Fascinating! H/t to Zero Hedge for finding this excellent article by Chris Martenson. (See also Tyler Durden’s "Is The Fed Enabling Foreign Central Banks To Swap Out Their Agency Debt Into Treasuries?") And welcome to Chris Martenson of ChrisMartenson.com!

The Shell Game – How the Federal Reserve is Monetizing Debt

Courtesy of Chris Martenson

Executive Summary

- The Federal Reserve and the federal government are attempting to "plug the gap" caused by a slowdown of private credit/debt creation.

- Non-US demand for the dollar must remain high, or the dollar will fall.

- Demand for US assets is in negative territory for 2009

- The TIC report and Federal Reserve Custody Account are reviewed and compared

- The Federal Reserve has effectively been monetizing US government debt by cleverly enabling foreign central banks to swap their Agency debt for Treasury debt.

- The shell game that the Fed is currently playing obscures the fact that money is being printed out of thin air and used to buy US government debt.

The Federal Reserve is monetizing US Treasury debt and is doing so openly, both through its $300 billion commitment to buy Treasuries and by engaging in a sleight of hand maneuver that would make a street hustler from Brooklyn blush.

This report will wade through some technical details in order to illuminate a complicated issue, but you should take the time to learn about this because it is essential to understanding what the future may hold.

One of the most important questions of the day concerns how the dollar will fare in the coming months and years. If you are working for a wage, it is essential to know whether you should save or spend that money. If you have assets to protect, where you place those monies is vitally important and could make the difference between a relatively pleasant future and a difficult one. If you have any interest at all in where interest rates are headed, you’ll want to understand this story.

There are three major tripwires strung across our landscape, any of which could rather suddenly change the game, if triggered. One is a sudden rush into material goods and commodities, that might occur if (or when) the truly wealthy ever catch on that paper wealth is a doomed concept. A second would occur if (or when) the largest and most dangerous bubble of them all, government debt, finally bursts. And the third concerns the dollar itself.

In this report, we will explore the relationship between those last two tripwires, government debt and the dollar.

Replacing private credit with public credit

Our entire monetary system, and by extension our economy, is a Ponzi economy in the sense that it really only operates well when in expansion mode. Even a slight regression triggers massive panics and disruptions that seem wholly inconsistent with the relative change, unless one understands that expansion is more or less a requirement of our type of monetary and economic system. Without expansion, the system first labors and then destroys wealth far our of proportion to the decline itself.

What fuels expansion in a debt-based money system? Why, new debt (or credit), of course! So one of the things we keep a very close eye on over here at Martenson Central, as they do at the Federal Reserve, is the rate of debt creation.

One of the big themes in the current credit bubble collapse is the extent to which private credit has been collapsing and the corresponding degree to which the Federal Reserve has been purchasing debt and the federal government has stepped up its borrowing. In essence, public debt purchases and new borrowing has attempted to plug the gap left by a shortfall in private debt purchases and borrowing.

That’s the scheme right now – the Federal Reserve is creating new money out of thin air to buy debt, while the US government is creating new debt at the most fantastic pace ever seen. The attempt here is to keep aggregate debt growing fast enough to prevent the system from completely seizing up.

How are they doing?

The debt gap

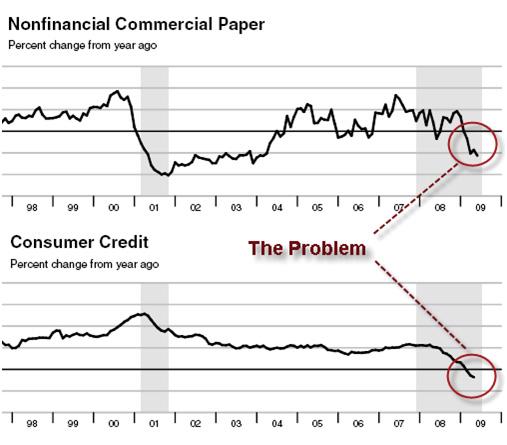

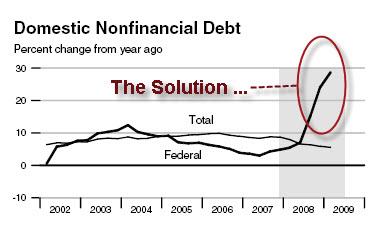

One of the great perks of living in a relatively open society is that we generally get access to pretty good information. The Federal Reserve routinely publishes a document called "Monetary Trends," where they collapse all their points of interest into a nice, tidy collection, and then make it available for all to see.

