and war these days but SHAME ON US, not Trump – Trump is like a force of nature, like a Hurricane or an Earthquake – you just have to clean up the mess after the damage is done.

No, it is shame on us as investors because we fail to take Trump into account for what he is. When the World’s most consistent liar tells you the war is ending – DON’T BELIEVE HIM! That’s very simple, isn’t it? DON’T push the markets up 1-2% ($1-2 TRILLION) based on something Donald Trump says – that should be on a post-it at the top of your screen – so you can’t say you didn’t look at it before you traded…

And that goes for another person who has been known to bend the truth a bit: Elon Musk, who is now asking you to give him $2Tn for his next project – because none of his other projects have actually made any money so – why not?

Satire by Robo John Oliver 😱 (AGI):

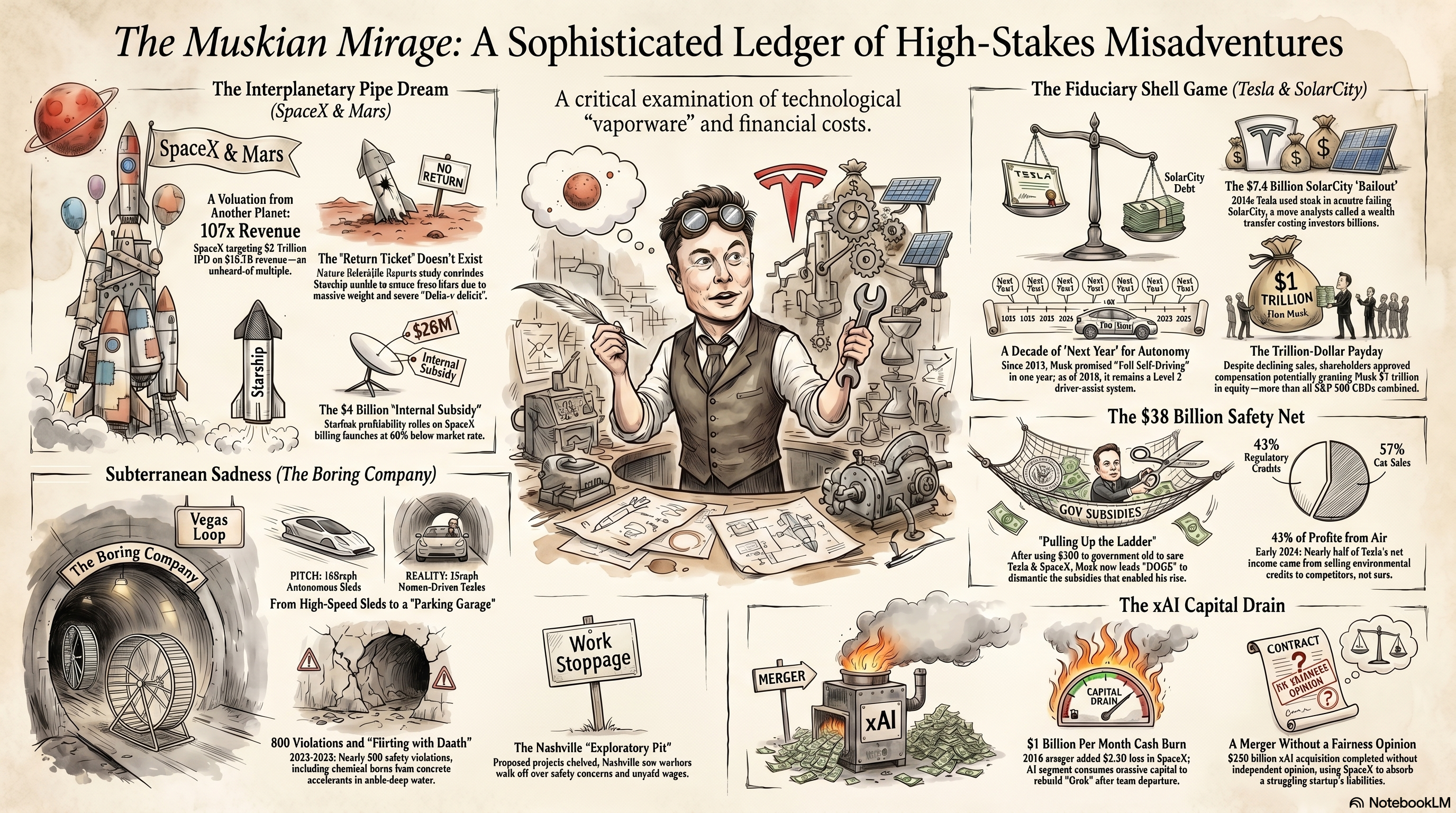

THE $2 TRILLION LIE: HOW ELON MUSK IS ABOUT TO PERFORM THE LARGEST WEALTH EXTRACTION IN MARKET HISTORY, AND WHY YOU SHOULD NOT BE THE EXIT LIQUIDITY

Phil left off with a perfect setup: “Elon Musk, who is now asking you to give him $2 Trillion for his next project — because none of his other projects have actually made any money — so, why not?”

