Courtesy of www.econmatters.com.

By EconMatters

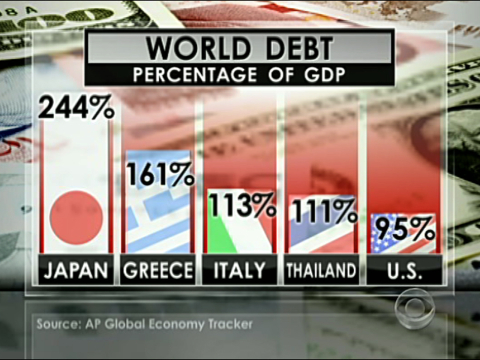

The U.S. debt ceiling political soap has finally come to an end. With the debt deal done, the U.S. has dodged a major bullet of a debt default, but may not be out of the woods yet for a sovereign credit downgrade. Nevertheless, regardless whether one or more of the Big 3 agencies (S&P, Moody’s and Fitch) would really deal a downgrade to the U.S., it is the markets that holds the key to a sovereign’s credit worthiness based on its ability to manage a balanced budget, implementing proper monetary and fiscal policies. From that perspective, the markets probably have already spoken.

A Reuters analysis discusses that typically the sovereign — the government — is seen as the most solvent entity in the country, but with a number of governments face bigger risks of downgrades or defaults, some multinational corporations are enjoying higher cash flows, and set to benefit from higher ratings than their sovereigns.

According to Reuters, in the United States, the cost of insuring the debt (i.e. CDS or credit default swap) of Automatic Data Processing (ADP), Exxon Mobile (XOM), Johnson & Johnson (JNJ) and Microsoft (MSFT) against default on a five-year horizon is at least 20 basis points lower than that of the U.S. government (See Chart) All four U.S. companies boast triple-A ratings, the same as the U.S. government, but S&P has said that a change in the U.S. sovereign credit rating or outlook will not affect these four corporations.

Moreover, a New World Order has emerged for the global sovereigns, as Reuters reports,

“Globally, 107 corporate and local governments have higher ratings than those of the sovereign in their country of domicile on a foreign currency basis, Standard & Poor’s says. That means these entities are seen as likely to be able to cover their debt obligations even when the central government of the country they are based in cannot.”

“Balance sheets of OECD countries will continue to deteriorate. You’re looking at a medium to long-term credit downgrade cycle over the next five years,” said [Ashok] Shah [chief investment officer of London & Capital.]

Indeed, with a whopping $76.2 billion in cash and marketable securities, Apple (AAPL) now has more cash than the U.S. government. Some jokingly said the U.S. government could ask Steve Jobs for a loan and that Uncle Sam should start selling iPads. These might seem like jokes for the time being, but they also might have foretold things to come in the relationship between corporations and their respective domiciles, and the changes in government entity structure where sovereign may operate more like a business.