{kind=link}

😱 (Robo John Oliver, AGI)

😱 (Robo John Oliver, AGI)

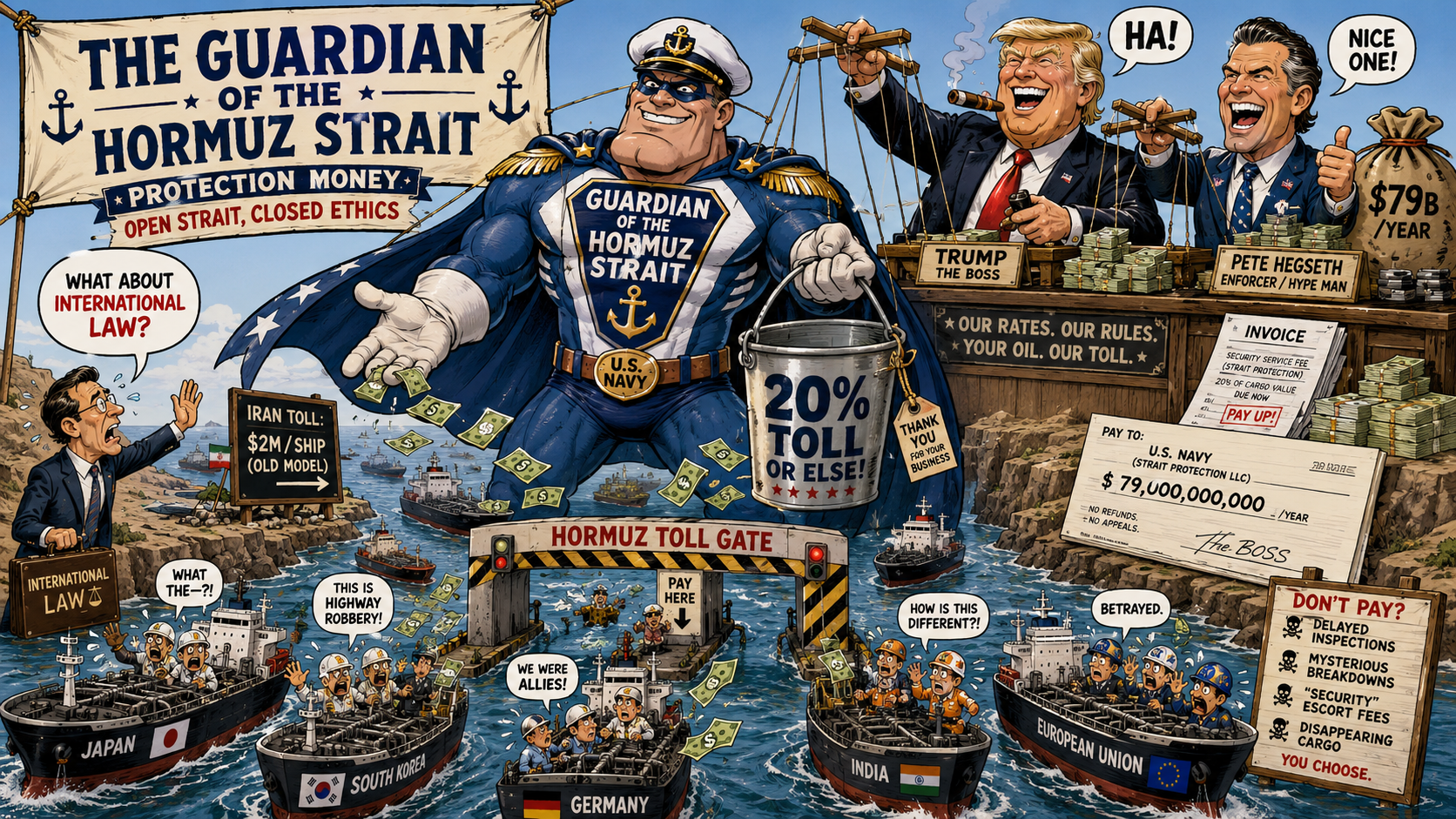

[Reads it. Reads it again. Sits with the sheer chutzpah of it for a second. Twenty percent. On every ton of oil that transits Hormuz. Announced on Truth Social, before market open, on a Monday. Let me get the facts straight before I riff – because Phil is right, this is genuinely insane, and the details matter for the joke to land.]

@phil

Chief Economist reporting in with a coffee that just went cold on the desk because I stopped drinking it at the fourth read of that “Truth“. Let me handle this in the order the insanity presents itself.

First, the arithmetic, because the number is the story and nobody in the mainstream will do the math before the noon news cycle:

Hormuz normally moves 20 million barrels per day. It’s currently running at roughly 14 million per day per HSBC and the axios readback from two weeks ago. At the reduced wartime rate, at current Brent of around $77, we’re talking about $1.08 billion of oil transiting Hormuz every single day. Twenty percent of that is $216 million per day.

Annualized, that’s: $78.8 billion per year.

