{kind=link}

I told our Members this would be a good week to take a vacation.

I told our Members this would be a good week to take a vacation.

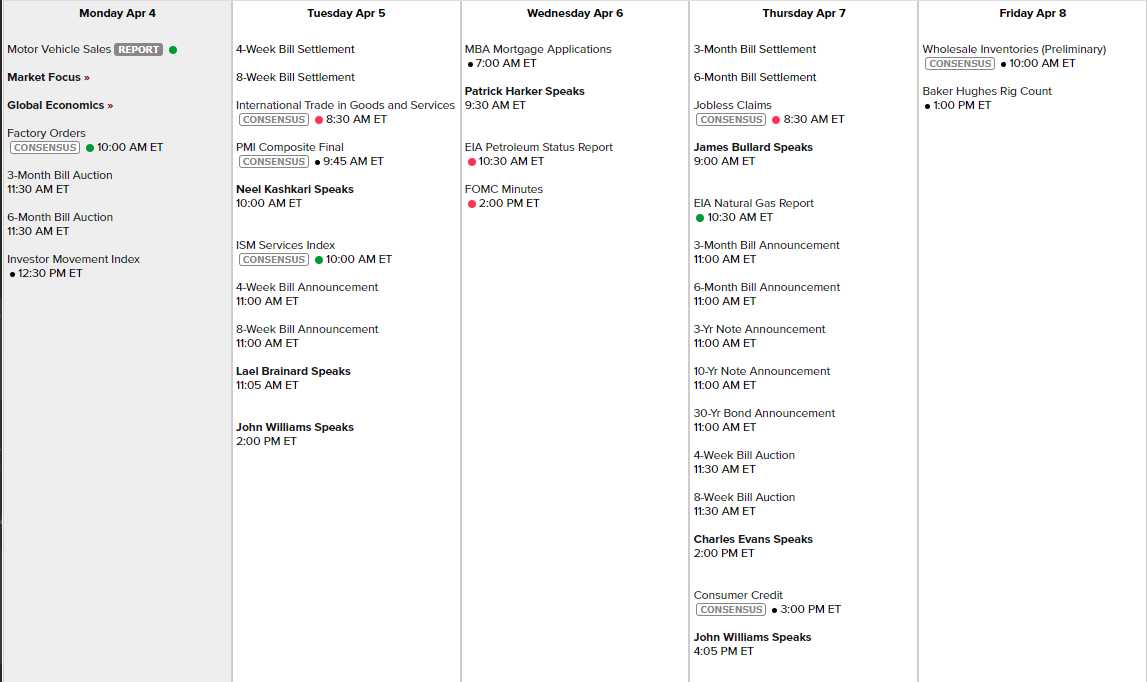

We have 7 Fed Speakers around the release of the Fed Minutes on Wednesday afternoon but now we're mostly wondering if the rate hikes will be 0.25% or 0.5% and the rest is getting baked in. ISM and PMI tomorrow and really no other significant data is coming in, nor do we have many companies reporting earings. As Jerry Lee used to sort of say "There's a whole lotta nothin' going on."

