{kind=link}

Courtesy of Pam Martens

By Pam Martens and Russ Martens

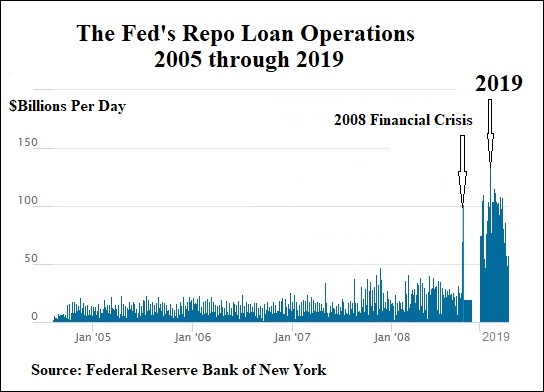

The conventional wisdom is that the Fed’s recent emergency lending facilities to Wall Street were caused by the COVID-19 crisis. The above chart, which uses the New York Fed’s own Excel spreadsheet repo loan data, shows the conventional wisdom is dangerously wrong.

In the last quarter of 2019 – before there was any news of COVID-19 in the U.S., and months before the World Health Organization declared COVID-19 a pandemic – the Fed pumped $4.5 trillion in cumulative repo loans to unnamed trading houses on Wall Street – its so-called “primary dealers.”

The collateral that the Fed accepted for the cumulative $4.5 trillion in loans consisted of $3.497 trillion in U.S. Treasury securities; $988.3 billion in agency Mortgage-Backed Securities (MBS); and $15.839 billion in agency debt.

The Fed’s emergency repo loan operations began on September 17, 2019. From September 17, 2019 through the last acknowledged operation on July 2, 2020, the Fed’s repo loans cumulatively totaled $11.23 trillion, made up of the following pledged collateral: $7.137 trillion in U.S. Treasury securities; $4 trillion in agency Mortgage-Backed Securities (MBS) and $91.525 billion in agency debt.

…