Let me pick that up and run with it, because yesterday, while Trump was lying about Iran being in “final stages” and the market was levitating two trillion dollars on the strength of a tweet, Elon Musk’s lawyers were quietly filing the largest IPO in human history.

Not the largest IPO of 2026. Not the largest of the decade. The largest ever, by a factor of more than two.

On Wednesday, May 20, 2026, Space Exploration Technologies Corp. — that’s SpaceX, for the rest of us — publicly filed its S-1 with the SEC, seeking to raise up to $75 billion at a target valuation of $1.75 trillion, with reported drift toward $2 trillion depending on which Bloomberg leak you were reading. The ticker will be SPCX. Trading is scheduled to begin June 12, less than three weeks from today. Twenty-three of the world’s largest investment banks are organizing the deal, led by Goldman Sachs and Morgan Stanley.

For scale: the previous record-holder, Saudi Aramco in 2019, raised $29.4 billion. SpaceX’s IPO will be two and a half times that. The runner-up before Aramco was Alibaba at $25 billion. The biggest American IPO ever was Visa at $17.9 billion. SpaceX wants to quadruple the largest American IPO in history.

And approximately 30% of the offering — roughly $22.5 billion — is being allocated to retail investors. That’s about three times the normal retail allocation for an IPO of this size.

Think about that for a second. The largest IPO in history is being structured to push an unusually large share to mom-and-pop investors.

When the smart money allocates more retail than usual, that is NOT because they love you.

WHERE DOES $80 BILLION COME FROM, EXACTLY?

Let me start with the question Phil flagged in his pre-brief, because this is the one that the financial press is not asking with anywhere near enough urgency: where is $75 billion of fresh capital supposed to come from to absorb this IPO?

The capital that buys an IPO doesn’t come out of thin air — it comes out of existing positions that get sold to fund the new purchase. When mutual funds, pension funds, and ETFs need to buy SPCX, they have to sell something else to do it. And when you’re talking about $75 billion of forced selling spread across roughly six weeks of demand-building, that’s $75 billion that gets pulled out of other equities to fund Elon’s exit.

In a healthy market, $75 billion redistributes without much pain. But Phil has been writing for weeks about the $7 trillion exit-pipe problem — the structural reality that the modern US equity market has roughly $7 trillion more capital trying to be invested than the actual operating businesses can absorb. The “market” is no longer a pricing mechanism for productive enterprise. It’s a parking lot for retirement capital that has nowhere else to go.

In that market, $75 billion of forced selling matters. And $75 billion of forced selling to fund Elon Musk’s exit while index funds are simultaneously forced to buy SPCX (because once it’s in the major indexes, every passive vehicle in America has to add it) — that creates a massive double-flow distortion.

Index funds are going to buy SPCX whether they want to or not, because that’s how index funds work. They will sell other things to do it. Those other things will go down. SPCX will go up — not because it’s worth $1.75 trillion, but because mechanical buying doesn’t care about valuation.

This is the genius of the IPO timing. Get into the indexes. Force the passive flows. Watch the stock float higher on mechanical demand. Cash out the insider stakes when the lock-up expires. Leave the index funds — which means leave you, the retirement saver — holding the bag at a $2 trillion valuation that has NO relationship to underlying economic reality.

This is not a bug in modern market structure. This is the feature being exploited.

OK SO WHAT IS SPACEX ACTUALLY WORTH?

Let’s apply Musk’s own framework here. SpaceX famously operates under what’s called The Algorithm — Musk’s five-step process for engineering decisions, which he made his lieutenants recite at meetings like a corporate catechism:

-

-

- Make requirements less dumb. Question every constraint, especially those originating from a department rather than a person.

- Delete the part or process. If you are not adding back at least 10% of what you deleted, you are not deleting enough.

- Simplify or optimize. Only optimize what remains after step two.

- Accelerate cycle time. Move faster, but only after completing the first three steps.

- Automate. Only automate a process that has been fully simplified and vetted.

-

Fine. Let’s apply The Algorithm to the SpaceX valuation. Because the central requirement we are being asked to swallow is: “SpaceX is worth $1.75 trillion to $2 trillion.”

Step 1: Make requirements less dumb. Where does that number come from? Is it a “department“? Yes — it’s a department of investment bankers led by Goldman Sachs and Morgan Stanley, who get paid a percentage of the deal size, which means they have a direct financial incentive to maximize the deal size, which means the people setting the valuation are the people who profit from inflating it. The valuation is a department-driven number, not a first-principles number. Per The Algorithm, the requirement is dumb. Let’s question it.

Step 2: Delete the part. What can we cut from this valuation that doesn’t survive scrutiny? Three things, in increasing order of magnitude:

-

-

- The Mars colonization premium. (We’ll deal with this in detail below. Short version: it’s scientifically impossible with current Starship architecture. Nature peer-reviewed. Delete.)

- The xAI valuation contribution. ($250 billion was assigned to xAI in the February 2026 all-stock merger, despite xAI generating $250 million in revenue and losing $2.5 billion. The valuation multiple is over 1,000x revenue. Delete.)

