{kind=link}

Courtesy of Lance Roberts, Real Investment Advice

Just recently, the New York Post a very interesting article entitled “Millennials should start taking stocks seriously.” While I am sure the author is well-intentioned, it is a very misguided article in its assumptions.

The author jumps right in with both feet:

“Many millennials are missing the chance to accumulate significant assets.”

There are so many problems with that statement alone its tough to find a starting point.

First, the stock market is not, and never has been, the “solution” to building wealth. If you look around the world, there might be a very small handful that have actually built a fortune by investing alone. That is the exception, not the rule.

The real wealth builder, even for guys like Ray Dalio, Larry Fink, Warren Buffett and others, was not from just investing their own money in the financial markets but by building businesses that invested “other peoples money” in the financial markets from which they collected heavy fees and compensation over time.

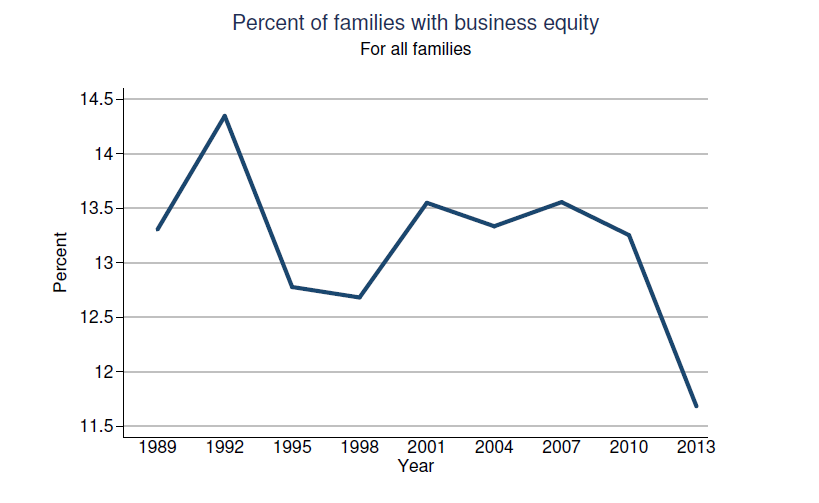

In America, the great “wealth equalizer” is, and always has been, entrepreneurship. But, unfortunately, according to a recent Federal Reserve study, since the financial crisis business equity ownership has declined markedly.

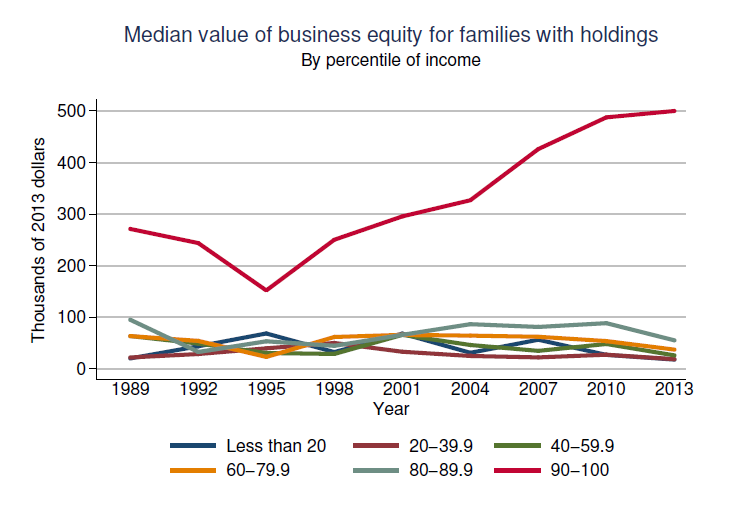

Well, except for those in the top 10%.

(Important Note: This decline in business owner equity goes a long way in explaining why the employment reports don’t reflect economic reality. As I discussed in “Is The BLS Overstating Jobs,” if business owner equity is on the decline, the number of business “births” assumed by the BLS may have inflated employment by over 5-million jobs since the financial crisis. Such inflation would explain the lack of wage growth.)

