GDP: 3 Years of Massive Downward Revisions; Inventory Adjustments Run their Course; Where to From Here? Fed’s Counterproductive Policies

Courtesy of Mish

Courtesy of Mish

The BEA has finally admitted something anyone with a modicum of common sense already knew: The recession was far deeper and the "recovery" far weaker than previously reported.

Please consider BEA report Gross Domestic Product: Second Quarter 2010 (Advance Estimate) Revised Estimates: 2007 through First Quarter 2010

Real gross domestic product — the output of goods and services produced by labor and property located in the United States — increased at an annual rate of 2.4 percent in the second quarter of 2010, (that is, from the first quarter to the second quarter), according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 3.7 percent.

The real story in the report was not the continuing ratcheting down of GDP forward estimates, but rather massive backward revisions, most of them negative, dating back three full years.

Revision Lowlights

- For 2006-2009, real GDP decreased at an average annual rate of 0.2 percent; in the previously published estimates, the growth rate of real GDP was 0.0 percent. From the fourth quarter of 2006 to the first quarter of 2010, real GDP increased at an average annual rate of 0.2 percent; in the previously published estimates, real GDP had increased at an average annual rate of 0.4 percent.

- For the revision period, the change in real GDP was revised down for all 3 years: 0.2 percentage point for 2007, 0.4 percentage point for 2008, and 0.2 percentage point for 2009.

- For the revision period, national income was revised down for all 3 years: 0.4 percent for 2007, 0.6 percent for 2008, and 0.4 percent for 2009.

- For the revision period, corporate profits was revised down for all 3 years: 2.0 percent for 2007, 7.2 percent for 2008, and 3.9 percent for 2009.

- For 2007, the largest contributors to the revision to real GDP growth were a downward revision to PCE, an upward revision to imports, and a downward revision to state and local government spending;

- The percent change from fourth quarter to fourth quarter in real GDP was revised down from 2.5 percent to 2.3 percent for 2007, was revised down from a decrease of 1.9 percent to a decrease of 2.8 percent for 2008, and was revised up from an increase of 0.1 percent to an increase of 0.2 percent for 2009.

- National income was revised down for all 3 years: $51.8 billion, or 0.4 percent, for 2007; $77.4 billion, or 0.6 percent, for 2008; and $55.0 billion, or 0.4 percent, for 2009. For 2007, downward revisions to corporate profits and to supplements to wages and salaries were partly offset by an upward revision to wages and salaries.

- Personal outlays — PCE, personal interest payments, and personal current transfer payments — was revised down for all 3 years: $15.4 billion for 2007, $15.0 billion for 2008, and $79.1 billion for 2009. For all 3 years, downward revisions to PCE more than accounted for the revisions to personal outlays. The personal saving rate (personal saving as a percentage of DPI) was revised up for all 3 years: from 1.7 percent to 2.1 percent for 2007, from 2.7 percent to 4.1 percent for 2008, and from 4.2 percent to 5.9 percent for 2009.

Inventory Rebuilding Runs Its Course

There are pages of revisions, that is just a sample. One of the key findings in the report concerns inventory rebuilding. Dave Rosenberg discusses inventories and the GDP in general in Slow Motion Recovery.

The big story in the second quarter as has been the case for much of the past year was the contribution from inventories – there was a “build” of $75.7 billion and this added over a percentage point to headline GDP growth. This follows a “build” of $44 billion in the first quarter so this is no longer the case that companies are merely reducing the pace of inventory withdrawal. Businesses actually added to their stockpiles at the fastest rate in five years. And with sales lagging behind, this inventory contribution is likely to fade fast in coming quarters. Real final sales – representing the rest of GDP (excluding inventories) – came in at a paltry 1.3% annual rate last quarter and has averaged 1.2% since the economy hit rock bottom a year ago in what is clearly the weakest revival in recorded history.

Normally, real final sales are expanding at closer to a 4% annual rate in the year after a recession officially ends. Then again, we haven’t heard anything official just yet about the one that began in December 2007 – and so the fact that it is averaging at around one-third that typical pace in the face of unprecedented policy stimulus is rather telling. And frightening.

Looking at the components of GDP, it appears as though the economy is set to slow even further and a flattening in Q3 and perhaps even contraction by Q4, barring some positive exogenous shock, cannot be ruled out.

If indeed, the inventory cycle is behind us, then what we have on our hands is an underlying baseline trend in GDP of 1.2% at an annual rate. And if we are correct in our assumption that the looming withdrawal of fiscal stimulus at the federal level and the cutbacks at the state and local government level subtract 1.5% from growth in the coming year, then it begs the question: How exactly does the economy escape a renewed moderate contraction over the next four to six quarters, barring some unforeseen positive boost? In turn, how does a strong possibility of such a contraction square with consensus views of a 35% surge in corporate profits to new record highs as early as next year? The answers to these questions are as painful as they are obvious.

Consumer Metrics Institute Looks Inside the New GDP Numbers

Rick Davis at Consumer Metrics Institute (CMI) has been calling for this slowdown and these revisions in advance. Please consider Inside the New GDP Numbers

The 2.4% figure will garner all of the headlines, but the more important "real final sales of domestic product" continues to be weak, growing at a reported 1.3% annualized rate. The real cause for concern is that the reported inventory adjustments dropped from a 2.64% component in the revised 1st quarter to a 1.05% component during the 2nd quarter. If factories have begun to realize that end user demand remains anemic, the inventory adjustments could well go negative soon, pulling the reported total GDP down with it.