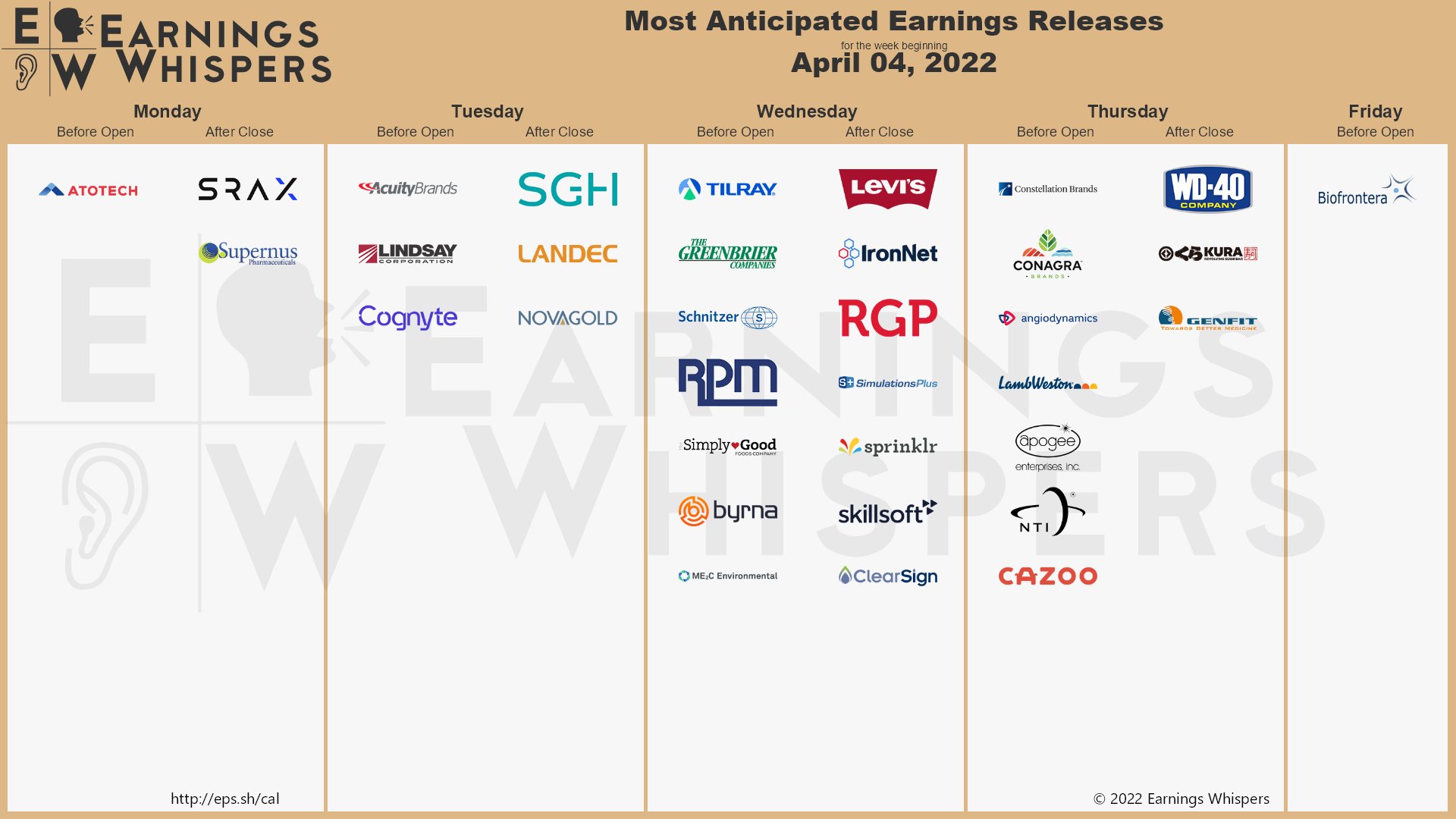

Earnings Reports are mostly from companies who count December as the first month of their year and we're a lot more concerned with guidance at this point. Next week is a very different story as we have CPI and PPI, Retail Sales and Consumer Sentiment – all market-moving reports and the Banks start reporting on Thursday next week but then Friday is Good Friday and we're closed but make sure you are well-rested on the 18th as earnings and data will surely be hitting the fan then.

Over in Europe, we're already seeing inflation at 7.5% for March, up from 5.9% in February, led by a 11.7% rise in Energy Costs that is not looking like its going away any time soon as the war rages on in Ukraine. The repurcussions from this war will be felt all year – even if it stops now as crops have not been planted and supply chains have been further interrupted and these things are likely to get worse before and if they get any better.