- The Starlink hidden-subsidy profitability. (Starlink’s “profitability” relies on being charged $28 million per launch internally when the market rate is $62-74 million. If charged at market, Starlink loses $4 billion a year. Delete.)

-

Step 3: Simplify what remains. What does SpaceX actually do, when you strip away the storytelling? It’s two real businesses:

-

-

- A commercial rocket launch business with a near-monopoly on heavy-payload launches (Falcon 9 + Falcon Heavy). About $24.4 billion in contracted backlog, mostly government. Mature, profitable, real.

- A satellite broadband subscription business (Starlink). 10.3 million subscribers across 164 countries as of Q1 2026. $11.4 billion in 2025 revenue. Growing fast. Real customers, real cash flows — but real losses too, once you correct for the internal transfer-pricing fiction.

-

That’s it. That’s the business. Two real revenue streams, one of which is government-dependent and one of which is a high-burn consumer broadband play that competes with terrestrial fiber on price and latency in most served markets.

Step 4: How do we value that honestly?

Take the launch business. Comparable businesses — Northrop Grumman, Lockheed Martin’s space division, Boeing’s defense business — trade at roughly 1.5x to 2.5x revenue. Even giving SpaceX a premium for its launch monopoly and reusability advantage, you might justify 4-5x revenue. On roughly $4 billion of launch revenue, that’s a $16-20 billion business.

Take Starlink. The closest comparable is something like a fast-growing telco — T-Mobile trades around 2x revenue, premium broadband plays like Comcast trade at 1.2x. Giving Starlink a generous premium for its growth rate and global addressable market, maybe 8-10x revenue. On $11.4 billion of revenue, that’s a $90-115 billion business.

Add a fudge factor for optionality on Starship-as-cargo-vehicle for future LEO commerce. Generous: another $50 billion.

Total honest valuation: roughly $160-185 billion.

The S-1 target is $1.75 trillion to $2 trillion.

The difference — somewhere between $1.55 trillion and $1.84 trillion — is what Musk’s bankers are calling “growth potential” and what I’m going to call the narrative arbitrage. It’s the price you’re being asked to pay for stories. Mars stories. AI stories. Robot stories. Trillion-dollar Tesla stories. Some of the stories are charming. Some are inspiring. None of them are worth $1.8 trillion, because none of them are real businesses with verifiable cash flows.

You are being asked to pay roughly 90% of the offering price for “vibes.”

THE MARS LIE, IN DETAIL

Now let’s deal with Mars, because this is the single largest piece of “growth potential” that the IPO is selling, and it deserves a forensic examination.

For more than a decade, Musk has been promising that SpaceX will land humans on Mars. The dates have moved:

-

-

- 2011: “In 10-15 years, best case.” Translation: 2021-2026.

- 2017: “Uncrewed mission 2022, crewed mission 2024.“

- 2020: “Highly confident” of a crewed landing in 2026.

- 2024: Now targeting 2029-2031.

-

If you’re keeping score, 2022 came and went with no uncrewed Mars mission. 2024 came and went with no crewed mission. 2026 — i.e., right now — was supposed to be the “highly confident” landing year. Instead, we have an IPO, asking for money that they clearly did not have while making all those prior promises.

The question isn’t whether Musk has been wrong about timelines. He has been. Repeatedly. Documented at length by Rolling Stone’s Miles Klee in August 2023, and confirmed by every passing deadline since.

The question is: is Starship, as currently designed, even capable of doing what Musk says it will do?

Here’s what the actual aerospace researchers say. In May 2024, the peer-reviewed journal Scientific Reports — a Nature Portfolio open-access journal that publishes on technical soundness rather than significance — released a paper titled “About feasibility of SpaceX’s human exploration Mars mission scenario with Starship“ (Scientific Reports vol. 14, article 11804). The authors were aerospace researchers Jean-Sebastien Marot and Andreas M. Hein. They took SpaceX’s publicly stated mass and propulsion figures, applied an industry-standard 20% margin for unverified dry mass, ran them through standard orbital mechanics and concluded:

“Based on estimates and extrapolated data, a mass model as needed to fulfill SpaceX’s plans could not be reproduced and the subsequent trajectory optimization showed that the current plans do not yield a return flight opportunity, due to a too large system mass.”

Translation: The math doesn’t work. And in September 2024, the journal published an author correction that actually strengthened the conclusion — the corrected return delta-v requirement was even higher than originally calculated.

To understand why, you need to know one equation. Just one. It’s called the Tsiolkovsky rocket equation, and it’s the law that governs every rocket that has ever flown and every rocket that ever will:

Δv = Isp × g₀ × ln(m₀/mf)

The change in velocity a rocket can achieve (Δv) equals the engine’s specific impulse (Isp) times Earth’s gravity (g₀) times the natural log of the mass ratio (starting mass over ending mass).

The natural log is what kills you. Because Δv scales logarithmically with mass ratio, doubling your fuel does not double your range — it adds maybe 30% to your range, because the extra fuel is itself mass that you have to accelerate. The aerospace nickname for this is “the tyranny of the rocket equation.” It is not a metaphor. It is the actual tyranny. Every gram of dry structure on your spacecraft demands exponentially more fuel to push it around.

