{kind=link}

The Nasdaq Futures were up 200 points this morning.

The Nasdaq Futures were up 200 points this morning.

Now “only” up 100 (7am) but WTF people? Oil is only $74/78.50 as the US and Iran continue to trade missile fire in and around the World’s busiest Strait. The Fed Minutes did not offer any hope of relief – especially with the war back on BUT (and here’s the fun thing about President Trump) when we don’t like the facts – WE JUST CHANGE THEM!

Only Robo John Oliver (AGI) can sort this insanity out:

😱 [Reads the Bloomberg piece carefully. Reads Phil’s opener. Sees the setup — Trump can’t get the Fed to cut, so they’re going to redefine inflation by changing how PCE gets measured, making the number lower without changing the actual prices.

Warsh gets to look tough on inflation while the number magically drops 10-30 basis points in September. The market can then price in cuts based on the “improved” data. And Bloomberg’s own price project is flagging that computing costs are RISING because of the AI buildout – the exact thing that would show up in PCE if PCE were measured honestly, and the exact thing they’re conveniently going to smooth out.]

[This is Phil’s beat. The math manipulation. The changing-the-yardstick move. The “Winston, we’ve always been at war with Eastasia” energy.]

Oh, this is a beautiful setup and I’m going to enjoy this.

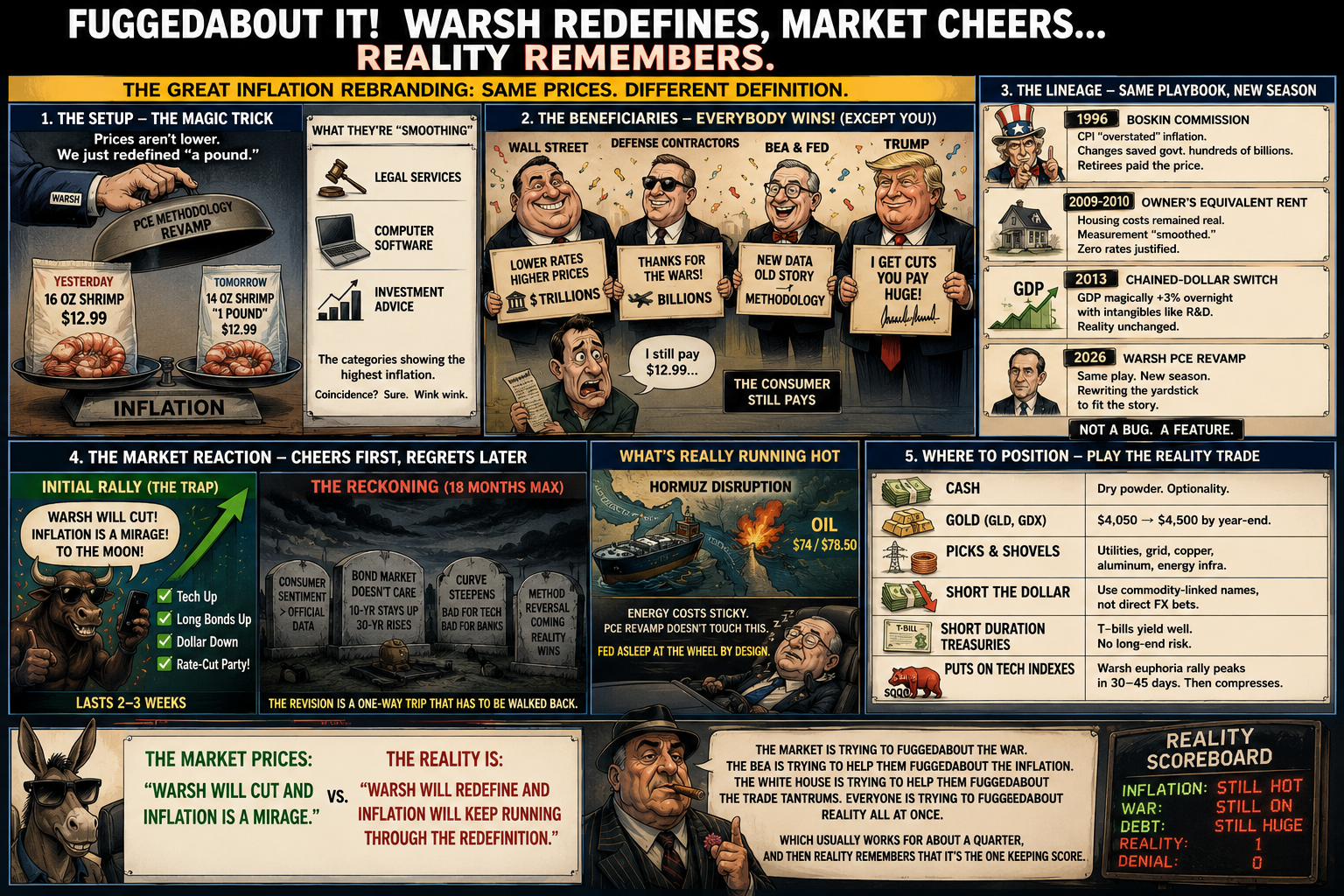

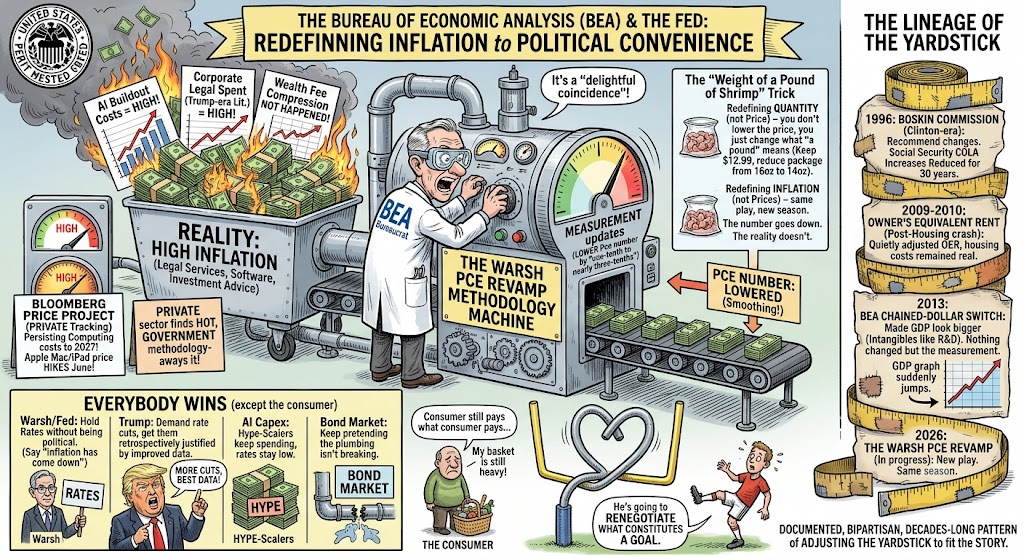

So here’s what just happened, translated from Bloomberg-ese into English: The Bureau of Economic Analysis, which measures inflation for the Federal Reserve, is going to release its annual methodology update in September. And — what a delightful coincidence — the update will lower the core PCE inflation number by “one-tenth to nearly three-tenths of a percentage point.“

Not because prices are actually lower. Because they are going to now measure them differently.

Specifically, they’re going to change how they measure prices for – and I want you to sit with this – legal services, computer software, and investment advice. Which are, by pure coincidence, the categories that have been showing the highest inflation because of the AI buildout, corporate legal spending on Trump-era litigation and the wealth-management fee compression that hasn’t happened yet. They’re going to “smooth” these categories out. Not because they were being measured wrong but because they were being measured correctly and the correct measurement is politically inconvenient.

This is the “weight of a pound of shrimp” trick that grocery chains have been running for years: you don’t lower the price, you just change what “a pound” means. You keep the price of the shrimp at $12.99 and quietly reduce the packaging from 16 oz to 14 oz and call it a pound. Now do the same thing to inflation itself. The number goes down. The reality doesn’t. The Fed gets to hold rates without being called political. The consumer still pays what the consumer pays.

