Well, this was certainly better than last week!

Well, this was certainly better than last week!

In last weekend's wrap-up we noted the market could go either way and, after a poor start on Monday, we really pulled it together and ended up tacking on (officially) 947 Dow points (11.2%) – most of them (890) coming on Tuesday! The "good" week did not quite save us from a terrible month where the MSCI World Index fell 19.1%, Emerging Markets Fell 27%, the S&P dropped 17% and the CRB fell 22%. Even gold dropped 18.5%, the biggest monthly loss since 1983 so we need to keep this week's run in perspective until we see some real follow-through as we enter the traditional Santa Clause Rally season.

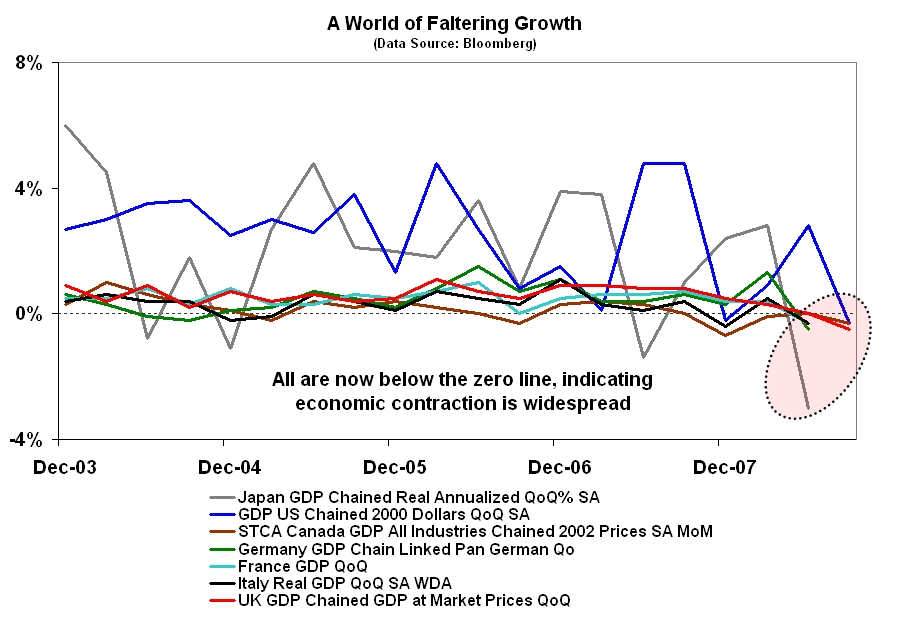

Yes the markets were oversold but the question now is – how oversold as there is very clear evidence of declining global growth which has popped the commodity bubble but also popped the Chicago PMI all the way down to 37.8 for October (down from 56.7 in September) and our GDP turned negative (-0.3%) for the first time since poppa Bush held office in 1991 so congrats to GW for getting this one in just under the wire! Sadly, we are not alone in our suffering as the global picture is falling apart along with Japan (who has led the downturn) and the US (see chart below):

Even worse than the GDP data, is the Real Per Capita Personal Income which fell an amazing 9.6% in Q3, the largest decline since 1949. This led to a decline in the PCE of 0.3%, news which the markets shook off on Friday and my concern is that the markets were poised to paint a gain on Friday and nothing was going to stop them but what will a weekend of reflection bring?

Last weekend, we didn't get any major government action to prop up the markets and the futures were limit down in the US on Monday morning. We recovered nicely from that and finished the day down "just" 200 points and we spend the rest of the week trying to get back to the highs of October 21st but still less than halfway back to where we opened the month on most indexes. I pointed out in Monday morning's post that the Nikkei was clearly oversold, trading at just 0.89 times book value and the Nikkei led us higher for the week with a 1,400-point gain (20%) off the bottom.

My sole stock selection for Monday morning was WMT and the 2010 $50s came in right at $10 in the morning and finished the week at $12.97 – that one seemed kind of obvious with the stock under $50 but I continued to bang the table on bottom fishing during member chat and I had said in the main post on Monday morning: "Already (9am) I see the futures improving. Let’s hope that follows through and we are not the only bargain hunters out there. The technical traders would love to see us make a bottom test but they were denied on Friday and they may be denied again today so it’s going to be very interesting this morning but there is nothing bullish about it until we get back over that 8,800 mark on the Dow." We took out that 8,800 line the following afternoon.

My sole stock selection for Monday morning was WMT and the 2010 $50s came in right at $10 in the morning and finished the week at $12.97 – that one seemed kind of obvious with the stock under $50 but I continued to bang the table on bottom fishing during member chat and I had said in the main post on Monday morning: "Already (9am) I see the futures improving. Let’s hope that follows through and we are not the only bargain hunters out there. The technical traders would love to see us make a bottom test but they were denied on Friday and they may be denied again today so it’s going to be very interesting this morning but there is nothing bullish about it until we get back over that 8,800 mark on the Dow." We took out that 8,800 line the following afternoon.