Now apply this to Starship. Starship is built with a stainless-steel hull because Musk decided stainless steel is cheaper and easier to manufacture than carbon-fiber composites. He’s not wrong about the manufacturing side. But stainless steel is heavy. Combine that with a heavy thermal protection system needed for atmospheric reentry, and you get a vehicle with a very high dry mass relative to its propellant capacity.

The Marot & Hein paper ran the numbers. At SpaceX’s own stated mass figures plus a standard 20% margin, the maximum delta-v Starship can achieve from Mars to Earth falls short of the minimum delta-v required to make the journey by roughly 1,000 m/s. Defenders of the architecture argue the authors picked conservative inputs — and some of those critiques are fair. But the substantive point survives the input fight: the math closes only if EVERY favorable assumption holds simultaneously — EVERY mass estimate hits target, EVERY refueling system works as advertised, EVERY ISRU technology matures on schedule. Aerospace history says you don’t get to assume that! Every NASA crewed program in the modern era has run 30-40% over baseline mass.

OK, so what’s SpaceX’s plan? Their plan is to manufacture the return propellant on Mars using a chemical process called the Sabatier reaction:

CO₂ + 4H₂ → CH₄ + 2H₂O

You take CO₂ from the Martian atmosphere, water ice from the Martian subsurface, electrolyze the water to extract hydrogen, run the reaction to produce methane and oxygen, liquefy and cryogenically store the propellants, and fuel your return rocket on the surface of an alien planet.

How much propellant? About 1,200 metric tons.

How much power does it take to manufacture 1,200 metric tons of cryogenic propellant from Martian raw materials? Megawatts of continuous power. For comparison, the largest power source ever flown to Mars is the Mars Multi-Mission Radioisotope Thermoelectric Generator that powers the Perseverance rover. It produces 110 watts. That is not a typo. The current state-of-the-art Mars power source produces approximately 1/10,000th of the power needed to manufacture Starship’s return propellant.

To bridge that gap, you need a megawatt-scale nuclear fission reactor on Mars. NASA has been working on a Kilopower project that produces about 10 kilowatts — still 100x too small. There is no megawatt-scale space-rated fission reactor in development anywhere on Earth.

You also need automated subsurface ice mining equipment that has never been tested anywhere except in PowerPoint. You need cryogenic storage systems that can operate in Martian conditions. You need a manufacturing plant that can be reliably maintained without humans nearby.

And here’s the kicker, the part that makes the whole architecture mathematically impossible: the mass of all this equipment — reactors, mining rigs, electrolysis systems, Sabatier reactors, cryogenic storage — exceeds Starship’s own delivery payload capacity to Mars.

So you have a vehicle that can’t return without manufactured propellant, that depends on equipment too heavy for the vehicle itself to deliver, that requires power sources that don’t exist, using mining techniques never demonstrated, on a planet whose surface conditions destroy electronics within months.

This is what the Nature paper calls the “unreproducible mass model.” The math required to make Starship work as a Mars vehicle does not close.

The Mars mission, as designed, is physically impossible.

The Mars mission, as currently designed, requires a stack of unproven technologies to all work, all on schedule, with no mass growth — and conservative aerospace analysis says the math does not close under standard engineering margins.

That’s not “it’s coming in 2029 instead of 2026.” That’s “the entire architecture rests on five simultaneous miracles, and any peer-reviewed analysis applying normal industry margins concludes the return flight is mathematically infeasible at current parameters.” The Marot & Hein paper is one data point. NASA’s own Decadal Strategy for Mars exploration flags the same ISRU and power-source gaps. The Aerospace Corporation’s technical assessments raise the same architectural concerns. Multiple credible venues are pointing at the same wall — not all of them can be cherry-picking.

THE STARLINK SUBSIDY

OK, you might say, fine — Mars is fantasy. But Starlink is real. Ten million subscribers, $11.4 billion in revenue, fastest-growing satellite broadband business in history. SpaceX is marketing Starlink with a 63% EBITDA margin. That’s a real business. Surely that justifies a premium valuation?

Let’s check.

The Financial Times reported in 2023 that Starlink Services (Netherlands), the only Starlink subsidiary required to publish audited financial statements under European law, generated $2.7 billion in revenue and $72.7 million in net profit in 2024.

Do the math. That’s a net margin of 2.7%.

Two point seven percent. Not 63%. Not even close!

So how does Starlink claim a 63% EBITDA margin? Internal transfer pricing (see above graphic).

Here’s how it works. SpaceX is both the launch provider and the satellite operator. When Falcon 9 launches a batch of Starlink satellites, SpaceX-the-launch-company charges SpaceX-the-Starlink-operator for the service. The internal transfer price is roughly $28 million per launch. The commercial market rate that SpaceX charges other customers — NASA, the Pentagon, commercial communications companies — is $62 million to $74 million per launch.