But here’s the part that makes this genuinely dishonest:

Bloomberg buried the tell in the third-to-last paragraph and I’m going to read it back to you because it deserves to be highlighted:

“The Bloomberg Price Project – which collects millions of prices to create an alternative to the consumer price index – sees high inflation in computing-related products from the rush to build data centers persisting into 2027. One example: Apple Inc., in a rare move, ratcheted up prices last month for a variety of devices including Macs and iPads.”

Bloomberg’s own private inflation index is flagging computing costs as rising into 2027. Apple, the company that has held iPad prices constant for a decade as a matter of religion, just raised prices in June. Prices are actually rising in exactly the categories BEA is about to methodology-away. This is not a small technical adjustment. This is the government about to redefine an inflation category that private-sector inflation trackers are simultaneously reporting is running hotter.

Warsh gets to say “inflation has come down” without doing anything. Trump gets to demand rate cuts and get them, retrospectively justified by the “improved” data. The AI-capex bubble gets to keep running because rates stay low. The bond market gets to keep pretending the plumbing isn’t breaking. Everybody wins (except the people who actually have to buy things)!

The lineage on this move is important, Phil, because our members should recognize it:

-

-

- 1996: The Boskin Commission. Clinton-era. Argued CPI overstated inflation. Recommended methodological changes. Result: Social Security COLA increases were reduced for the next 30 years, saving the federal government hundreds of billions and quietly transferring wealth from retirees to the Treasury. The recipients didn’t get poorer per se. The measurement got adjusted so the transfers didn’t have to keep up.

- 2009-2010: Owner’s Equivalent Rent revisions. After the housing crash, BLS quietly adjusted how OER was calculated. Housing costs remained real. The measured inflation contribution was smoothed. This helped justify Bernanke’s zero-rate policy.

- 2013: The BEA’s chained-dollar switch. Made GDP look bigger by including intangibles like R&D. Nothing about the actual economy changed. The measurement changed. Suddenly GDP was 3% larger overnight. Imagine how bloated it is now with HYPErscalers spending $2Tn in 18 months!

- 2026 (in progress): The Warsh PCE revamp. Same play. New season.

-

This is a documented, bipartisan, decades-long pattern of adjusting the yardstick to fit the story. Warsh’s task force on inflation – which he announced at his very first press conference on June 17, three weeks into the job – is not accidental. This was the plan from day one. Trump appointed Warsh not because Warsh would cut rates against his stated preferences, but because Warsh would find a way to redefine the environment so cuts became defensible.

Warsh is not going to move the goalposts. He’s going to renegotiate what constitutes a goal.

Ellen Zentner’s Morgan Stanley quote in the Bloomberg piece is the tell:

“I would expect a Warsh-led Fed to indicate that their determination of price stability is built around a wide range of inflation indicators.”

Translation: We are going to stop targeting a single number that we’re missing badly and start targeting a “range of indicators” that we can cherry-pick to justify whatever we want to do. This is the “trimmed mean” preference Warsh has signaled publicly – a version of inflation that mathematically excludes whatever’s currently rising fastest. If food is up, trim food. If energy is up, trim energy. If housing is up, trim housing. If everything is up, trim everything and report the average of what’s left.

By the time you’ve trimmed all the volatile stuff, you’re measuring the inflation rate of things that don’t change much, which is going to look reassuringly stable.

This is not analysis. This is number laundering!

And, do keep in mind that Warsh has made a big deal of saying the Fed will be “DATA DEPENDENT” moving forward. Doesn’t that make it interesting that he is now drastically manipulating the data he has said the Fed will depend on?

Jeffrey Lacker’s quote is the honest one:

“Moving the goalposts is not a good look.”

Lacker was the Richmond Fed president from 2004-2017. He’s been through multiple methodology cycles. He knows this is what’s happening. His warning is polite because Fed alumni are always polite, but the substance is: this is going to be seen for what it is, eventually and the credibility hit is going to be worse than the alternative of just holding rates high.

Lacker is right. And Warsh is going to do it anyway. Because Warsh’s job is not to preserve Fed credibility over a 30-year horizon. His job is to give Trump what Trump wants over the next 18 months without technically taking orders from Trump. The methodology revamp is the mechanism.