By Tuesday morning we were ready for a turnaround. You can read my Tuesday morning post, where I reprinted my impassioned case for buying at 8,200, which turned out to be excellent advice and, of course, almost all of the nearly 100 bullish trade ideas I put up in the past two weeks are doing very well on this bounce but we remain skeptical until we make better progress on our levels – especially the 40% off the top marks we've been watching closely for weeks.

We loved the early sell-off Tuesday morning and it gave us a great bottom test to key off of at 11 am, where we got almost all of the 1,000-point gain we were expecting off the Fed cut a day early. Our much loved UYG calls jumped over 35% from that great bottom call and the SKFs, which we loved on the way up, were just as much fun on the way down as they fell from 190 to 125 by the week's end. Even if you weren't a premium member and didn't see my FXI call at 11:04 when it was $20.35 and read about it in the evening post, it "only" opened at $22 the next morning but finished the week at $25.16. My group of slowpoke stocks on Tuesday evening did a pretty good job of outperforming the S&P for the rest of the week, especially WYNN, who jumped an additional 60% Wednesday-Friday! LVS did even better but we'd been on that one for over a week and WYNN was good variety.

Wednesday morning, I said we needed a half-point cut to make the markets happy and Bernanke did not disappoint as our Federal pony once again trotted out his one trick, which reminds my of the Paul Simon lyrics: "Hes a one trick pony – He either fails or he succeeds – He gives his testimony – Then he relaxes in the weeds – Hes got one trick to last a lifetime – But thats all a pony needs." Hey, they didn't hire "Helicopter Ben" to run a tight Federal ship did they? Of course the phrase "putting screen doors in a submarine" doesn't begin to describe the inadequacy of Bernanke's policy but it's always good for a quick boost when we need it.

On Wednesday morning I said: "For now, we NEED to take back last Tuesday’s levels as a minimum goal for the day and we really want to see those 40% lines taken back and held, not just right after the Fed, but through Friday – after the excitement dies down." We had a really strong finish to the week but the FXP March $100s we were hoping to get for $40 over the weekend as disaster protection came all the way down to $30.50 so it will be interesting to see how much follow-through we do get out of China next week. Thursday morning I think I was too bearish as I worried over the still-tight money supply but. aside from our own Fed, global CB's were dumping cash on the market yet we still weren't getting back to the 10/21 levels we had been watching. My only pick that morning post was the IWM May $52s, which did make a nice pop from $5 to $7.27 as the Russell had a very nice 2-day run.

Friday Morning I discussed trading strategies for LVS, GE and GS, which are all doing quite well so far, especially LVS, which popped another 36% on Friday – the gift that keeps on giving. Still, I remain very concerned about the global picture and we made our levels on what seemed like a suspiciously false rally but we caught it during member chat and I even put out a trade on USO CALLS of all things, which did tremendously well from the 12:47 pick. At 12:53, GS gave us the go signal on the rally and the Qs finally broke 33, which was our primary signal to get a little more bullsh. Thankfully, they held it into the close but we're still nervous and will remain so until we see some progress next week.

We have the election to distract us on Tuesday and that is also keeping a lid on the financial news as most papers are concentrating on the election so it may go unnoticed on Monday that no additional funding is pouring into the markets. We have a lot of data hitting the wire including ISM and Construction Spending at 10 am on Monday followed by Auto Sales and Factory Orders on Tuesday. Wednesday we see ADP Employment and ISM Services, Thursday is Unemployment and Q3 Productivity and Friday will give us October Unemployment Rates (7% possible), Pending Home Sales, Wholesale Inventories and Consumer Credit so a big, big week of data!

We have the election to distract us on Tuesday and that is also keeping a lid on the financial news as most papers are concentrating on the election so it may go unnoticed on Monday that no additional funding is pouring into the markets. We have a lot of data hitting the wire including ISM and Construction Spending at 10 am on Monday followed by Auto Sales and Factory Orders on Tuesday. Wednesday we see ADP Employment and ISM Services, Thursday is Unemployment and Q3 Productivity and Friday will give us October Unemployment Rates (7% possible), Pending Home Sales, Wholesale Inventories and Consumer Credit so a big, big week of data!

Earnings have not mattered very much so far as the broader market has tugged companies up and down regardless of their actual reports. There are hundreds of companies reporting next week and Monday we'll be very interested to hear from DRYS, OSK and SPG pre-market and APC, ADP, CROX, EOG, MA, and VIA.B after. Tuesday we get ADM, DF, MVL, JOE, THC and VNO with SAM reporting during the day and NILE and HLS taking us through the election eve, after which the markets mood may change quite a bit. So it's a little more fence-sitting for now but that's better than the 70% bearish stance we ended last week with so let's call it progress!