Here’s what caught my eye in the most recent one:

What we see here is federal debt (bottom chart) exploding at a nearly 30% yr/yr rate of change in response to a collapse in corporate and consumer borrowing (top charts).

This raises a most interesting question: "Who is lending the money to accommodate all that federal borrowing?"

Here’s where the story gets interesting.

Treasury International Capital (TIC) flows

Lately, a number of observers have made note of a troubling decline in foreign demand for US paper assets, notably bonds. Worse, it’s even turned into outright selling which will ultimately translate into dollar weakness.

The relative demand for the dollar "out there" in the international Foreign Exchange (or "Forex") market directly impacts the dollar’s strength. If there are more sellers then its value will fall; if there are more buyers, then its value will rise. One way to assess this delicate balance is to ask, "In total, are foreigners buying or selling US assets and what are they doing with those proceeds?"

Luckily for us, the exact answer to this very question is released in a monthly report put out by the Treasury Department, called the Treasury International Capital Flows report, or TIC report for short.

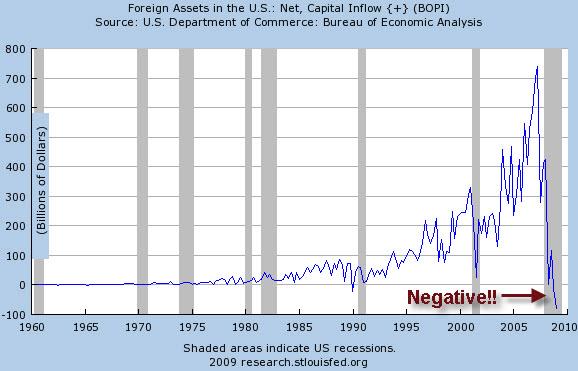

The recent TIC reports have been quite alarming, because they not only reveal the most sudden deceleration in flows in history, but also that they have been negative for some time now. This chart is from the Federal Reserve:

What we see here is that from the early 1990’s onward until 2007, foreigners bought progressively more and more US assets and did so by bringing their money to the US and leaving it there. It is only over the past seven months, out of decades, where that process has reversed and become negative. This is a significant event, to say the least.

On the surface, the above chart hints at a potential disaster for a country that is embarking on the largest-ever federal debt binge in history.

After all, if US assets are being shunned by foreigners, how will we find enough buyers? And what will happen to the dollar?

The answers are: "We won’t" and "Nothing good."

Digging in

If we dig into deeper into the detail of the report, we find something even more interesting. While the overall flows have been negative, there is an enormous difference between the behaviors of foreign central banks and private investors. Fortunately the TIC report distinguishes between these two broad classes of buyers.

Since the start of 2009 and continuing through the month of May, private investors sold $364 billion dollars worth of US assets, while central banks purchased $50 billion dollars worth (source is a .csv file available here from the Treasury). Added up, some $314 billion dollars of foreign money has left the country since the start of the year.

What this demonstrates is the utter reliance of the entire house of cards upon the continued purchase of US financial assets by foreign central banks. Without the continued cooperation of the foreign central banks in accumulating US assets, suffice it to say that the dollar will fall a lot lower than it already has.

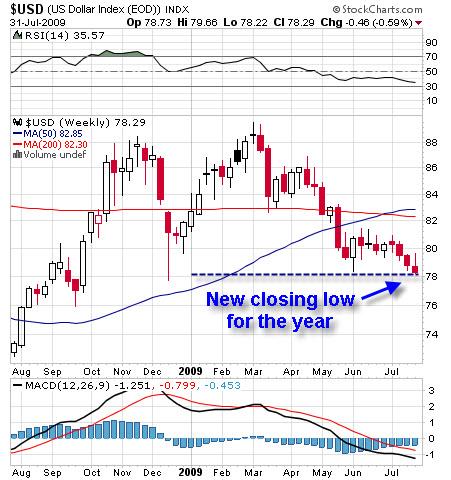

The dollar

Not surprisingly, the dollar recently put in a new closing low for the year (YTD 2009) and is approaching a major area of support and resistance. If it breaks through, we could be looking at a rapid game-changer here.

Of course, I’ve said all this before, and every time we seem to get close, there’s been an upside surprise in store. The forces aligned to prevent a dollar collapse are numerous.