The BEA revised much more than the first quarter of 2010. They revised down 2009, 2008 and 2007 as well. Apparently the "Great Recession" has been worse than our government has previously reported.

The new GDP report shows that the current gap between the consumer demand that we measure and the BEA’s reported number continues to grow as factories build their inventories in anticipation of a strong recovery. If factories curb their enthusiasm during the third quarter, the BEA’s "advance" estimate for Q3 2010 might be brutal, just 4 days before the U.S. mid-term election.

The new GDP report shows that the current gap between the consumer demand that we measure and the BEA’s reported number continues to grow as factories build their inventories in anticipation of a strong recovery. If factories curb their enthusiasm during the third quarter, the BEA’s "advance" estimate for Q3 2010 might be brutal, just 4 days before the U.S. mid-term election.

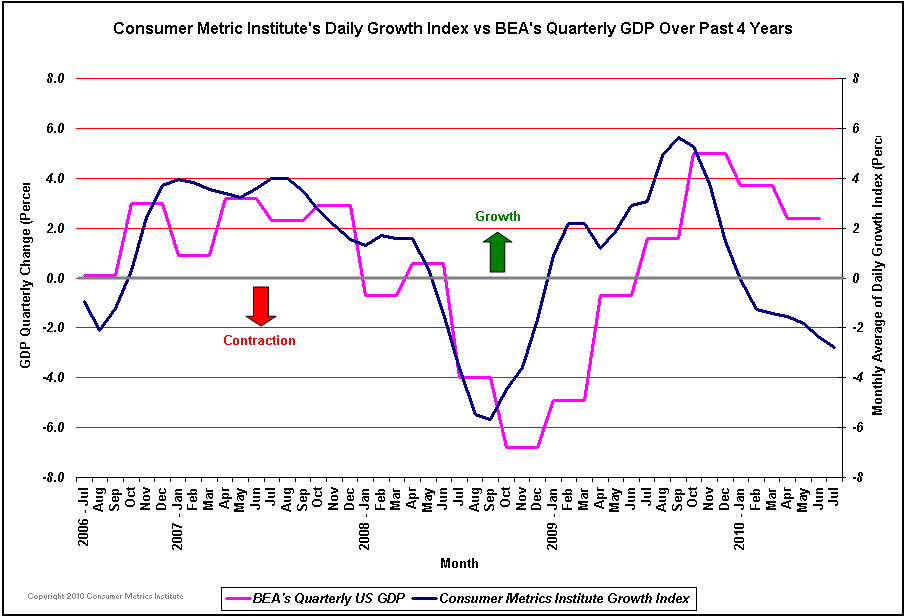

Consumer Metrics vs. BEA

click on chart to enlarge

The CMI lead the BEA by 1-2 quarters at both the prior bottom and again at the most recent peak. Although the CMI has GDP negative, that is as a result of analyzing consumer spending.

We must factor in massive government stimulus that did literally no good, but it did add to GDP.

No matter how useless, government spending is always considered productive. Thus I was certain that GDP would not come in negative this quarter. However, I am equally certain Consumer Metrics has the weakening trend correct.

Unless there is another round of huge government spending, GDP will be headed towards 0% in the 4th quarter.

For a discussion of the parameters Consumer Metrics takes into consideration and how their modeling works, please see my February 26, 2010 post GDP Contraction Coming In Second Quarter 2010?

Where To From Here?

The important point as always is not where we have been, but rather where we are headed. In this regard, note how hopeless the BEA is. We are just now getting revisions as to where we were three full years ago. Looking ahead, everyone listens to Bernanke who not only appears clueless, but has a vested interest to not tell the truth lest it "spook the markets".

However, we do not need Bernanke or the cheerleaders on CNBC to tell us what we need to know, we can open our eyes and see rising foreclosures, no "help wanted signs", a recovery in profits but no real world recovery, and various Obama stimulus measures that have all failed spectacularly, especially home tax credits.

Now that inventory replenishment is nearly over, if not indeed completely over, this economy is headed back into the toilet unless consumer demand picks up.

As noted in Bill Gross Ponders "Deep Demographic Doo-Doo" the likelihood for consumer demand to pick up is remote at best.

Hello Japan

Real final sales of domestic product — GDP less change in private inventories — increased 1.3 percent in the second quarter, compared with an increase of 1.1 percent in the first.

Those anemic numbers are AFTER trillions of dollars of stimulus money had been thrown at it.

Does this sound like Japan to you? It does to me.

Fed’s Counterproductive Policies

The Fed wants banks to lend and consumers to spend. St Louis Fed Governor James Bullard ("Bullard the Dullard"), is now proposing QE2, hoping to force down interest rates even more.

Ponder the effect on consumer spending plans. Credit card rates are north of 20%. The savings deposit rate at banks is 1%. Any consumer in his right mind has every incentive to pay down their credit cards and not spend more.

Think about that. Consumers can get effective rates of return on their money by paying off credit cards or other consumer debt and not charging more. Will forcing long-term rates lower change this picture? Of course not. Ironically, it will cause the savings rate to rise (simply by increasing the incentive to pay down debts at much higher interest rates!)

Moreover, forcing down long-term rates will rob those on fixed incomes struggling to make ends meet, thus increasing pressure on bankruptcies and foreclosures. However, it might make gold buyers happy campers as the liquidity attempts to find a home.

In other words, QE2 would be hugely counterproductive to the Fed’s desire to spur lending and spending. Those who expect to see massive inflation as a result of Bullard’s proposal, simply do not understand the role of collapsing credit in this economic depression.

Picture credit: Jr. Deputy Accountant