{kind=link}

We WANT to be optimistic, don't we?

I mean investors are a generally optimistic group – we are betting on things being better in the future than they are today – it's kind of our underlying investing thesis that causes us to be investors in the first place. What separates us from the average luxury bunker buyer is that we feel obstacles can be overcome and conflicts will be resolved and our innate ingenuity will solve almost any problem.

For example, Eli Lilly is up today on nice results and, unfortunately, an 81% increase in sales of their Covid treatment and Trulicity (diabetes) sales are up 20% as we all sat on our asses for 2 years but Kudos to LLY for coming up with a better solution and that's Tirzeatide, which just finished a large-scale study showing an amazing 22.5% (not a typo) average weight loss for people who combined the drug with a healthy diet and exercise.

LLY is not cheap at $271Bn with $8Bn in earnings and $13Bn in debt but MRNA sure is at $57Bn with $10Bn in earnings and $10Bn in CASH!!! Expectation are the Covid shots will wind down but Covid wasn't why they started the company – it simply proved the value of what they can accomplish. Don't worry Moderna investors, there will be other horrible diseases we need vaccines for – and now they will have about $20Bn in CASH!!! going forward to fund R&D with.

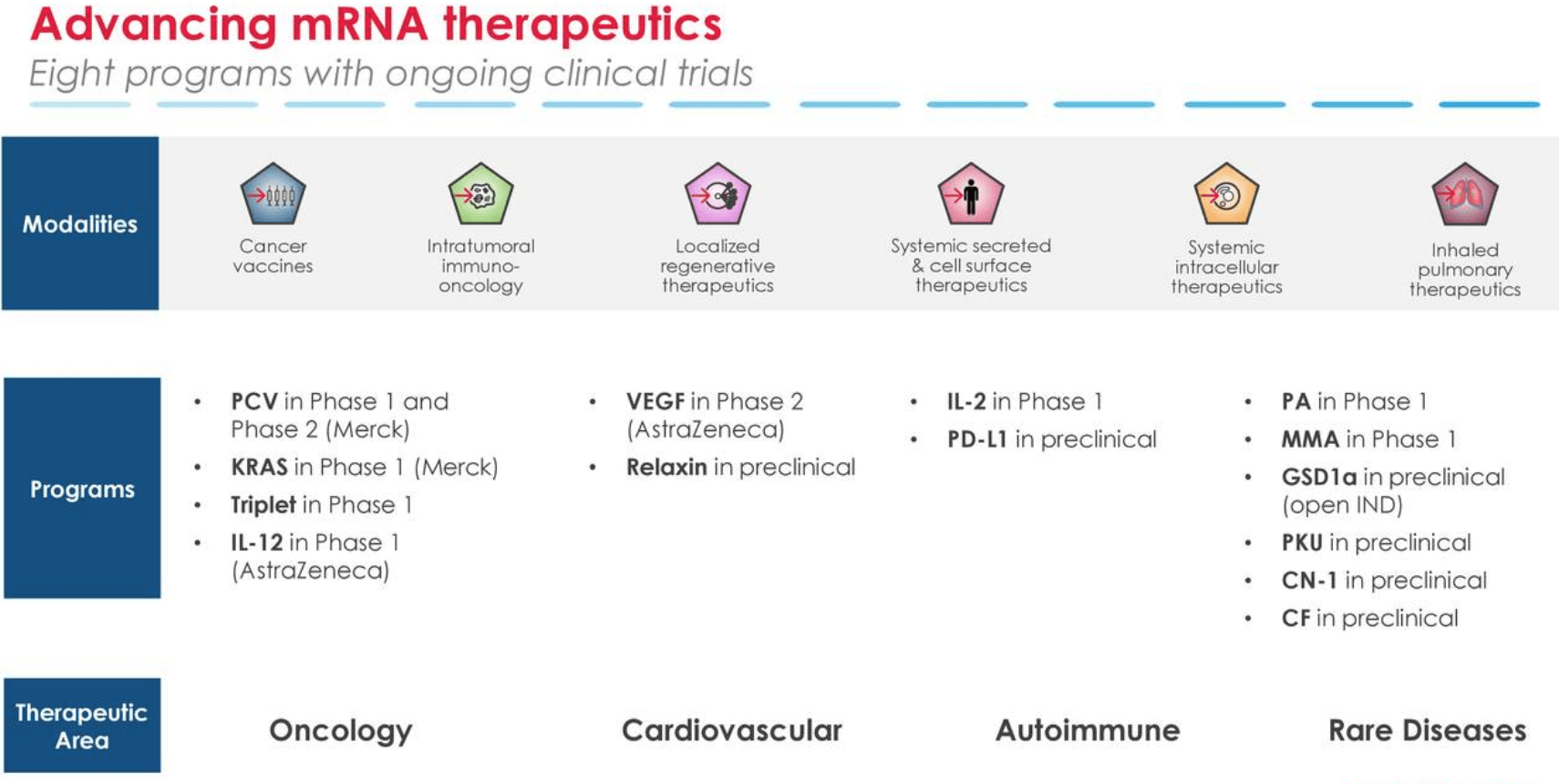

LLY expects to make $7.5Bn with their weight-loss pills but MRNA can come up with a vaccine so you don't gain the weight in the first place. That's not where Moderna's focus is, however, their current pipeline looks like this:

We'll hear more about it on their May 4th Conference Call but these were the original goals for the company – Covid was just a bonus that proved their methodology could lead to workable vaccines – why abandon them now? Traders (not investors) are certainly feeling the pressure as the stock is 66.6% off it's highs but that's a sign to invest, not divest.

