{kind=link}

Uh-oh!

Uh-oh!

Wasn't it just 2 days ago that the EU was all set to pop the ESM to $1.25Tn and the IMF was going to add another Trillion and the Fed was talking about more QE in the $1.25Tn range, which plunged the Dollar to multi-week lows? Shouldn't adding 6% of the entire planet's GDP in additional stimulus give us more than a one-day pop in the markets?

As I pointed out in Monday's Morning Alert to Members – these are all just RUMORS and my conclusion in the Alert was:

Despite the bullish turn of events (which we anticipated last week) we're more inclined to cash out our bullish trades into the excitement and press our bear bets and TOMORROW, if we're still over our levels – THEN we will scramble to add some aggressive bullish trades to our virtual portfolios. Again, I cannot stress enough that CASH is my preferred position because this market is tough to call and you need to be very flexible and very nimble to trade it.

We proceeded as planned and, so far, we haven't had any reason to capitulate and get more bullish and that is both surprising and disappointing as this is the end of the first quarter of 2012 – if not now – when? As David Fry notes:

We proceeded as planned and, so far, we haven't had any reason to capitulate and get more bullish and that is both surprising and disappointing as this is the end of the first quarter of 2012 – if not now – when? As David Fry notes:

Monday’s rally was typical as we head toward the end of the quarter. Hedge fund performance fees are on the line and any way to boost these profits is job one. Top holdings for hedge funds include the usual suspects: AAPL, IBM, INTC, BAC, DIS, HD etc.

With little volume it’s easy for algos and hedge funds to prop stocks on little hard news. Tuesday we briefly saw more of this. Just as markets were weakening a story appeared using the Fed’s favorite oracle, the WSJ, as Fed governor Rosengren stated, “more stimulus is on the table”. Immediately HFT algos jumped and markets rose if only briefly.

It's very exciting for us as PLCN (see Thursday's notes) went all the way up to $736 on Monday and sold off on some pretty heavy trading yesterday. Slowly but surely, our negative premise is beginning to take shape as Piper Jaffray is finally catching up with us and noting "a sharp decline in unique visitors to Priceline's booking.com" from growth of 61 percent during the fourth quarter to growth of just 40 percent during the first quarter through last month.

Could it really be possible that PCLN (with a $36Bn market cap) is NOT worth more than AYR ($650M), ALK ($2.5Bn), ALGT ($1Bn), CPA ($1.2Bn), DAL ($8.3Bn), HA ($267M), JBLU ($1.4Bn), PNCL ($24.7M), RJET ($238M), SKYW ($565M), LUV ($6.4Bn), SAVE ($1.4Bn), UAL ($7Bn) and LCC ($1.2Bn) combined? I didn't leave anyone out, that's the ENTIRE Airline sector.

Could it really be possible that PCLN (with a $36Bn market cap) is NOT worth more than AYR ($650M), ALK ($2.5Bn), ALGT ($1Bn), CPA ($1.2Bn), DAL ($8.3Bn), HA ($267M), JBLU ($1.4Bn), PNCL ($24.7M), RJET ($238M), SKYW ($565M), LUV ($6.4Bn), SAVE ($1.4Bn), UAL ($7Bn) and LCC ($1.2Bn) combined? I didn't leave anyone out, that's the ENTIRE Airline sector.

Not only is PCLN (and several other stocks on our Long Put List) RIDICULOUSLY overpriced to any rational valuation, but now EXPE is making use of their cash to acquire VIA Travel to beef up their operations in a shrinking European market. PCLN, with $4.5Bn in revenues and $1Bn in income is the classic middle-man to cut out as that $4.5Bn is bottom-line profits for Airlines and Hotels, who pay PCLN a fee to fill their seats and rooms. So PCLN is subject to both pressure from their customers as well as a weakening Global economy – a tough act to keep up when your p/e ratio is 35:1.

I'm not going to lecture you on value investing because Gerald Burstyn of Advisor One did such a good job of it this morning. It's been a rough year for value players – as there are few values to be found but, unlike most value investors, we also like to play the short side when we see egregiously OVER-valued stocks like our friends at PCLN, CMG, or our old favorites at GMCR. When an air market pops – there are great fortunes to be made getting on the right side of these stocks when they begin to lose their Momo Mojo.

I'm not going to lecture you on value investing because Gerald Burstyn of Advisor One did such a good job of it this morning. It's been a rough year for value players – as there are few values to be found but, unlike most value investors, we also like to play the short side when we see egregiously OVER-valued stocks like our friends at PCLN, CMG, or our old favorites at GMCR. When an air market pops – there are great fortunes to be made getting on the right side of these stocks when they begin to lose their Momo Mojo.

