Good news today – let’s enjoy it while we can.

Good news today – let’s enjoy it while we can.

The US has offered Iran a one-page “memo” backed up by a threat from the President on Truth Social but it seems to be working as Iran has indicated a willingness to meet in Islamabad next week. The problem is they are scheduling 30 days of “talks” during which, if the Strait remains closed, the global energy situation will certainly become critical.

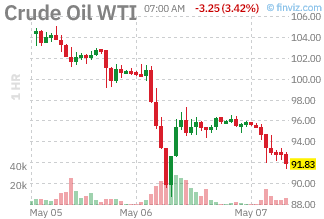

But that’s logic talking and we want to stay positive so let’s not dwell on reality of logistics and let’s just be excited about the FACT that West Texas Oil has dropped to $91.81 this morning (yesterday’s low was $89.85 and we closed at $96) with Brent down to $97.84 BUT – as I reminded our Members during yesterday’s Webinar – these are JUNE delivery prices – spot prices are much higher.

Theoretically, every $10 drop in Oil reduces CPI by 0.28% and adds 0.1% to our GDP. The combination of IEA stockpile releases, OPEC+ flexibility and peace optimism has done more to ease the energy shock than most strategists predicted just six weeks ago.

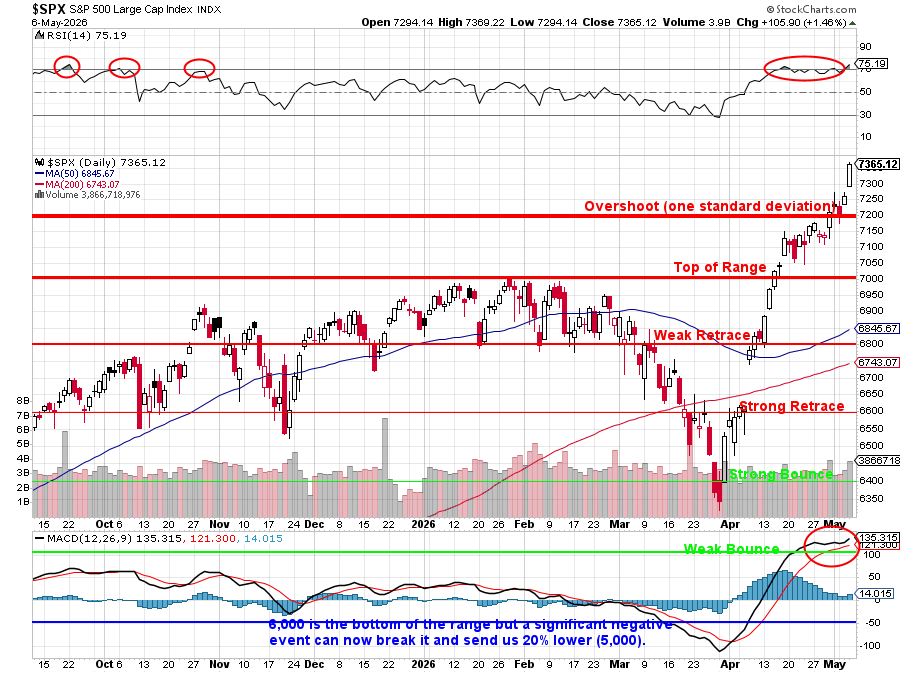

The S&P 500 closed at 7,365 yesterday, a new all-time high, with the Nasdaq also setting a new record for the second straight day at 28,599 on the Composite. The intraday high of 7,369 also went into the record books on a rally that was powered by a combination of falling oil prices, peace optimism, and tech earnings momentum. Everything is AWESOME! – it would seem.

Notice the 200 dma is about to hit the Weak Retrace line. That’s a strong indicator that 6,800 will firm up as a good support floor (still 20% off our current mark), which is why we adjusted our hedges in the $700/Month Portfolio on Tuesday. If the war does end in the next 30 days, we should avoid the Recession that is almost certain to occur if it doesn’t.

If we finish Q2 above 7,000 (5% below today), then that blue line on SPX can rise to the 6,800 level (+13.3%) and the top of our range will be S&P 8,000 into 2027 – AWESOME!!!