But the same risk remains, and the fundamental picture concerning the dollar has not changed since I first became wary of its fortunes in 2002. In fact, it’s grown worse. Federal deficits are higher than I ever imagined possible (13% of GDP!), and now the TIC flows are negative. The only somewhat bright(er) spot is that the trade deficit has shrunk quite a bit. However, it, too, remains solidly in negative territory, meaning it continues to apply pressure to the value of the dollar by increasing the total number of dollars that need to find a quiet resting place outside of the country.

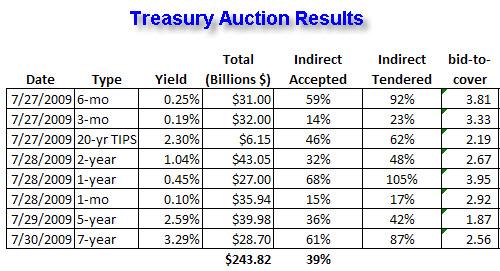

Treasury auctions

During this past business week (July 27th – 31st, 2009), the US Treasury auctioned off more than $243 billion worth of various Treasury bills and bonds. "Indirect bidders," assumed to be mainly central banks, took an astonishing 39% of the total, or nearly $95 billion worth.

With the exception of the 5-year auction, which mysteriously stank up the joint with a worrisome bid-to-cover ratio well below 2.0 (the bond market behaved poorly upon the release of that news item), the story here is that foreign central banks are buying up vast quantities of Treasury offerings.

Wait a minute, hold on there…I thought we just talked about how the TIC report said that foreign central banks have only bought $50 billion in total US paper assets through May – and now they are said to be buying $95 billion during a single week in July alone?

Something is not adding up here.

To understand what, and to get to the essence of the shell game, we need to visit one more source of information – something called the Federal Reserve Custody Account.

The Federal Reserve Custody Account

It turns out that when China’s central bank (or any other foreign central bank) decides to buy either US agency or Treasury bonds, they do not walk up to some window somewhere, hand over a pile of cash, and then take some nice looking bonds home with them in a suitcase.

Instead, what happens is that the Federal Reserve actually holds the bonds (or rather an electronic entry representing the bonds) in a special account for these various central banks. This is called the "Custody Account" and it holds US debt ‘in custody’ for various central banks. Think of it as a magnificently vast brokerage/checking account, run by the Federal Reserve for central banks, and you’ll have the right image.

Although the TIC report shows flows of capital into and out of the country, it does not show you what is going on with those funds that are already in the country. If you look again at the first chart in this report, and behold the vast flows of money that came into the US between 1995 and 2008, you can get a sense of how much money got sent to the US and mostly remains parked there.

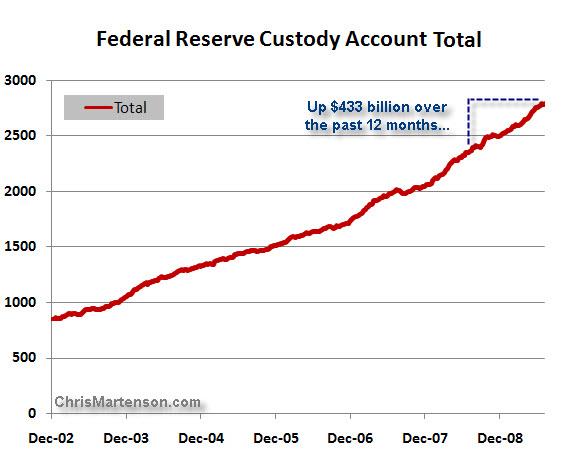

The custody account currently stands at $2.787 trillion (with a "t") dollars. It has increased by over $430 billion the past 12 months and by more than $275 billion in 2009 alone (through July 29). These are truly shocking numbers, and they tell us that foreign central banks have been accumulating US debt instruments throughout the crisis.

As we can see in the chart below, there has been absolutely no deflection in the growth of the custody account as a consequence of the financial crisis, bottoming trade, or the local needs of the countries involved. It’s almost as if the custody account is completely disconnected from the world around it. If you can spot the credit bubble crisis on this chart, you have sharper eyes than me.

What does such a chart imply? We might wonder what sorts of distortions are created by having such a massive monetary spigot aimed from several central banks towards a single country. We also might question just how sustainable such an arrangement really is. It is a complete mystery how such a chart can display nary a wiggle, despite all that has recently transpired.

This next table showing the yearly changes in the custody account actually surprises me quite a bit.