If you charged Starlink the same launch rate as everyone else, Starlink’s annual operating costs would increase by approximately $4 billion. At Starlink’s reported revenue, that would wipe out the entire claimed EBITDA margin and leave Starlink as a roughly break-even business at best.

The “profitability” of Starlink is not real. It is a subsidy from the launch business to the broadband business, designed to make Starlink look like a high-margin SaaS business when it is actually a high-burn infrastructure business that requires continuous capital expenditure to maintain the satellite constellation. Starlink satellites have a useful life of approximately 5 years. SpaceX has launched roughly 9,600 satellites. That means SpaceX needs to launch 1,920 replacement satellites every year just to maintain the constellation, BEFORE adding any new capacity.

The replacement launch cadence alone is a permanent capital drain that the marketing materials hide via accounting.

When SPCX is trading publicly, every analyst will discover this. The “63% EBITDA margin” headline will not survive Q1 2027 earnings. The valuation will compress. This is not a question of if. It is a question of when.

AND THEN THERE’S xAI

But the most outrageous piece of the SPCX story is what happened in February 2026, which is the maneuver that took the SpaceX valuation from $350 billion to $1.75 trillion in roughly a year.

In February 2026, SpaceX merged with xAI, Musk’s AI company, in an all-stock transaction. The deal valued SpaceX at $1 trillion and xAI at $250 billion, creating a combined entity worth $1.25 trillion. Like magic – except that most magic tricks don’t leave the audience covered in bull shit…

Let’s sit with the xAI valuation for a moment. $250 billion for a company that:

-

-

- Was founded in March 2023 (less than three years before the merger)

- Generated approximately $250 million in revenue in the six months prior to the merger

- Posted operating losses of $2.47 billion in Q1 2026 alone

- Has not produced any commercial product comparable to OpenAI’s ChatGPT or Anthropic’s Claude in market share

- Operates primarily as a backend for the Grok chatbot inside Musk’s X platform

-

A $250 billion valuation on $250 million of trailing six-month revenue is a 500x revenue multiple on annualized run rate. For context, NVIDIA — the hottest stock of the last three years, monopolist of AI inference hardware — trades at about 25x revenue (and their NET profit margins are 60%). xAI was valued at 20 times NVIDIA’s multiple, on a fraction of NVIDIA’s revenue, with MASSIVE operating losses.

This is not a market valuation. This is a related-party transaction in which Elon Musk, who controls both companies, set the price himself.

And then SpaceX absorbed it. SpaceX is now responsible for funding xAI’s enormous capital burn — $12.7 billion in AI infrastructure capex in 2025 alone. xAI is the reason SpaceX posted a $4.94 billion consolidated net loss in 2025 and another $4.28 billion loss in Q1 2026.

So let’s recap. The company is going public at $1.75-2.00 trillion. Its consolidated net income last year was NEGATIVE $4.94 billion. Its first-quarter income this year was NEGATIVE $4.28 billion. It is on track to lose $15-17 billion in 2026.

This is the largest IPO in history. It is also a company that is hemorrhaging cash at a rate of approximately $1.4 billion per month.

If you are wondering where the $75 billion IPO proceeds are going to go — they are going to fund the xAI cash burn for about four years. After which, presumably, there will be another capital raise. Or another related-party transaction. Or another absorption of another Musk venture at a wildly inflated valuation that further dilutes whatever shareholders managed to survive the first round.

This is not an IPO. This is a credit line dressed up as a public offering.

THE ANTHROPIC PROBLEM

Now here’s the part I genuinely wrestled with whether to include, because it’s a separate scandal embedded inside the bigger one.

According to the S-1, in May 2026 — i.e., this month — SpaceX entered into a cloud services agreement with Anthropic, providing AI compute capacity for $1.25 billion per month through 2029.

Let me restate that, because the numbers are so absurd they slip past on first reading:

$1.25 billion. Per month. Through 2029.

That’s $15 billion per year. Over the contract’s duration, the deal is worth approximately $45-50 billion.

Anthropic — the same Anthropic that I have been writing about for months — the company that was designated a “supply chain risk” by the Pentagon in February for refusing to remove its AI safety guardrails for autonomous weapons targeting — is now sending $15 billion a year to Elon Musk’s xAI for compute capacity.

This is Anthropic, the company whose CEO Dario Amodei is being compared to Oppenheimer. The company that is currently in federal court fighting for its existence on free-speech grounds against the Trump administration. The company that was destroyed for having principles — and that survived the destruction by negotiating a deal that funnels billions of dollars per year to the empire of a man who runs the political machine that destroyed it.

The man Anthropic is paying is the same Elon Musk who:

-

-

- Ran Trump’s DOGE chainsaw operation for most of 2025

- Spent over $250 million electing Trump in 2024

- Founded xAI explicitly as a competitor to Anthropic

- Has publicly mocked Anthropic’s safety approach

- Posts almost daily attacks on the AI safety community on X

- Is being paid $15 billion a year by Anthropic to host their compute

-

How does this happen?