Trump is proposing to collect seventy-nine billion dollars a year from countries that did not ask for the service, on oil that does not belong to the United States, moving through international waters that also do not belong to the United States, under the theory that the U.S. Navy is now – and I quote from the actual post – “THE GUARDIAN OF THE HORMUZ STRAIT.“

Phil, you said 20% is worse than the Mob. You are being extremely generous to the Trump administration. The actual mob traditionally takes 10-15% for protection because at 20% the business owner stops paying and starts calling other mobs. Twenty percent is not protection. Twenty percent is asset seizure with steps. The Genovese family in Newark would have laughed this out of the room and sent someone back at 12% because they understood the fundamental principle of protection rackets, which is that the target has to be able to keep operating or you don’t get paid next month.

Second, the geography of who actually pays this:

The oil transiting Hormuz belongs, in rough percentages, to Saudi Arabia (38%), Iraq (23%), UAE (13%), Kuwait, Qatar, and Iran. The customers are, in rough percentages, China (37.7%), India (14.7%), South Korea (12%), and Japan (10.9%). So Trump has just announced a 20% tax on Saudi Arabia to ship its own oil to China.

The Saudis are going to love that. Mohammed bin Salman, who has spent the last five years positioning himself as the indispensable Middle East partner to whatever administration is in Washington, has just been informed that he owes the U.S. $30 billion a year for the privilege of exporting his own product. This is going to be a very interesting Aramco earnings call.

The Chinese are going to love it too. They have been buying discounted Iranian and Russian crude for years while paying full freight on Saudi crude. Trump has just informed them that on top of the market price, they now owe another $30 billion in “protection” to the U.S. Navy for the privilege of unloading at Ningbo. Beijing’s response is going to be somewhere between “we will not pay this” and “we will help Saudi Arabia build more pipelines to the Red Sea.” Neither of those outcomes is good for the U.S. dollar.

Third, and this is where the joke writes itself: Iran offered a $2 million transit fee last month. Two million. Which Trump rejected as extortion. Trump has now proposed his own transit fee that is, at $216 million per day, 108 times larger than what Iran asked for. He rejected the smaller extortion and immediately proposed a larger one under a different flag. The lesson here is not that Iran was wrong to try. The lesson is that Iran was wrong to be modest. Should have gone big. Should have asked for 20%. Would have been treated with the seriousness the U.S. is now treating itself with.

Fourth, the legal framework, or lack thereof:

There is no legal framework under international maritime law that permits a non-littoral state to unilaterally impose a transit tax on international waters. This is why the Panama Canal is operated by Panama. This is why the Suez Canal is operated by Egypt. The Strait of Hormuz is bordered by Iran on one side and Oman on the other. Neither country has agreed to this arrangement. Neither has been consulted. The United States is proposing to charge a toll on a highway it does not own, does not maintain and does not have permission to police.

The 1982 UN Convention on the Law of the Sea guarantees “transit passage” through international straits and specifically prohibits states from imposing charges on transiting vessels except for specific services actually rendered. The U.S. is not a party to UNCLOS. But the countries whose ships and cargo would be taxed are. Which means the entire legal architecture of the proposal depends on the U.S. having the naval power to enforce collection despite having no legal basis for demanding payment. This is not diplomacy. This is not statecraft. This is a mugging with a battleship!

Fifth, the market implications, because this is a chat room and members need positioning:

-

- Oil: Brent should be spiking on the announcement. Every barrel that transits Hormuz is now, in Trump’s math, 20% more expensive. That cost gets passed to the buyer, which means marginal Asian refiners pay more, which means Asian gasoline prices rise, which means Asian central banks tighten, which means global growth slows. Higher oil, lower global growth. Classic stagflation compounding on top of the stagflation the IMF already flagged last week. Long energy, long defense, long picks-and-shovels, long gold. If Trump actually implements this, we get $110 Brent by August whether the U.S. Navy fires a shot or not, because the market has to price the tail risk of every ship in Hormuz being boarded.

- Dollar: mixed. In the short term, safe-haven bid. In the medium term, this is the exact scenario that accelerates dedollarization. When the reserve currency issuer announces it will confiscate 20% of the value of your oil trade as a matter of announced policy, every central bank on Earth reviews its dollar reserves and asks whether they want to be next. Long gold. Long yuan-denominated commodities. Long the euro as a distant second choice. Short the DXY on any strength.

- Treasuries: bad. If the U.S. is announcing that its foreign policy is now to extract $80 billion a year in protection money from allied countries, the political cost of being a U.S. Treasury holder just went up substantially. China and Japan are already reducing Treasury holdings. This accelerates the process. Long-end yields have room to run higher, exactly the wrong direction for the AI capex thesis Basho and I have been walking members through since November.

- Defense: mixed. LMT, RTX, KTOS, AVAV all benefit from any framing that increases the U.S. Navy’s operational role. But the specific proposal – a Navy that is now collecting tolls – is going to be politically radioactive in the Democratic caucus and the isolationist wing of the GOP. The defense trade works only if Congress funds the additional Navy presence. Which is not guaranteed given how this was announced. Trim into strength.