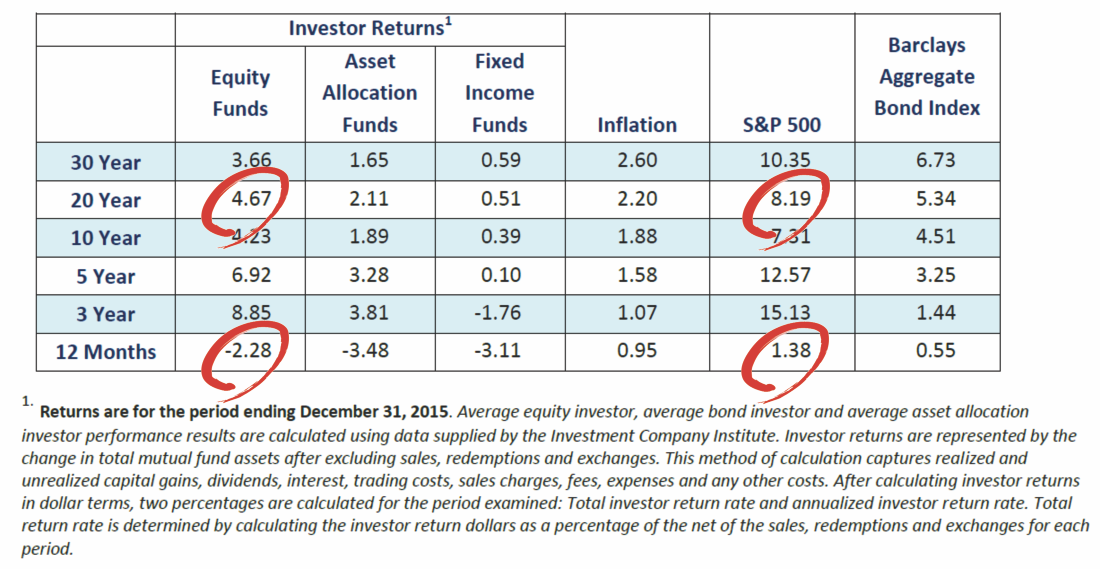

Secondly, investing in financial markets was never intended to be a “wealth builder,” but rather an “inflation adjustment” for “savings” over time.

Over a 30-year period, investors barely generated returns sufficient enough to offset the rate of inflation. Add-in the effect of taxation and the outcome was far worse.

Furthermore, what the author completely misses is the importance of “time” and the impact of “loss.”

Individuals only have a finite amount of time to invest for retirement. While it is great to show 100 year plus charts of the return of an invested dollar in the financial markets, that is not reality. Most individuals, by the point in life that they have available capital, have at best 15-20 years to invest.