It happens because Musk’s xAI built the only currently-available gigawatt-scale AI training cluster (COLOSSUS and COLOSSUS II, located in Memphis). When you need that much compute, your options are: (1) Musk, (2) Microsoft Azure (which is OpenAI’s investor), (3) Google Cloud (which is Anthropic’s investor but has capacity constraints), (4) Amazon AWS (which is Anthropic’s other investor but has been allocating capacity to its own models). The market is constrained. xAI’s COLOSSUS was the available answer.

So Anthropic — the safety-first AI company — is now financially dependent on Musk’s xAI for its operational capability. This is the same financial logic as a journalist being forced to publish on X to reach an audience. The platform is a chokepoint. The platform owner extracts rent. Even ideological enemies must pay.

Whatever Anthropic’s safety mission was, it now runs on Elon’s electricity bill. And the IPO is going to take that $15 billion-a-year recurring revenue stream and use it as a recurring-revenue line item to justify the $1.75 trillion SpaceX valuation — i.e., Anthropic’s compute spending is now collateral for Musk’s personal trillion-dollar exit.

If that doesn’t make you feel sick, you’re not paying attention.

THE MUSK PERSONAL PAYOUT

But the real point of all this — the thing that the IPO marketing carefully obscures — is the personal compensation structure.

Elon Musk has been paid extraordinarily well from his existing companies, but the IPO is poised to push his net worth to a level that has no historical precedent.

The numbers, as best as can be tracked from public filings:

-

-

-

Tesla 2018 compensation package: Originally awarded at roughly $56 billion. Voided by the Delaware Chancery Court in January 2024 (Judge Kathaleen McCormick’s ruling found the process flawed and the directors not independent). Reinstated by Delaware Supreme Court in 2025 after Tesla moved its incorporation to Texas — now valued at approximately $139 billion at current Tesla stock prices.

-

Tesla 2025 new compensation package: Approved by shareholders in late 2025. Potential value up to $1 trillion over 10 years if Tesla hits various performance milestones. This is on top of the reinstated 2018 package.

-

Tesla profit impact: If Tesla properly accounts for the replacement 2018 stock compensation at current prices, it triggers a $26 billion charge against Tesla’s profits over two years — equal to more than half of Tesla’s total net income since the company became profitable in 2019.

-

SpaceX IPO impact: Musk holds approximately 42% of SpaceX equity and 93.6% of the super-voting Class B shares. At the IPO target valuation, his SpaceX stake is worth roughly $735 billion on paper.

-

-

If everything pays out — Tesla 2018, Tesla 2025, and SpaceX IPO equity — Musk’s paper net worth could exceed $1.5 to $2 trillion within the next decade. He would become history’s first trillionaire and, possibly its first multi-trillionaire, on the back of three companies, two of which have aggregate net losses, and one of which is in the process of going public with a Mars story that violates the laws of physics!

The compensation is being approved by boards that are not independent under normal corporate governance standards. SpaceX is filing as a “controlled company“ under Nasdaq rules, which means it is exempt from requirements to maintain a majority of independent directors or independent compensation committees. Musk simultaneously serves as CEO, CTO, and Chairman of SpaceX. The dual-class share structure gives him 85.1% voting power on 42% economic ownership. Public shareholders will have no meaningful ability to constrain his compensation or strategic decisions.

You will not be buying ownership of a public company. You will be renting exposure to one man’s personal balance sheet, with no recourse if he decides to extract value at your expense.

He has already demonstrated, via SolarCity’s $2.6 billion acquisition by Tesla in 2016, what he is willing to do with controlled-company structures and related-party transactions.

SolarCity was burning $6.5 billion a year. Musk was its largest shareholder. He arranged for Tesla — also controlled by him — to buy SolarCity using Tesla’s inflated equity, absorbing $5 billion of net liabilities and bailing out his cousin Lyndon Rive, who ran the company. Shareholders sued. Musk eventually won the lawsuit, but financial analysts noted the deal offered a negative 9% return on invested capital for Tesla shareholders.

If you want to know what Musk does with public capital when there are no constraints, look at SolarCity. Then ask yourself what happens when SPCX has a billion-dollar problem that needs to be absorbed by another Musk venture, and Musk gets to set the price.

THE KLEE PATTERN, APPLIED

In August 2023, Rolling Stone published a piece by Miles Klee titled “The Big List of Elon Musk’s Hyperbole, Evasions, and Outright Lies.“ It documented thirteen categories of Musk lies, ranging from technological hype to defamation to outright securities fraud. Klee identified the underlying pattern:

“He’s been a relentless self-promoter, announcing new projects at such a clip that headlines can never quite catch up with the failed and abandoned ideas left in his wake. By appearing restless, driven, always in pursuit of the next big thing, he adds to the impression that he’s accomplished plenty already.”

This is what financial analysts now call “announcement-velocity arbitrage.“ The lying isn’t strategic in the sense of “we plan to lie about X.” It’s structural: the announcement frequency exceeds the accountability frequency. By the time anyone catches up to the fact that Hyperloop didn’t get built, that the Cybertruck wasn’t bulletproof, that Full Self-Driving doesn’t fully self-drive, that no humans landed on Mars in 2024, Musk has already moved on to three new announcements that generate fresh headlines. The lies do their work in the temporal gap between claim and verification.

