{kind=link}

By Louis Navellier. Originally published at ValueWalk.

For weekend reading, Gary Alexander, senior writer at Navellier & Associates, offers the following commentary:

“I would like to say to Milton … Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.” – Fed Governor Ben Bernanke, speaking to Milton Friedman on his 90th birthday, 2002.

Last week, I showed how the Federal Reserve Open Market Committee was very active during most mid-term election years from 1962 to 1998, often causing turbulence in the markets and a change in Congressional party power, thereby fueling a market rally late in the year. I showed how the S&P 500 gained an average 50% from its low point in a mid-term election year (like this one) to the high point of the following year.

Q1 2022 hedge fund letters, conferences and more

The Fed Learned Some Lessons

In the 21st century, the Fed seems to have learned some lessons by avoiding too much market intervention prior to elections – but the best news is that the market still took off strongly during the final quarter of most mid-term election years. Let me show you these recent examples, and then draw some tentative conclusions:

In 2002, the stock market emerged from two killer crashes resulting from the tech-stock bubble of 1999, first in 2000, and again in 2002. (The 9/11 crisis came in the middle of those two market purges.) This combined slow-motion crash took 30 months to reach bottom, falling almost 50%. The economy was not that bad in 2002, with low (1.6%) inflation and a +1.7% GDP with 6% unemployment, but Fed chair Alan Greenspan kept his powder dry during election season and only lowered rates 0.5% the day after the mid-term elections.

Then the market soared: In 2003, the S&P 500 closed the year at 1111.92, up 43% from its 2002 low.

In 2006, the new Fed Chair Ben Bernanke (serving from February 2006 to January 2014) also laid low during election season. With a healthy economy (+2.8% GDP, 3.2% inflation, and 4.4% unemployment), he raised rates four times in the first half of 2006, from January 31 to June 29, but he made no moves in the second half.

Then, an amazing thing happened. After the 2008 financial crisis, the Fed lowered short-term interest rates to effectively zero (a range of zero to 0.25%) for a full seven years, from December 16, 2008, to December 17, 2015 – virtually the first full seven of Barack Obama’s eight years in office, and in most of Ben Bernanke’s 8 years as Fed Chair, so there is nothing to report about the Fed’s actions during the 2010 mid-term elections.

In 2014, there is likewise nothing to report during the only year in which Janet Yellen (serving from February 2014 to February 2018) was Fed Chair during a mid-term election. Rates remained frozen at zero to 0.25%.

In 2018, Jerome Powell (serving from February 2018 to the present) made a blunder that impacted the elections and pushed the markets into a panic. During a quite healthy economic year (+2.9% GDP, unemployment at only 3.9%, and inflation at 2.4%), he raised rates four times – once too often, most said – during his rookie season. On the surface, this was his noble attempt to bring rates back to normal – a “normalization” process – but his third increase impacted the election, and his fourth increase tanked the stock market in December.

Powell first raised rates from 1.5% to 1.75% on March 22, then to 2.0% on June 14, and then to 2.25% barely a month before the election, on September 28, and then up to 2.50% just before Christmas, on December 20. As a result, the S&P declined almost 20% from late September to late December in a fourth-quarter swoon.

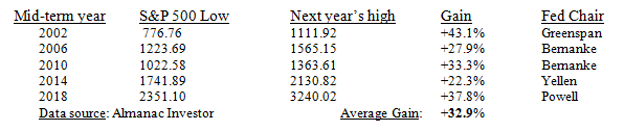

Here’s a continuation of last week’s table of market lows in mid-term election years vs. highs the next year:

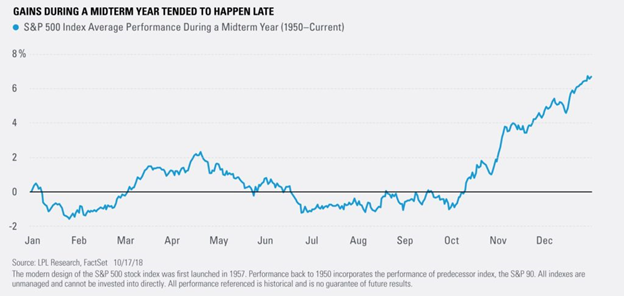

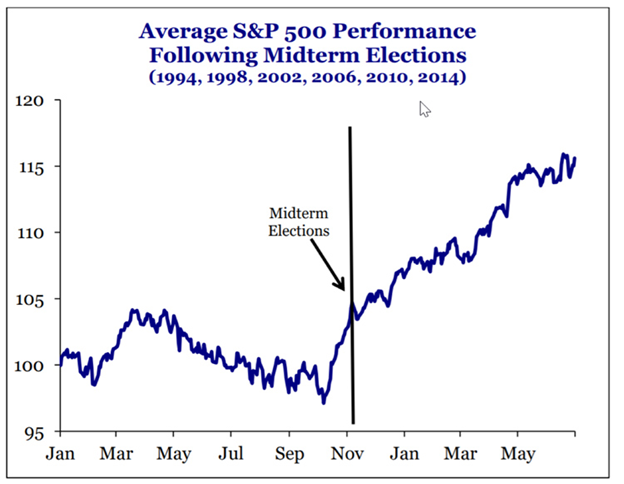

As I’ve shown before, the bulk of the full-year gains in mid-term election years (since 1950) tend to come in the fourth quarter alone, with the first half of the next year marking a continuation of that upward trend.

Powell torpedoed the 2018 fourth-quarter stock market by his September and December rate increases, so that made the 2018 fourth quarter an anomaly, so I’ve taken 2018 out of both charts – above and below:

Some Lessons for Investors (and the Fed) from This 2-Week, 60-Year Survey

Now, let me conclude with four quick and easy lessons that the Fed might learn from their successes and failures during their frequent flurry of mid-term election year interest rate increases over the last 60 years.

- Markets Overreact to Fed Rate Increases: There is no need to stage a market panic when the Fed raises rates. The Fed is merely following market trends after market rates rise. They are merely reflecting the actions of the bids and offers of millions of market actors in bond and currency markets in the real world. If you want to react to rising rates, react to the 10-year Treasury rate, not the Fed funds rate.

- The Fed Should Avoid Any Action After September 1 in Election Years. Since human beings are sheep, and we have been conditioned to think rate increases can topple kings and markets, Fed decision-makers should agree not to touch the magic interest rate button after Labor Day in even-numbered years.

Now, on to some more fundamental lessons:

- Group Think can be Dangerous. During 2021, virtually all Fed governors and leading economists were saying inflation was “transitory” and “manageable,” while I and most economists I respect were saying the opposite. The Fed has over 300 PhD economists, but they are nearly all Keynesian economists (or policy wonks) who denigrate “monetarism.” Treasury Secretary Janet Yellen is now doing her apology tour, but in March 2021, when the Biden administration was claiming that its $1.9 trillion stimulus plan would not fuel inflation, Ms. Yellen said the inflation risk was “small and manageable.” Yellen echoed Powell in calling any risk “transitory” and said that every economist she knew felt that way. That’s “group think,” by definition. Some blame Putin or Covid, but few cited “too much money.”

- Fine-tuning is a fool’s errand. In the 1960s, Presidential economic advisor Walter Heller developed the concept that central planners can “fine-tune” the economy to such perfection that they can prevent recessions, contain inflation, create jobs, fund both welfare and warfare (“guns and butter”), and create a virtual paradise (Great Society). How did that work out? A Vietnam quagmire, massive debts, and a decade of stagflation. Planners don’t have the power to create a Great Society or even a Pretty Good one. That’s up to citizens. Central bankers can be replaced by a computer, so just keep it simple, Geek Squad!

Updated on

Sign up for ValueWalk’s free newsletter here.