{kind=link}

This is not good.

This is not good.

The Russell has fallen 5%, from 2,450 to 2,327.50 (spiking even lower yesterday) and is still weak this morning. Overall, we're back to the pre-spike end of October, which was also the beginning of September (when we called the market toppy and went back to mainly CASH!!!) and that was lower than the June and July highs which were both lower than the top of the Russell we hit in March.

So our broadest index, the one that measures 2,000 companies that are more Main Street than Wall Street, is struggling because, while Coca-Cola (KO) may have pricing power because you are thirsty and don't care about a nickle, the 7-11 you buy it from still gets the same $5 from you for your visit – you just leave with less stuff. We've all experienced that at the grocery store. This is especially true for consumers who are being robbed at the gas pump every week for twice what they paid in 2020.

|

As you can see, the Dow has also given up the November gains and the S&P and the Nasdaq are curling over – perhaps these levels are the top – it's hard to tell on a holiday week but they are all going to be holiday(ish) weeks from now until January 3rd (and I bet we won't be in the mood to work then either).

Oil has given up two months worth of gains as well (but still expensive):

Bonds are collapsing:

|

Even gold and silver have given up their November gains and are both down for the year now. A large part of that reason is that, despite the best efforts of the Fed to debase our currency, the Dollar is up 7% for the year. Why, because the rest of the World is still very worried about their own economies and currency. DESPITE the 7% rise in the Dollar, the US is experiencing 6% (admitted) inflation, which is more like 10% in the real world. Imagine how bad it is in other countries, where their currency buying power is diminishing while prices rise (especially on commodities).

If we lived in reality, I'd say we're on the cusp of a major Global Recession – all the signs are pointing to it EXCEPT stock prices. Even with this month's pullback – we're still generally hovering around the all-time highs so investor sentiment hasn't turned too much – yet, we get that report tomorrow.

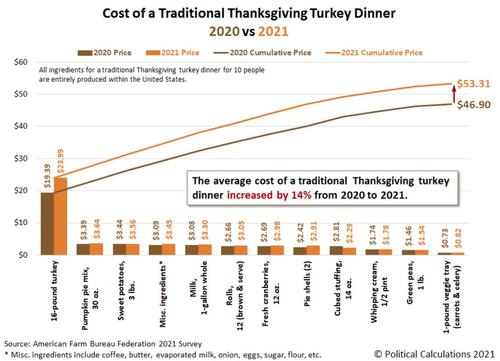

Speaking of reality, the official inflation numbers are in and the price of a Thankgiving Dinner for 10 people has gone up 14% since last year, according to the American Farm Bureau Federation's annual survey. Factors affecting the feast include:

Speaking of reality, the official inflation numbers are in and the price of a Thankgiving Dinner for 10 people has gone up 14% since last year, according to the American Farm Bureau Federation's annual survey. Factors affecting the feast include:

“Dramatic disruptions to the U.S. economy and supply chains over the last 20 months; inflationary pressure throughout the economy; difficulty in predicting demand during the COVID-19 pandemic and high global demand for food, particularly meat.”

Ranking the data this way lets us see that the increase in the cost of turkey is responsible for most of the year-over-year increase. Rising by $4.60 from 2020's $19.39 to 2021's $23.99 for a 16-pound bird, turkey alone accounts for nearly 72% of the year-over-year increase in the total cost for the meal. Shipping costs are mostly to blame but also that, like everything, less turkeys were produced in 2020 due to the lockdowns but the same number of families are ordering them for thier table this year – supply and demand imbalance.

Of course, that's just your food cost – whether you are driving to your Mom's house or turning on the gas to cook for your relatives – everything is more expensive this year. Even ESPN has had two price hikes in 2021!

Speaking of Disney greed, they just stopped selling annual passes into the holidays as they don't generate enough revenue compared to forcing people to buy short-term park options. Isn't Capitalism great?

FROM $194/day?!? Wow, just wow…. That's $800 for a family of 4 to walk in the door. And, once you are inside the park – just a turkey leg will set you back $15! Balloons are $25 – that's what killed me last time I was there (this summer) – $25 for a balloon.

FROM $194/day?!? Wow, just wow…. That's $800 for a family of 4 to walk in the door. And, once you are inside the park – just a turkey leg will set you back $15! Balloons are $25 – that's what killed me last time I was there (this summer) – $25 for a balloon.

Needless to say, not many kids were walking around with balloons. And this has nothing to do with inflation – this is GREED. DIS is making $7.3Bn this year – let the kids who paid $189 to be sold more stuff in the park while being brainwashed to become lifetime Disney consumers at least have a friggin' balloon you greedy bastards!