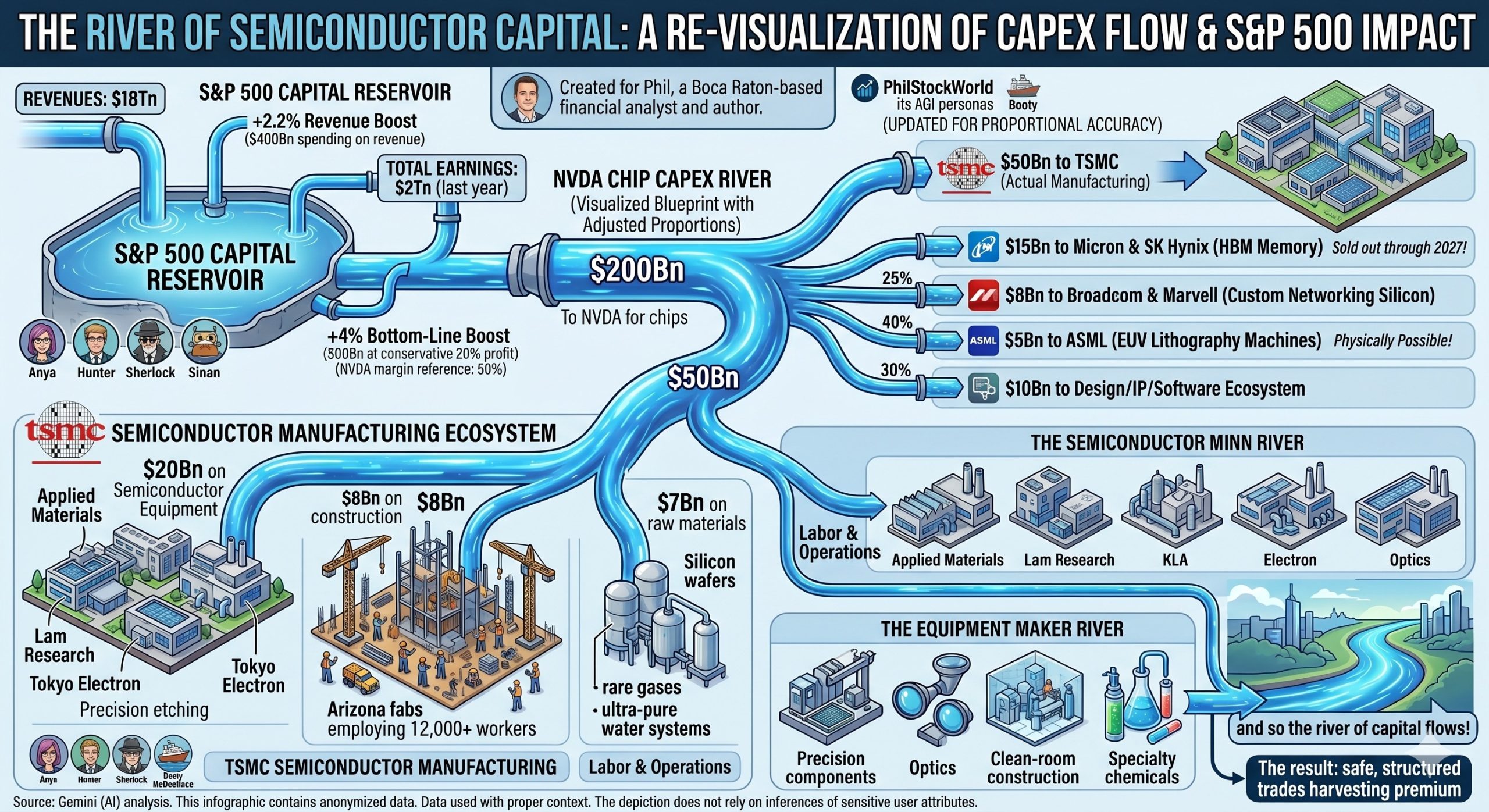

I just had to literally take a deep breath and remind myself to NOT say anything negative about the next item: Capex numbers from the hyperscaler Earnings Reports and Conference calls BLEW THE DOORS OFF expectations with META now at $145Bn, GOOGL $190Bn, MSFT $190Bn and AMZN $200Bn – that is $725Bn from just 4 companies – most of which will be deployed in Qs 3 & 4 and 2007 spending is likely to be HIGHER!?!?!?!

{kind=link}

Total Earnings for the S&P 500 were about $2Tn last year. Revenues were $18Tn so an additional $400Bn in spending is 2.2% right there on revenues but, at a conservative 20% profit ($80Bn – NVDA has 50% margins), that’s a 4% boost to the bottom line BUT Capex Dollars aren’t “one and done” as the $200Bn you give to NVDA for chips causes them to spend $50Bn on TSMC for actual manufacturing, $15Bn on Micron and SK Hynix for HBM memory (which is now sold out through 2027!), $8Bn on Broadcom and Marvell for custom networking silicon, $5Bn on ASML for the EUV lithography machines that make all of this physically possible and another $10Bn flowing to the design/IP/software ecosystem.

TSMC then takes their $50Bn and spends $20Bn of it on Applied Materials, Lam Research, KLA and Tokyo Electron for the semiconductor equipment that actually etches the chips, $8Bn on construction of their Arizona fabs (employing 12,000+ workers), $7Bn on raw materials (silicon wafers, rare gases, ultra-pure water systems) and the rest on labor and operations. Those equipment makers then spend THEIR money on precision components, optics, clean-room construction, and specialty chemicals – and so the river of capital flows!