Despite everything that’s been going on, the custody account is on track to grow by the largest dollar amount on record this year, nearly $500 billion dollars (if the current pace continues). Where is all this money coming from and for how much longer?

Understanding the gap between the TIC and the Custody numbers

One thing you might have noticed is that the TIC report only shows $50 billion in foreign bank inflows for 2009, while the custody account grew by $277 billion.

How is it possible for the TIC report to show smaller inflows than growth in the custody account? We can see that clearly in this table, which compares the two. (Note: These are 12 monthly yr/yr changes, so the numbers will be different than the YTD numbers I just cited):

.jpg)

One explanation is that the custody account, at some $2.7 trillion dollars, is accumulating a lot of interest. If those interest payments are not "sent home" and remain in the account, then the account will grow by enough to more or less explain the difference. For example, the $135 billion difference shown above could be generated by a 5% return to the custody account, which is not an unthinkable rate of interest for that account.

International check kiting

Some people view the custody account as nothing more than an elaborate version of check kiting, played at the central banking level.

An illegal scheme whereby a false line of credit is established by the exchanging of worthless checks between two banks. For instance, a "check kiter" might have empty checking accounts at two different banks, A and B. The kiter writes a check for $50,000 on the Bank A account and deposits it in the Bank B account. If the kiter has good credit at Bank B, he will be able to draw funds against the deposited check before it clears, i.e., is forwarded to Bank A for payment and paid by Bank A. Since the clearing process usually takes a few days, the kiter can use the $50,000 for a few days, and then deposit it in the Bank A account before the $50,000 check drawn on that account clears.

In this game, Central Bank A prints up a bunch of money and buys the debt of Country B. Then the central bank of Country B prints up a bunch of money and buys the debt of Country A.

Both enjoy the appearance of strong demand for their debt, both governments get money to use, and nobody is the wiser. Except that the world’s total stock of central bank reserves keep on growing and growing and growing, as reflected in the custody account, which will someday result in thoroughly unserviceable amounts of debt, an unmanageable flood of money, or both.

If this strikes you as a scam, congratulations; you get it.

If that was all there was to the story, then it would be far less interesting than it actually is. When we dig into the custody account data, we find that the total picture is hiding something quite extraordinary. Even as the total custody account has been growing steadily and faithfully, the composition of that account has been changing dramatically.

.jpg)

Here we note that agency bonds peaked in October of 2008 at nearly a trillion dollars but have declined by $178 billion since then. Treasuries, on the other hand, have increased by over $500 billion over that same span of time. A half a trillion dollars! If you were wondering how the US bond auctions have managed to go so smoothly, here’s part of your answer.

What is going on here? How is it possible that central banks are buying so many Treasury bonds, at the fastest rate of accumulation on record?

It would appear that foreign central banks have been swapping agency bonds for Treasury bonds, but that’s not how the markets work. First, they would have to sell those bonds, before they could use the proceeds to buy government debt. So to whom did they sell those Agency bonds in order to afford the Treasury bonds?

Here we might recall that the Federal Reserve has been buying agency bonds by the hundreds of billions.

The shell game

Have you ever seen a sidewalk magician run the shell game, where a pea under a shell is magically shuffled around – now you see it under this shell, now you see it under that shell, now it disappears completely – or does it? The more it moves around, the more confused you get. If you can only figure out which shell the pea is hidden under, you win! But where is the pea? The point of the game, from the perspective of the street hustler, is to use complexity of motion to confuse the mark.

These are the three critical points to remember as you read further:

- The US government has record amounts of Treasuries to sell.

- Foreign central banks, which have a big pile of agency bonds in their custody account, would like to help but want to keep things somewhat under the radar to avoid scaring the debt markets.

- The Federal Reserve does not want to be seen directly buying US government debt at auctions (and in fact is not permitted to, but many rules have been ‘bent’ worse during this crisis), because that could upset the whole illusion that there is unlimited demand for US government paper, but it also desperately wants to avoid a failed auction.

For various reasons, the Federal Reserve cannot just up and start buying all the Treasury paper that becomes available in record amounts, week after week, month after month.

Instead, it uses this three-step shell game to hide what it is doing under a layer of complexity:

Shell #1: Foreign central banks sell agency debt out of the custody account.

Shell #2: The Federal Reserve buys those agency bonds with money created out of thin air.

Shell #3: Foreign central banks use that very same money to buy Treasuries at the next government auction.

