{kind=link}

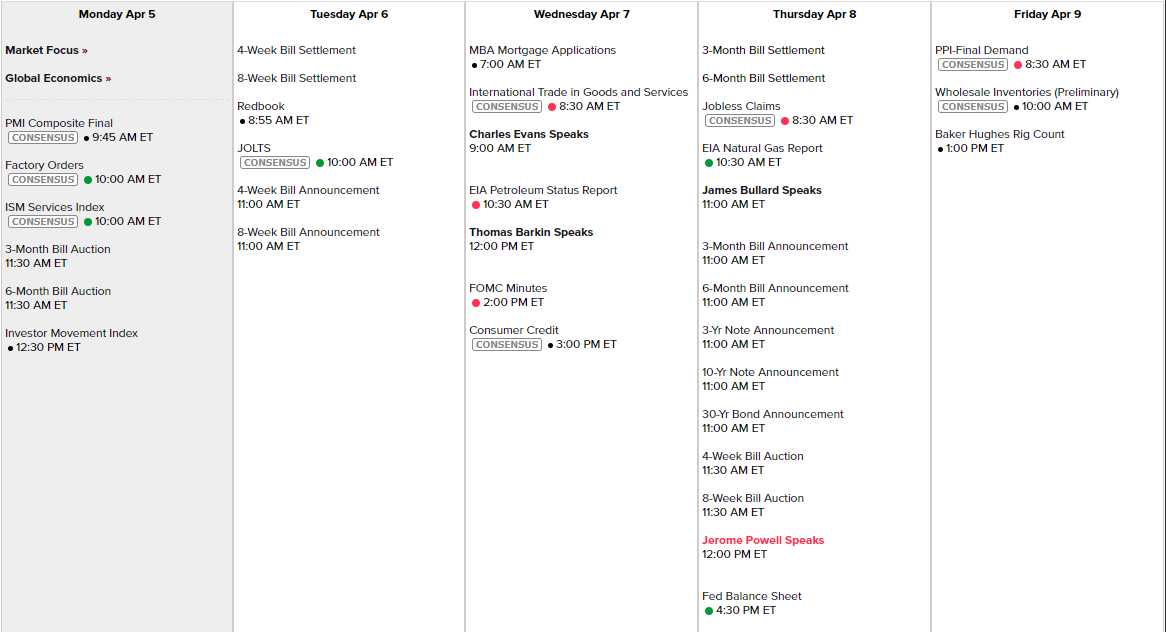

Of course Europe is closed on Easter Monday so it's a very low-volume affair and we'll have to see what sticks this week. We have a few early earnings reports but nothing Earth-shaking. Earnings reports start in earnest next Wednesday, with JPM, GS (and that's all we need to know) along with Wells Fargo, Progressive, First Republic and Bed Bath and Beyond – a very good mix to start earnings season off with.

Until then, we continue to tread water in thin air (there's a mixed metaphor!) and we're thin on Fed speech this week though Powell speaks on Thursday. This morning we have PMI, ISM and Factory Orders, JOLTS tomorrow, Housing, Trade and Fed Minutes Wednesday, along with Consumer Credit, nothing Thursday and PPI and Inventories on Friday. Kind of boring, actually.

Signs, so far, point to a very uneven recovery – despite the strong Jobs Numbers on Friday. Texas will blow up this week as people get their electric bills for last month's storm – people simply can't afford $3,000 electric bills to heat their homes. As you can see from the chart on the left, sub-prime borrowers are getting worse, not better and $1,400 isn't going to fix that mess. Don't forget that mortgage and rent forgiveness will expire one day – and that's a crisis we're just kicking down the road so far.

Signs, so far, point to a very uneven recovery – despite the strong Jobs Numbers on Friday. Texas will blow up this week as people get their electric bills for last month's storm – people simply can't afford $3,000 electric bills to heat their homes. As you can see from the chart on the left, sub-prime borrowers are getting worse, not better and $1,400 isn't going to fix that mess. Don't forget that mortgage and rent forgiveness will expire one day – and that's a crisis we're just kicking down the road so far.

Auto loans are a key indicator of how riskier borrowers are faring. The loans represent the biggest monthly debt payment for many subprime borrowers, who often don’t have mortgages or college debt. Many work in restaurants, hotels and bars that have been hurt badly by Covid-19.

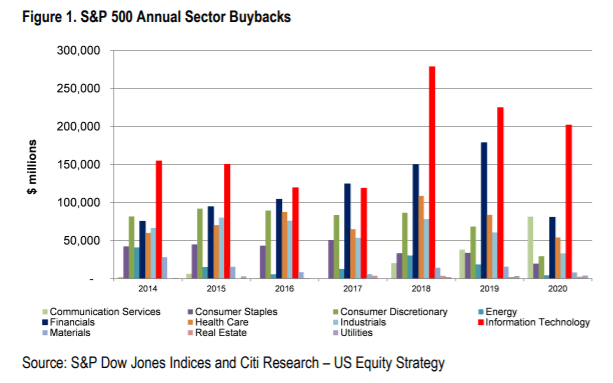

On the other end of the financial spectrum, stock buybacks are a thing again as companies are buying back 30% more stick this year than last year, bringing us back to 2018 levels of buying (which were insane) at 50% higher prices than they were buying the shares before – what could possibly go wrong??? For our beloved Bansters, the Fed announced at the end of last month "the temporary and additional restrictions on bank holding company dividends and share repurchases currently in place will end for most firms after June 30, after completion of the current round of stress tests." Game on!

JP Morgan (JPM) is in the middle of buying back $30Bn of their own stock, which is 6% of it and that will make their earnings APPEAR to be 6% per share higher than they were – NOT because they made more money, but because they have less shares to divide them by – it's BRILLIANT! Does it make sense for JPM to buy their own stock at $155 when it was $100 in November? Depends how much you value appearances, I supose. JPM trades $2.4Bn worth of shares on the average day so $30Bn is about 12.5 days worth of buying by the company itself. Imagine the effect of that on low-volume days….

That's the kind of crazy market we're in and there's no sense in fighing it – we just have to play it until it fails and hope we're quick enough not to get crushed under the correction.

Be careful out there!