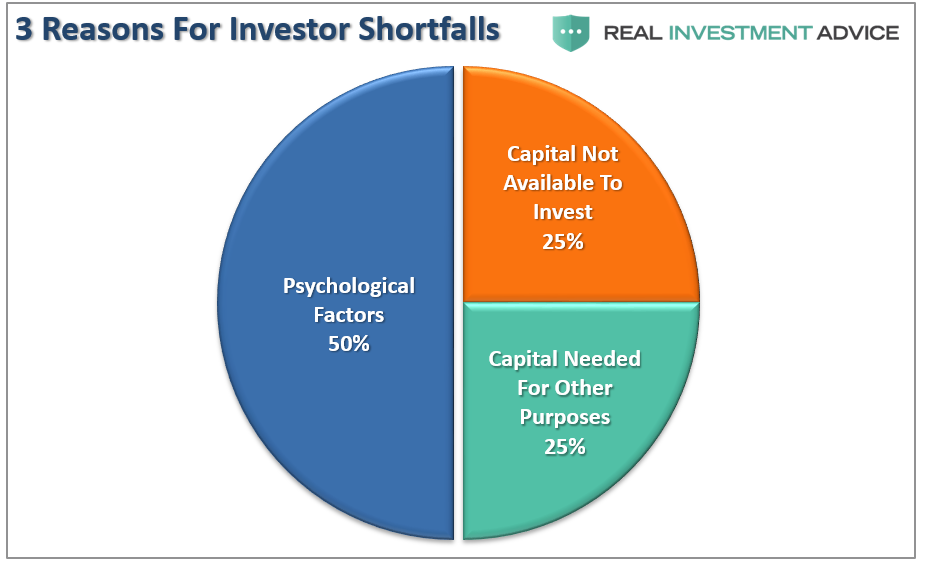

“Notice that “fees” are not an issue. The real problem for individuals can be reduced to just two primary issues: a lack of capital to invest and psychology. I will not deny that “costs” are an important consideration when choosing between two specific investment options; however, the emotional mistakes made by investors over time are much more important.”

The lack of capital is hugely important in the ability to generate “wealth” from the stock market. There has not yet been an investment program invented that did not require actual capital to invest at the beginning. Even according to recent surveys:

“The Bankrate.com survey found that 52% of Americans have no stock market holdings at all. None. In 2002, it was just 33%. Among those who don’t invest today, 53% said they don’t have the money, and 21% said they don’t trust advisers.”

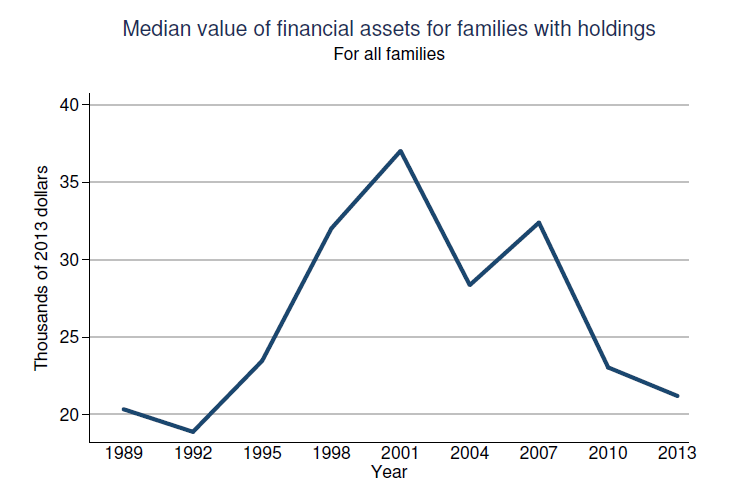

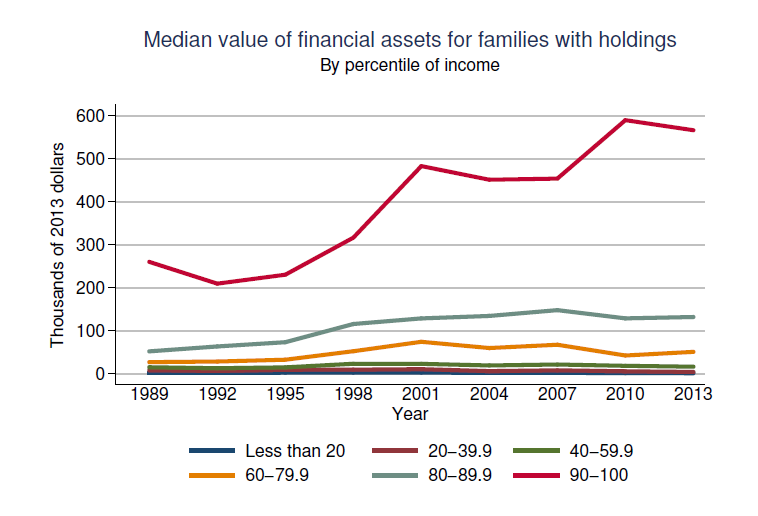

The median value of financial assets for families has fallen sharply since the turn of the century. Note that there are nearly 60% MORE Americans with no stock market holdings today than in 2002. This aligns with the Federal Reserve study which showed a significant plunge in families with holdings.

Again, except for those in the top 10 percent of the population.

Of course, after two very nasty “bear markets” since the turn of the century is not surprising that few individuals have capital remaining to invest or trust the “financial advisors” who lost it for them.