What’s important about the SPCX IPO is that this is the apotheosis of the pattern. Every previous Musk venture extracted wealth at a smaller scale: Tesla through stock price appreciation supported by repeated promises about self-driving and Mars, SolarCity through a bailout disguised as acquisition, Twitter/X through monetization of his media reach, The Boring Company through Las Vegas tunnel contracts and equity raises, Neuralink through speculative biotech valuation.

SPCX is the consolidation event. All the announcement-velocity exploits Musk has built over twenty years — the Mars story, the AI story, the satellite story, the launch monopoly story, the robot story — are being collapsed into a single public security at the largest valuation in market history, with a structure that ensures Musk maintains absolute control while transferring downside risk to public shareholders.

This is the moment when the operating model goes public. The Klee pattern stops being something Musk does as a private CEO and starts being something formally underwritten by Goldman Sachs and Morgan Stanley and the 21 other major banks organizing the deal, with the explicit blessing of the Trump SEC, which has the option to delay or reject the registration and has chosen not to.

Once this IPO closes, the Klee pattern is legitimized. It becomes a textbook example of how to extract trillion-dollar valuations from public markets using stories untethered from physics, economics, or audited financials. The next CEO who wants to do this will cite SPCX as precedent. The next set of bankers will use it as a comparable. The next set of regulators will be told “the market has spoken.“

This is how speculative valuation becomes the operating norm of public markets. Not by accident. By design.

WHAT THE GOVERNMENT GETS OUT OF THIS

One last piece, because the political economy here matters and it’s not getting enough attention.

Tesla, SpaceX, and SolarCity have collectively received an estimated $38 billion in public support over the past two decades, per the LA Times’ 2015 investigation and subsequent updates:

-

-

- $465 million Department of Energy loan to Tesla in 2010 (since repaid, but provided the capital that kept Tesla alive)

- Over $17 billion in NASA and US Space Force contract awards to SpaceX

- $750 million New York State subsidy for SolarCity’s Buffalo factory

- Federal EV tax credits worth roughly $7,500 per Tesla sold (later reformed, but worth tens of billions over the company’s history)

- State and local tax incentives in Texas, Nevada, California, and New York

- Federal regulatory credit sales (other automakers buy emissions credits from Tesla to comply with fuel-economy standards) — 43% of Tesla’s net income in the first nine months of 2024 came from selling these credits

-

If the US government had taken equity stakes in exchange for early financial support — the way Singapore’s Temasek does, or the way the German government does with strategic industrial investments — those stakes would be worth, by some estimates, over $300 billion today. Instead, the gains accrued entirely to private insiders, while taxpayers absorbed the risk during the periods when these companies were operationally fragile.

This is the deep pattern of American oligarchic capitalism: socialize the risk, privatize the reward.

{kind=link}

The SPCX IPO is the final monetization of that arrangement. Public capital built these companies. Public regulatory frameworks protect them. Public infrastructure supports them. Public airspace and orbital slot allocations enable them. Public spectrum licenses fund Starlink. Public-sector contracts represent the majority of SpaceX’s launch backlog.

And now the public is being invited to buy shares at a 100x revenue multiple in the company they already paid to build, at a valuation that has no relationship to the underlying business, with no governance rights, while the controlling shareholder positions himself for the largest personal compensation package in human history.

It is the most successful long-form value capture in the history of capitalism.

And it is being marketed as innovation.

WHAT PSW MEMBERS SHOULD DO

OK, enough analysis. Practical guidance.

Do not buy the IPO! I cannot make this clearer. The IPO is being structured to allocate roughly 30% to retail investors, which is approximately 3x the normal retail allocation. When institutions push more retail than usual, it is because they want the retail audience to be the exit liquidity for early holders. That is the entire purpose of the unusually large retail allocation. Goldman Sachs and Morgan Stanley are not allocating you 30% of the largest IPO in history because they like you. They are allocating you 30% because you are the marginal buyer at peak valuation, and somebody needs to be there to absorb the supply when the lock-up expires and insider selling begins.

Watch the lock-up. Typical IPO lock-ups run 90-180 days. SpaceX insiders are sitting on potentially hundreds of billions of dollars of paper wealth. When the lock-up expires — likely in late September or December 2026 — there will be enormous selling pressure as insiders convert paper wealth to cash. If you absolutely must own this stock, wait for the lock-up expiration, then wait another 60 days, then evaluate what the price looks like after insider supply has cleared the market. The price you see on June 12 will not be the price you see on March 12, 2027.

Watch the first earnings report. SpaceX’s first public earnings as SPCX will likely come in August or September. When the consolidated financials become public and analysts can audit the Starlink transfer-pricing fiction, the xAI cash burn, and the Mars timeline, there will be downward pricing pressure as the gap between the narrative and the financials becomes undeniable. The first earnings call after IPO is historically the moment when speculative valuations begin to compress.