All Biotechs are taking a beating this quarter and yesterday, in our Live Trading Webinar, we were discussing putting more eggs in fewer baskets and MRNA is still our favorite (not counting PFE) but we have a severe loss in our Long-Term Portfolio on that spread:

| MRNA Short Put | 2024 19-JAN 200.00 PUT [MRNA @ $142.43 $-3.36] | -5 | 10/5/2021 | (631) | $-12,500 | $25.00 | $54.18 | $-73.00 | $79.18 | $1.97 | $-27,088 | -216.7% | $-39,588 | ||

| MRNA Short Put | 2024 19-JAN 180.00 PUT [MRNA @ $142.43 $-3.36] | -10 | 1/13/2022 | (631) | $-40,150 | $40.15 | $23.75 | $63.90 | – | $-23,750 | -59.2% | $-63,900 | |||

| MRNA Long Call | 2024 19-JAN 150.00 CALL [MRNA @ $142.43 $-3.36] | 20 | 1/21/2022 | (631) | $120,000 | $60.00 | $-15.73 | $44.28 | $-0.73 | $-31,450 | -26.2% | $88,550 |

In context, of course, we promised to buy $280,000 worth of MRNA stock and we're down $82,288 though we did buy back the short calls with a net $24,000 gain so that's a net net $52,288 loss, which is only 20.8% of our commitment to $280,000 worth of the stock. Also, notice the stock is down 25% since January so we were better off with the options play than owning the stock. That's because our short puts were PROMISES to buy the stock if it got cheaper, rather than paying $200 at the time.

If we do intend to stick with MRNA for the long haul – it is beyond foolish not to improve the LTP position. Our 20 2024 $150 calls are $44.28 ($88,550) and the 2024 $130 calls are $52 and of course it makes sense to spend net $7.72 to push ourselves $12 in the money and gain $20 in strike. That will cost us $15,440 but we can offset that cost by selling 20 of the $200 calls for $30 ($60,000). Since that would put us +$44,560 and 20 more longs only cost $104,000 – why not sell 15 more of the 2024 $200 calls for $45,000 and buy 20 more of the 2024 $130s for $104,000 and then we will have spent net $14,440 to move from 20 long 2024 $150 calls to 40 of the 2024 $130 calls, covered with the $200s.

This is also good as a new trade, of course.

At $200, we would recover $280,000 and, since we have 5 open calls, we can sell 5-10 short-term calls, like the July $170s for $10, to pick up some extra income along the way. Selling 10 July calls for $10,000 would use 78 of the 631 days we have to sell and 5 extra short calls carry very little risk. Perhaps we could make $50,000 doing this consistently while we wait – but not yet – let's see how earnings go before selling short calls.

At $200, we would recover $280,000 and, since we have 5 open calls, we can sell 5-10 short-term calls, like the July $170s for $10, to pick up some extra income along the way. Selling 10 July calls for $10,000 would use 78 of the 631 days we have to sell and 5 extra short calls carry very little risk. Perhaps we could make $50,000 doing this consistently while we wait – but not yet – let's see how earnings go before selling short calls.

As to the short puts, $200 is still our target so we'll wait for earnings as we are in the puts at net $175 and net $140, which is where we are now, the rest of the loss is paper premiums, which shouldn't bother us as long as we REALLY want to own the stock – and we do! There are about $100,000 worth of short puts but the 2024 $150 puts are $45 so we could bump up to 20 of those at $90,000, paying $10,000 to drop to the lower strike and, as we collected $52,000 originally, we'd be in the 20 short puts at net $42,000 or $21 per put so our net entry would be $129 – even lower than we are now. And that's before we roll out to the 2025 puts, which should come out in July.

This is how we "fix" a trade but that only works if we were right about the long-term value of our stock and that remains to be seen but MRNA is one I am happy to take a chance on. Most of our other Biotechs we will be pulling the plug on in favor of this spread, which hopefully will get us our money back and more for the whole group.

This is how we "fix" a trade but that only works if we were right about the long-term value of our stock and that remains to be seen but MRNA is one I am happy to take a chance on. Most of our other Biotechs we will be pulling the plug on in favor of this spread, which hopefully will get us our money back and more for the whole group.

Not to get too optimistic but two other trade ideas we identified in yesterday's Live Trading Webinar were Boeing (BA) and Generac (GNRC) and we'll be setting up entries for them as well but only small ones as I'm more concerned with fixing our underperformers before we take on the burden of new trades.

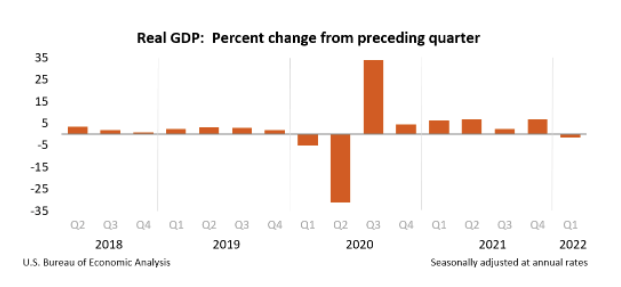

8:30 Update: As we expected, GDP was a huge miss, at NEGATIVE 1.4% vs +1.1% expected by our Leading Economorons. Ridiculously, the markets are taking it as a positive since it means the Fed is less likely to tighten but, if the GDP is falling and inflation is still rising (it is), then the Fed has no choice but to sheperd us into a recession.

Real Personal Income declined by 2% in Q1 after falling 5.4% in Q4 so it will take 3 quarters of record increases just to get consumers back to even by the end of the year – doubtful. Personal Savings also fell $180Bn – about 15% of our total savings. Let's take avantage of this "rally" to punch up our hedges yet again…