Note on Dave Fry's China chart, that we're dangerously close to rolling over and that was before last night's 2.66% drop in the Shanghai Composite, dropping that index back below the 50 dma, which was already 6% below the 200 dma and that will drop FXI below it's own critical $37.25 line this morning and all the window dressing in the World is not going to hold up the markets if those Chinese walls come crumbling down.

Can AAPL possibly go up high enough to make us forget China falling apart? They barely managed to make us forget the Nasdaq yesterday as AAPL put up another $8 day (1.3%) but, this time, it was barely enough to hold up the Nasdaq, which had a horrific close after a nice start following AAPL to $616. We are clearly starting to get less bang from our AAPL bucks on the Nasdaq as the overall weakness in the tech sector can no longer be masked by AAPL's success as we once again head into the earnings confessional:

We discussed AAPL's outsided influence on the Nasdaq in yesterday's post and yes, we did take a gamble on the AAPL May $470 puts on Friday, which were $2.15 at the time and now $1.45 for a quick 33% loss. Those can now be rolled up to the May $495 puts at $2.45 for $1 for a net $3.15 entry and it's not that we think AAPL will drop 20% but we do expect a pullback ahead of earnings as concerns about margins begin to surface as wages are rising fast in China and the Baltic Dry Index came off the bottom since January earnings – and who do you think is filling those ships with parts going into China and IPhones, IPods and IPads coming back out? We love AAPL and most of our AAPL bets are bullish – this is a "just in case" play into earnings – that's all….

One thing we're almost always bearish on is oil and in yesterday's morning Alert to Members (10:16) I reminded our Members that $107.50 is our shorting line for oil (/CL in the Futures) and we even added USO April $40 puts at .65 to our virtual $5,000 Portfolio. The oil futures were good for an intraday $1,000 per contract gain as oil pulled back to the $106.50 line where my 11:16 comment to Members is also noted on the chart. We had a nice bounce back to $107.50 and, since then – it's been one nice drop, which has been perfect for our longer-term USO puts and SCO calls.

One thing we're almost always bearish on is oil and in yesterday's morning Alert to Members (10:16) I reminded our Members that $107.50 is our shorting line for oil (/CL in the Futures) and we even added USO April $40 puts at .65 to our virtual $5,000 Portfolio. The oil futures were good for an intraday $1,000 per contract gain as oil pulled back to the $106.50 line where my 11:16 comment to Members is also noted on the chart. We had a nice bounce back to $107.50 and, since then – it's been one nice drop, which has been perfect for our longer-term USO puts and SCO calls.

Hopefully oil will stay down here but we do have inventories at 10:30 and we usually get a run-up into those and a net build of about 2M barrels is already expected so we'll need a pretty good amount to spook oil lower. What's really bothering oil this morning is renewed talk about coordinated International releases of oil reserves to put a damper on runaway gasoline prices as we head into the Spring/Summer driving season. This isn't NEWs – we talked about it last week and CNBC denied it was true but THEY LIED TO YOU! We keep telling you they are crooks and liars and that you should pretty much do the opposite of whatever they say but, sadly, people still like to "stick with Cramer."

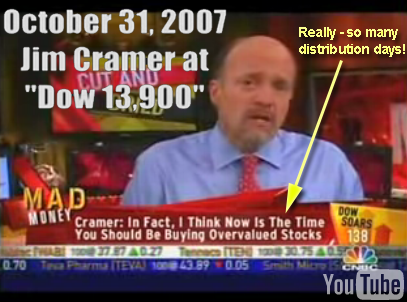

That is, of course, ironic as Cramer isn't sticking with anybody as his web-site, TST, annouces "sweeping layoffs," cutting all of it's Main Street staff as well as some in Boston. As noted by Business Insider "We'd go over the names of people we've been told who are laid off, but it's easier to say who is staying." As you can see from the image on the right – Cramer is giving the same quality advice he was giving back in 2007 – I just can't imagine what's going wrong at The Street….

That is, of course, ironic as Cramer isn't sticking with anybody as his web-site, TST, annouces "sweeping layoffs," cutting all of it's Main Street staff as well as some in Boston. As noted by Business Insider "We'd go over the names of people we've been told who are laid off, but it's easier to say who is staying." As you can see from the image on the right – Cramer is giving the same quality advice he was giving back in 2007 – I just can't imagine what's going wrong at The Street….

What's going on in America is Durable Goods up just 2.2% vs 3% expected in February (with the extra day) and Mortgage Applications down 2.7% after already falling 7.4% last week so that's down 10.1% in two weeks from levels that already SUCKED as rates ticked up from 4.19% to 4.23%. Wow, if consumers are that sensitive to any kind of rate increase, what happens if the Fed DOESN'T keep dropping Trillions on the market – OR – what happens when all those Trillions the Fed is dropping on the market begin to CAUSE rates to increase due to Dollar deflation?

Mr. Rock, meet Mr. Hard Place.