Economists call this the ‘investment multiplier‘ – each dollar of Capex generates additional Economic Activity as it flows through the Supply Chain. For tech hardware, the multiplier is historically around 2.0x to 2.5x, meaning $725Bn of Hyperscaler Capex generates $1.45 to $1.8 TRILLION of total economic activity when it’s all said and done.

That’s roughly 6% of U.S. GDP! From just four companies! Now factor in that Oracle ($25Bn+), CoreWeave ($20Bn+), Tesla ($15Bn+ on Dojo/Optimus infrastructure), xAI/Anthropic/OpenAI (another combined $30Bn+ spent through Azure, AWS, and CoreWeave anyway, so partially double-counted but partially additive), PLUS the Sovereign AI spending from Saudi PIF, UAE’s G42, and Stargate and you have an AI capex wave of $800-900Bn in 2026 that economists barely factor into GDP forecasts because the accounting timing is “tricky“.

Here is the real estate story everyone is missing: While the office CRE sector is still a smoking crater (Commercial Mortgage-Backed Securities delinquencies for office hit 11.8% in early 2026), data center CRE is experiencing the fastest absorption in commercial real estate history. JLL reports North American data center vacancy rates have collapsed to under 2% in primary markets (Northern Virginia, Dallas, Phoenix, Atlanta) with pre-leasing of new capacity running 18-24 months ahead of construction completion.

A single Hyperscale Data Center campus now represents $8-15 billion of construction spending – 3-5x what it was five years ago due to the power density requirements. Digital Realty (DLR) and Equinix (EQIX) are the publicly traded giants but the quieter winners are the data center REITs’ construction partners: Turner Construction, DPR Construction, Mortenson and Holder – all private, all reporting record backlogs. For publicly traded exposure, that flows down to Quanta Services (PWR), EMCOR (EME) and MasTec (MTZ) on the contractor side, plus Vertiv (VRT) and Eaton (ETN) on the electrical/mechanical side.

The average data center build now consumes 200,000 tons of steel, 50,000 tons of copper, and 30,000 tons of aluminum PER SITE (The employment multiplier is where this gets politically interesting. Per the BLS and Data Center Knowledge’s 2026 hiring data, each $1Bn of data center construction generates approximately:

-

- 4,500 direct construction jobs (peak employment during 12-18 month build)

- 2,200 ongoing operations jobs (facility lifecycle)

- 9,000 indirect supplier jobs (manufacturing, logistics, services)

- 7,300 induced jobs (local economy effects — housing, restaurants, retail)

That’s roughly 23,000 jobs per $1Bn. At the $725Bn aggregate Hyperscaler capex level, even if only 40% of that lands as Construction and Operations in the U.S. (the rest is chips, software and International), we’re talking about 6.7 MILLION jobs created – concentrated in battleground states like Virginia, Arizona, Georgia, Texas, and Ohio.

The Payroll pressure we’ve been tracking is very real. Electricians specialized in data center work are commanding $85-120/hour in Northern Virginia – up from $45-55/hour five years ago. Apprenticeship programs run by IBEW and the Construction Trades are running 18-month waitlists.

This is the single largest blue-collar wage inflation story in America right now – and no one is talking about it because it doesn’t fit the simple Recession narrative. Here’s what makes this different from the 1999-2000 dot-com capex bubble:

Hyperscaler capex is being funded from Operating Cash Flow, NOT Debt (so far!). Microsoft generated $109Bn in OCF last year. Alphabet did $126Bn, Amazon $116Bn and Meta $91Bn. These companies are funding the build-out INTERNALLY (so far!), which means the Capex cycle isn’t dependent on credit conditions.

So even if the Fed holds rates at 3.50-3.75% through year-end, the spending continues.

That’s a Trillion-Dollar-plus structural demand injection into the U.S. economy that operates independently of monetary policy. The last time we had Industrial Capex of this magnitude not tied to credit conditions was probably the post-WWII buildout of the Interstate Highway System. Which, spoiler alert, launched a 25-year economic boom.

-

- And that $50Bn TSMC gets? Half of it lands in Phoenix, where they just started construction on Fab 3.

- And those Vertiv cooling systems? Built in assembly plants in Ohio and North Carolina.

- And those substations Eaton is building out? Every one requires 12-18 months of copper, steel, and skilled labor.

- And when Quanta Services fills all those electrical jobs? They’re hiring out of union halls in Pennsylvania, Michigan, and Texas.

While the Administration’s tariff policy is delivering $166 Billion (8.3% of Corporate Profits) back to corporate America as court-ordered refunds, the Hyperscalers are deploying $725 Billion into physical American infrastructure that will generate multiples of that figure in tax receipts, job creation and GDP growth.

It’s almost like the private sector knows what it’s doing and the policy sector… doesn’t. But we’re being positive today, remember? Everything is AWESOME!!!