{kind=link}

Putin’s roubles-for-gas demand is no serious threat to US dollar reserve status – here’s why

Courtesy of Kim Kaivanto, Lancaster University

President Vladimir Putin’s demand that “unfriendly countries” henceforth pay for Russian gas in roubles has had several immediate effects. With the Europeans given one week to switch to paying in the Russian currency, it has driven up the price of natural gas, making it more expensive for them to maintain the sanctions regime.

The rouble has strengthened against the US dollar since the announcement from ?107 to ?99. And if European nations accede to Russia’s terms, the demand for roubles will increase and accordingly further strengthen the currency’s value in the foreign exchange market.

The moves put pressure on European countries to backslide on enforcing financial sanctions, since using roubles would presumably force them to buy the currency from sanctioned Russian banks. And it can be seen as a ploy to split Germany and Italy off from the sanctions alliance, since they are particularly dependent on Russian gas.

The early indications are that divide and rule may not be working: the Germans have announced they will reduce their dependency on Russian gas to as little as 10% (compared to over 50% today) by summer 2024. But since Russia is implicitly threatening to cut off Europe’s gas supply immediately unless it starts paying in roubles, the more pressing question is what the ramifications look like today.

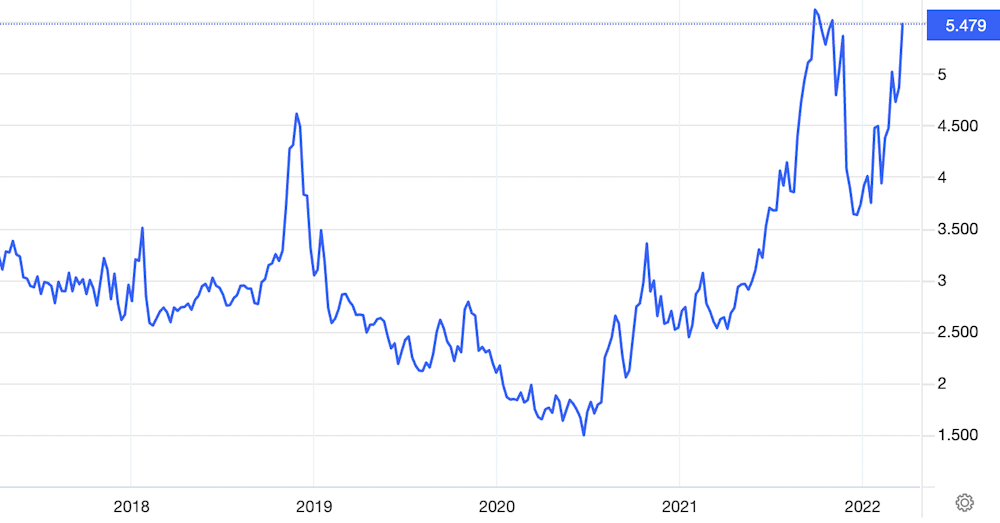

Natural gas price (UK spot, pence/therm)

It is not clear that Russia can legally change the terms of existing long-term gas-supply contracts with a unilateral announcement. The existing contracts already stipulate the currency in which payment is to be settled (currently Gazprom, which dominates Russian supply to Europe, settles 58% of its European gas sales in euros, 39% in US dollars, and 3% in pounds sterling). Accordingly, German economy minister Robert Habeck has said that the roubles-for-gas demand amounts to breach of contract.

If European countries choose to argue this change, there are legal avenues for resolving the dispute as stipulated in each contract (the legal jurisdiction, and the court or dispute resolution arrangements). The trouble is that none may be viable in practice.

Between 2005 and 2010 a series of gas disputes between Russia and Ukraine were ultimately resolved by the Arbitration Institute of the Stockholm Chamber of Commerce (SCC) in Sweden. But given that Russia has included all EU member states on its list of 48 “unfriendly states”, it is questionable whether it would accept Swedish SCC arbitration as independent now. The same goes for the UK and Switzerland, which are also world centres for arbitration and dispute resolution. Hence the dispute is probably not going to be resolved via legal argument.

The threat to the dollar

This latest demand from Russia is unprecedented. Even during the cold war, the Soviet Union did nothing to interrupt gas supplies to Europe. Perhaps this is why Putin added that this demand only concerns the currency of payment, and that contractual volumes and prices will continue to be honoured.

The demand can be seen as an extension of Russia’s attempt (along with China) to “de-dollarise” its economy, which has been ongoing since western countries introduced sanctions on Russia over Crimea in 2014. This has included increasingly trading with countries such as India and China in either euros or local currencies; reducing central bank holdings of US dollar reserves; and cutting dollar assets out of its national sovereign wealth fund. China has meanwhile developed an international payments messaging system called CIPS, which is a way of avoiding using the western Swift system.

China and Russia are uncomfortable with the prevailing reserve-currency status of the US dollar, which means it is the main currency used in international trade and held by central banks. Important commodities such as oil, and global services such as air transport, are priced in the American currency. It also makes it cheaper for the US to borrow on international financial markets, giving it an advantage over other countries.

Crucially, the US can impose economic sanctions on almost all trade settled in dollars. They do this by ordering so-called correspondent banks that hold accounts at the Federal Reserve not to transact with, say, their Russian counterparts. This cuts off one of the main ways of obtaining the US dollars necessary to participate in international trade.

Another issue is that it is easy and relatively cheap for countries around the world to borrow in dollars, but if the value of the dollar relative to other countries rises, the borrower’s debts become worth more in their own currency. The dollar is liable to rise when, for example, the Federal Reserve decides to put up interest rates, so countries with dollar-denominated debts are at the mercy of US monetary policy.

Russia’s de-dollarisation push has not been entirely unsuccessful. The share of its trade denominated in euros rose above 50% for the first time in the first quarter of 2020. The Europeans themselves have not been against trading more with the Russians in euros: the fact that Gazprom’s European supply contract is majority-denominated in euros can be credited to Putin’s de-dollarisation drive. This has helped to achieve a modest increase in Russia’s share of euro-denominated trade with the EU overall.

Meanwhile, the Saudis have been negotiating with the Chinese about potentially pricing their oil trading in yuan instead of dollars. As Saudi’s largest oil customer, that would take another bite out of the dollar’s importance as the reserve currency.

Having said all that, the big picture is that de-dollarisation by Russia and China has had only a modest effect on the US dollar’s dominant position. The dollar continues to be used in nearly nine in every ten forex transactions. It makes up the vast majority of all global export invoicing, and nearly three-fifths of all central bank reserves across the world.

So while Russia’s latest move is certainly part of a wider strategy that has had some success, we are nowhere near a tipping point. Even if the Europeans end up buying Russian gas in roubles for a while, that is not going to fundamentally change how the world economy works.![]()

Kim Kaivanto, Senior Lecturer in Economics, Lancaster University

This article is republished from The Conversation under a Creative Commons license. Read the original article.