The impact of a bear market is vastly important to future returns. I dug this article up by Sara Max from Time.com wrote:

“In fact, investors who’ve had the bad luck of getting in at the very top of a market have ultimately come out ahead – provided they stayed the course. Consider this analysis from wealth management tech company CircleBlack: An investor who put $1,000 in the Standard & Poor’s 500 index of U.S. stocks at the beginning of 2008 (when stocks fell 37%) and again in early 2009 would have been back in positive territory by the end of 2009.”

This is what my Dad would have called “PPA – Piss Poor Analysis.”

While it is true that someone who invested a $1 at the peak of the market in 2008 and another dollar at the bottom in 2009 would have now gotten back to even, unfortunately, they were not able to regain the 7-years to retirement lost in doing so. The importance of “lost time” can not be overstated enough.

While there have been massive breakthroughs in science and technology, no one has yet discovered the secret of “eternal youth.”

By the time that most individuals achieve a point in life where incomes and savings rates are great enough to invest excess cash flows, they generally do not have 30 years left to reach their goal. This is why losing 5-7 years of time getting back to “even” is not a viable investment strategy.

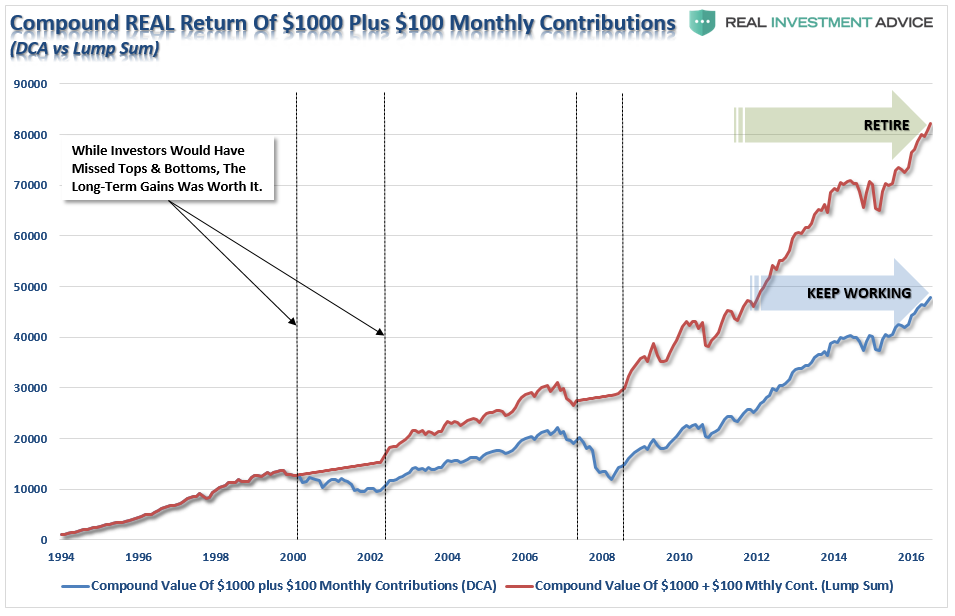

The chart below is the inflation-return of $1000 invested in 1995 with $100 added monthly. The blue line represents the impact of the investment using simple dollar-cost averaging. The red line represents a “lump sum” approach. The lump-sum approach utilizes a simple weekly moving average crossover as a signal to either dollar cost average into a portfolio OR move to cash. The impact of NOT DESTROYING investment capital by buying into a declining market is significant.

Importantly, I am not advocating “market timing” by any means. What I am suggesting is that if you are going to invest into the financial markets, arguably the single most complicated game on the planet, then you need to have some measure to protect your investment capital from significant losses.

While the detrimental effect of a bear market can be eventually be recovered, the time lost during that process can not. This is a point that is consistently missed by the ever bullish media parade chastising individuals for not having their money invested in the financial markets.

The reality is that most of these individuals have never lived through a real bear market, nor have they ever suffered the losses of significant wealth during the process. Their time will eventually come, and as anyone who has been around the financial markets for as long as I have (28 years) will tell you, your attitude about “risk” changes significantly when the “bear begins to maul you.”