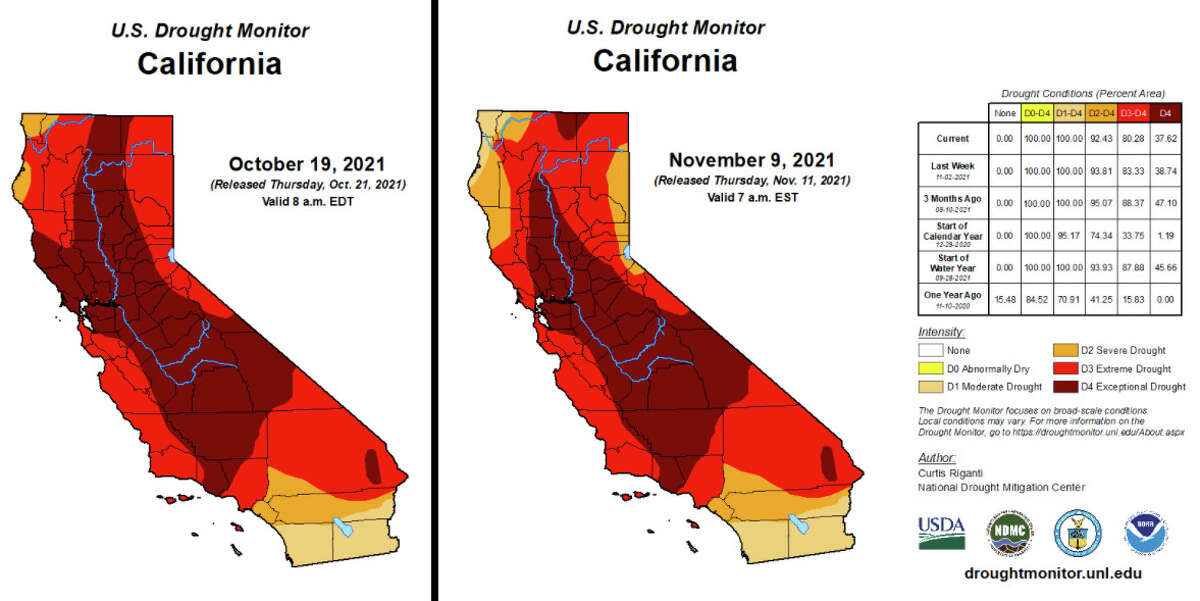

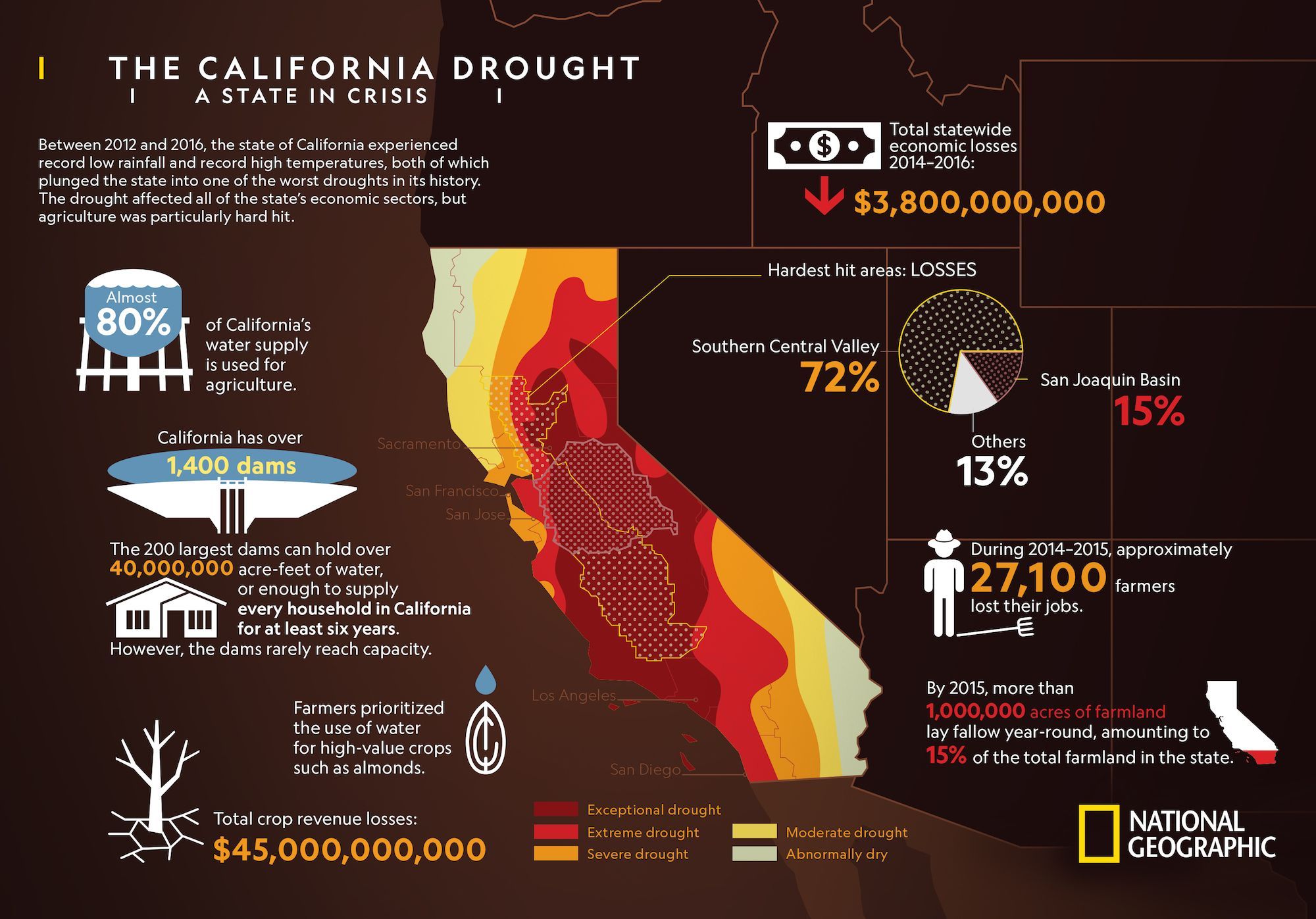

Also getting worse is the drought in California as snowpack this year is at 39% of average and that's the wost level in 1,200 years – so pretty bad. According to Dr. Schwartz, who wrote the report:

Also getting worse is the drought in California as snowpack this year is at 39% of average and that's the wost level in 1,200 years – so pretty bad. According to Dr. Schwartz, who wrote the report:

"Many people have a rather simplistic view of drought as a lack of rain and snow. That’s accurate — to an extent. What it doesn’t account for is human activity and climate change that are now dramatically affecting the available water and its management.

Droughts may last for several years or even over a decade with varying degrees of severity. During these types of extended droughts, soil can become so dry that it soaks up all new water, which reduces runoff to streams and reservoirs. Soil can also become so dry that the surface becomes hard and repels water, which can cause rainwater to pour off the land quickly and cause flooding. This means we no longer can rely on relatively short periods of rain or snow to completely relieve drought conditions the way we did with past droughts."

Even with normal or above-average precipitation years, changes to the land surface present another complication. Massive wildfires, such as those that we’ve seen in the Sierra Nevada and Rocky Mountains in recent years, cause distinct changes in the way that snow melts and that water, including rain, runs off the landscape. The loss of forest canopy from fires can result in greater wind speeds and temperatures, which increase evaporation and decrease the amount of snow water reaching reservoirs.

We are looking down the barrel of a loaded gun with our water resources in the West. Rather than investing in body armor, we’ve been hoping that the trigger won’t be pulled. The current water monitoring and modeling strategies aren’t sufficient to support the increasing number of people that need water.

This is the kind of stuff that should be affecting your long-range real estate planning. Of course, the same kinds of climate catastrophes will spread all over our country and the rest of the World in the not-too-distant future but this is happening now – a preview of things to come elsewhere. The food shortages, unfortunately, will be felt nationally and it will happen this year as more and more of California's crop land goes off-line.

There was a great article in the NYTimes about one company's adventures in global shipping that gives us a good idea of what a mess everything is. These are the kinds of things we'll be listening for as the Earnings Reports start pouring in next week but, until then – enjoy a quiet week.