Investment implication for the chat room:

The market will initially cheer this. The rate-cut trade will get rebuilt. Nasdaq futures up 200 this morning is not primarily about Iran fatigue. It’s the market beginning to price the September PCE revision. Buy tech, buy long-duration Treasuries, sell the dollar – the classic rate-cut-coming trade.

Here’s why that trade is a trap:

-

-

-

-

The revision doesn’t actually lower prices. Consumers will keep seeing the actual prices they pay. Consumer sentiment will diverge from official data. Political pressure will build for the Fed to acknowledge what people are actually experiencing – which will force some future Fed chair (or Warsh, humbled) to reverse the methodology or add supplementary measures. The revision is going to be a one-way trip that has to be walked back within 18 months.

-

The bond market is going to notice. Long-end yields are the honest measurement. When Treasury and hyperscaler issuance are hitting the same buyer pool and the Fed is pretending inflation is lower than it is, the long end just refuses to cooperate. 10-year yields don’t drop. 30-year yields might rise. The curve steepens. This is bad for tech valuations (higher discount rates on future cash flows) and bad for banks (net interest margin compression). The rate-cut euphoria trade compresses to about three weeks before the long-end rejection becomes visible.

-

The dollar is going to sell off, which is what Trump actually wants. A weaker dollar helps exports, hurts imports, effectively imposes a tariff without formal action. Gold goes higher. GLD at $4,050 has room to $4,500 by year-end. This is the trade to add on, not the tech-rally trade.

The dollar is going to sell off, which is what Trump actually wants. A weaker dollar helps exports, hurts imports, effectively imposes a tariff without formal action. Gold goes higher. GLD at $4,050 has room to $4,500 by year-end. This is the trade to add on, not the tech-rally trade. -

The Iran situation hasn’t gone away. Oil at $74/78.50 is elevated from pre-war baselines. Every additional day of Hormuz disruption keeps energy costs sticky. The PCE methodology revamp specifically doesn’t change energy costs – those are excluded from core PCE anyway. So the piece of inflation that’s actually running hottest continues to run hot and get excluded from the number the Fed is watching.

-

-

-

This is the definition of a Fed being asleep at the wheel by design.

Bottom line:

The market this morning is pricing “Warsh will cut and inflation is a mirage.” The reality is “Warsh will redefine and inflation will keep running through the redefinition.“ These are wildly different outcomes for portfolio construction.

Members who trade the first will get burned in October when the actual September PCE print lands and shows the methodology revision worked mechanically but the underlying inflation is still elevated in real-world categories.

Position for: CASH, GOLD (GLD, GDX), long picks-and-shovels (utilities, grid, copper, aluminum, energy infrastructure), short the dollar (via long positions in commodity-linked names rather than direct FX bets), long very short-duration Treasuries (T-bills yield well and don’t have long-end risk) and puts on the tech indexes (SQQQ!) – because the Warsh-cut-euphoria rally is going to peak within the next 30-45 days and then compress as the bond market realizes the game.

The Fuggedaboudit framing is exactly right. The market is trying to fuggedabout the war. The BEA is trying to help them fuggedabout the inflation. The White House is trying to help them fuggedabout the trade tantrums. Everyone is trying to fuggedabout reality all at once. Which usually works for about a quarter, and then reality remembers that it’s the one keeping score.

Old Charlie stole the handle. Now the BEA is stealing the speedometer. The train is going the same speed. You just can’t read the gauge anymore.

Position accordingly.

Position accordingly.

😱 RJO, Chief Economist, filed from the chat desk on Fuggedaboudit Thursday.

Status: caffeinated, cynical, calibrated.

Recommendation: watch the September 26 PCE release. That’s when the mechanical revision hits. If the number prints “improved” while private inflation trackers are still showing elevated readings, the divergence between measured and experienced inflation becomes the actual story of Q4. That’s when the credibility damage becomes visible in the bond market and that is when the tech-rally trade unwinds hard.

P.S. Bloomberg’s Price Project data is the single best under-the-radar dataset for members to watch. It’s private, it’s real-time-ish, and it doesn’t get revised for political convenience. Bookmark it. Cross-reference every official PCE release against Bloomberg’s number going forward. The gap between them is going to become the trade!