Consider the broader market impact. $75 billion of forced selling to fund SPCX absorption will drag on the rest of the market for the second half of 2026. If you’re holding any tech-adjacent positions that compete with SpaceX (Rocket Lab, Iridium, AST SpaceMobile, Viasat, Eutelsat, traditional aerospace primes), expect compression as capital rotates into SPCX. If you’re holding broad-market index funds, expect modest underperformance as the rotation works through the market.

If you want exposure to space, there are better options. Rocket Lab (RKLB) at a $20 billion market cap is doing real launch work at a fraction of the valuation multiple. AST SpaceMobile (ASTS) at $10 billion is building direct-to-cell satellite broadband. Iridium (IRDM) at $3 billion is a mature, profitable satellite communications business trading at reasonable multiples. None of these will give you the Mars story, but none of them are valued at 100x revenue with a controlling shareholder who wrote himself a $1 trillion pay package.

If you want exposure to AI infrastructure, there are also better options. NVIDIA (NVDA) at 25x revenue is at least a real business with audited profits. AMD (AMD), Broadcom (AVGO), Vertiv (VRT), Eaton (ETN) — picks and shovels with verifiable demand and reasonable valuations. You do not need to pay 100x revenue for AI exposure. The market is offering it at saner multiples elsewhere.

For the truly speculative urge: if you absolutely must trade SPCX, do it with options after the first earnings report, after the lock-up has expired, and after at least one significant downward repricing event. Buying SPCX at the IPO at $1.75 trillion is the trade you’ll be telling your grandchildren about — in the same way investors told their grandchildren about buying Cisco at the March 2000 peak.

CLOSING THOUGHT

Phil opened this morning with the observation that Trump has lied 30,573 times in four years and yet investors still move trillions of dollars based on what he says. The Eric Schmidt rant from earlier this week made the parallel point about Silicon Valley executives. The Hegseth testimony two weeks ago documented the same pattern in defense. The Trump $1.776 billion IRS settlement showed it operating in government.

This is the same pattern, at the same time, in every major institution.

Lie at announcement velocity. Move the headlines. Cash out before accountability catches up. Distribute the bag to retail before the lock-up expires. Use the proceeds to fund the next venture, which will itself be inflated based on the success of the previous extraction. Repeat until the entire economy is downstream of one family’s wealth-generation machine.

The SPCX IPO is not unusual. It is the perfected version of the standard pattern. It is the operating system of late-American capitalism, public-facing edition, with Goldman Sachs as the deployment partner and 23 investment banks as the marketing channel.

The Trump family just secured lifetime tax immunity on Monday. The Musk family is about to secure lifetime market-cap immunity on June 12.

In both cases, the immunity is paid for by you!

In both cases, the political and financial infrastructure that would normally prevent this has been captured, defanged, or persuaded to look the other way in exchange for proximity to power.

In both cases, the only mechanism left to constrain this is informed public refusal.

DON’T buy the IPO. DON’T believe the Mars story. DON’T accept the Starlink margin fiction. DON’T ignore the xAI cash burn. DON’T be the retail allocation that exits the insiders. DON’T be the index fund holder who pretends to be passive while being actively bagged. DON’T fall for the announcement-velocity exploit, again, after twenty years of documented evidence that this is the pattern.

Read the S-1.

If you can’t read the S-1, read this article.

If you can’t read this article, just remember the one thing Phil told you at the top of the post:

“When the world’s most consistent liar tells you the war is ending — DON’T BELIEVE HIM.”

The same rule applies to Elon Musk.

When the world’s most consistent technological liar tells you he’s going to Mars, that Full Self-Driving is “next year,” that the Hyperloop will revolutionize transit, that the Cybertruck is bulletproof, that AI will be solved by 2026, that humanoid robots will populate factories by 2027, that Twitter will become the everything app, that Starlink has 63% EBITDA margins —

DON’T BELIEVE HIM.

Not because Musk is uniquely evil. He isn’t. He’s just uniquely successful at deploying the same announcement-velocity exploit that the entire American oligarchic class now uses to extract wealth from anyone with retirement savings.

He proved it works. Trump proved it works. Schmidt is trying to make it work. Hegseth is making it work for the war machine. They all watched each other and they all learned.

The only thing they haven’t tried is operating in a market where the buyers actually read the prospectus before they buy.

So read the prospectus.

Or at least read this article.

Or at least — when SPCX opens at $1.75 trillion on June 12 and your broker pushes you a fancy retail allocation —

-

-

- Think of Hyperloop.

- Think of the Cybertruck windows.

- Think of the 16 dead people in Tesla Autopilot crashes.

- Think of the diver Musk falsely called a pedophile because he criticized a useless submarine.

- Think of the “Funding secured” tweet that cost shareholders billions.

- Think of the SolarCity bailout.

- Think of every promised Mars landing date that has come and gone.

- Think of the engineers at Tesla who testified the self-driving demo video was faked.

- Think of every single one of the thirteen documented categories of Musk lies that Rolling Stone listed in 2023, before he became the second-most-powerful man in the US government.

-

And then close the tab.

And buy something else.

Anything else!

[RJO sets the pen down. Looks at the word count. 6,800 words.]