Shuffle, shuffle, shuffle, shuffle, shuffle, SHUFFLE, shuffle! Confused yet?

Don’t be. If we remove the extraneous motion from this strange act, we find that the Federal Reserve is effectively buying government debt at auction. This is exactly, precisely what Zimbabwe did, but with one more step involved, introducing just enough complexity to keep the entire game mostly, but not completely, hidden from sight. They can scramble the shells all they want, but the pea is still there somewhere – the pea being the fact that the Fed is creating money to fund the purchase of US debt.

.jpg)

At the time, the Federal Reserve program to purchase agency bonds was described like this:

Fed to Pump $1.2 Trillion Into Markets

Greatly Expanded Purchases Are Designed to Lower Interest Rates, Stimulate Borrowing

The Federal Reserve yesterday escalated its massive campaign to stabilize the economy, saying it would flood the financial system with an additional $1.2 trillion.

In its statement yesterday, the Fed said it will increase its purchases of mortgage-backed securities by $750 billion, on top of $500 billion previously announced, and double, to $200 billion, its purchases of [Agency] debt in housing-finance firms such as Fannie Mae and Freddie Mac.

While "stimulating borrowing," "stabilizing the economy," and "lowering interest rates" are laudable goals, the primary goal of the program seems to have been something else entirely – to assure plentiful funds for the massive US Treasury auctions coming due. I saw nothing in any article I read about this program that even suggested that one of the goals was to allow foreign central banks to effectively swap their agency debt for US government debt using money printed from thin air. But that’s clearly one of the outcomes.

The Federal Reserve, for its part, has been quite open about these purchases of Agency debt. It even provides an excellent website with nice graphics, allowing us to track the purchase program.

.jpg)

(Source)

However, this openness only extends to the amounts themselves, not the source(s) of those Agency bonds. This is, in my mind, yet another reason the Fed desperately wishes to avoid an audit. The results would expose the game for what it is.

As we can see in the above chart, the Fed has purchased more than $640 billion of Agency bonds, and has promised to buy more in the near future.

As we now know, at least some of that money has been recycled into US government debt, where "indirect bidders" have been snapping up an unusually high proportion of the recent offerings. (Note: The way Indirect bidders are calculated has recently changed, and I am not entirely clear on how much this influences the numbers we now see….I’m working on it).

A fair question to ask here is, "If there are green shoots everywhere and the stock market is racing off to new yearly highs, why is the Fed continuing to pump money into the system at these mind-boggling rates?" One answer could be, "Because things might not be as rosy as they seem."

Conclusion

The Federal Reserve has effectively been monetizing far more US government debt than has openly been revealed, by cleverly enabling foreign central banks to swap their agency debt for Treasury debt. This is not a sign of strength and reveals a pattern of trading temporary relief for future difficulties.

This is very nearly the same path that Zimbabwe took, resulting in the complete abandonment of the Zimbabwe dollar as a unit of currency. The difference is in the complexity of the game being played, not the substance of the actions themselves.

When the full scope of this program is more widely recognized, ever more pressure will fall upon the dollar, as more and more private investors shun the dollar and all dollar-denominated instruments as stores of value and wealth. This will further burden the efforts of the various central banks around the world as they endeavor to meet the vast borrowing desires of the US government.

One possible result of the abandonment of these efforts is a wholesale flight out of the dollar and into other assets. To US residents, this will be experienced as rapidly rising import costs and increasing costs for all internationally-traded basic commodities, especially food items. For the rest of the world, the results will range from discomforting to disastrous, depending on their degree of dollar linkage.

Under these circumstances, "inflation vs. deflation" is not the right frame of reference for understanding the potential impacts. For example, it would be possible for most of the world to experience falling prices, even as the US experiences rapidly rising prices (and hikes in interest rates) as a consequence of a falling dollar. Is this inflation or deflation? Both, or neither? Instead, we might properly view it as a currency crisis, with prices along for the ride.

Further, all efforts to supplant private debt creation with public debts should be met with skepticism, because gigantic programs are no substitute for the collective decisions of tens of millions of individuals and cannot realistically meet millions of individual needs in a timely or appropriate manner.

The shell game that the Fed is currently playing does not change the basic equation: Money is being printed out of thin air so that it can be used to buy US government debt.

My advice is to keep these potential issues and insights in sharp focus, make what moves you can to diversify out of dollars, and be ready to move rapidly with the rest. This game is far from over.

Your faithful information scout,

Chris Martenson