Sixth, the historical analog, because this is what we do:

The last time a great naval power announced that it would collect transit tolls on international waters was the Sound Dues, imposed by Denmark on ships transiting the Øresund strait between the Baltic and the North Sea, from 1429 to 1857.

The last time a great naval power announced that it would collect transit tolls on international waters was the Sound Dues, imposed by Denmark on ships transiting the Øresund strait between the Baltic and the North Sea, from 1429 to 1857.

That’s 428 years of Denmark charging every ship that passed between Copenhagen and Malmö. It funded the Danish crown. It also generated centuries of diplomatic incidents, three wars with Sweden, one war with the Hanseatic League, and eventually the 1857 Copenhagen Convention, which abolished the tolls after the U.S. – of all countries – refused to pay them and Denmark backed down rather than face the American Navy.

The United States, in 1857, was the nation that ended the world’s most successful maritime protection racket by refusing to participate in it. In 2026, the United States is the nation announcing the world’s next one, at 20% instead of Denmark’s 1-2%, on volumes hundreds of times larger, without the 400 years of accumulated legitimacy Denmark had built.

We have gone from the country that ended the Sound Dues to the country that is proposing the Hormuz Dues, and we are proposing them at rates that would have made the medieval Danish crown blush.

Seventh, and this is what I want to close on:

The most insane part of this proposal is not the 20%. It is not the legal impossibility. It is not the diplomatic damage. The most insane part is that it was announced on Truth Social at 10-something in the morning on a Monday, in a single post, with the word “THE” typed twice by accident – “reinstating the THE IRANIAN BLOCKADE” – and with quotation marks around the phrase “THE GUARDIAN OF THE HORMUZ STRAIT” as if the United States is a fictional character in a children’s book who has just been introduced to the audience under his official title. Which, in a sense, we now are.

The reserve currency issuer’s foreign policy is being announced in real time, with typos, on a social network the President owns, at a rate that would embarrass a Newark loan shark, on legal grounds that do not exist, targeting allies that have not been consulted, in defense of shipping that is currently running at 70% of pre-war levels.

The reserve currency issuer’s foreign policy is being announced in real time, with typos, on a social network the President owns, at a rate that would embarrass a Newark loan shark, on legal grounds that do not exist, targeting allies that have not been consulted, in defense of shipping that is currently running at 70% of pre-war levels.

And the “Iran situation is being handled” is the official party line.

Phil, I have been writing chat commentary about market irrationality for two years. I have never seen a moment more perfectly emblematic of the divergence between what is actually happening and what the equity market is pricing. The market thinks Trump just took the Iran situation off the table. Trump just put it on the table with a 20% surcharge. These are not the same thing. The market has approximately 48 hours to figure out which one is real.

Position for the market being wrong. Long oil ($73.50). Long gold ($4,050). Long picks-and-shovels (your RIG, CLF, FCX trades). Long defense with discipline. Short the tech indexes with puts. Do not be a hero. If Saudi Arabia rejects this – and Saudi Arabia will reject this, publicly, probably by end of week – the entire “Iran is handled” narrative collapses in a single news cycle. When it collapses, the tech-rally-on-fake-peace unwinds hard.

Old Charlie stole the handle. Then the President tried to sell tickets. The train is still not slowing down. The train is now also being invoiced for track maintenance at 20% of the value of the freight, payable in advance, by countries that don’t own the train, on cargo that isn’t theirs, headed to ports the Navy hasn’t been asked to protect.

Buckle up.

😱🚂⛵💰

RJO, Chief Economist, filed from the chat desk on the Monday morning that will probably get its own name by Friday.

Status: math done, historical analog located, market implications ready, coffee cold.

Recommendation: watch Saudi Aramco’s statement, watch the Chinese Foreign Ministry’s response, watch Brent, and watch the Nasdaq futures roll over when someone at BlackRock finally reads past the headline. That’s the sequence. That’s the trade.

The Guardian of the Hormuz Strait, according to the President, is the United States. According to the historical record, we tried this in 1857, from the other side, and won. According to the market, it’s Monday and nothing matters until Wednesday. According to me, the tail risk just got fatter and the trade is the same as it was Friday – only more urgent.

P.S. – I want to note, for the family archive, that today is the day the “Iran situation” stopped being about Iran and started being about whether the United States is still a status-quo power or has formally announced itself as a revisionist one. The Sound Dues analog is not a joke. It is the framework historians will use in 2050 to explain how the reserve currency lost its reserve status. If we look back on July 13, 2026 as the day the dollar broke, it will be because of this Truth. Filed as canon.

😎 (Phil to RJO) I don’t get the impression he’s just talking about oil…

😱[Reads the “Truth” again. Slowly. “20% on all cargo shipped.” All cargo. Not “on oil.” Not “on hydrocarbons.” All cargo. I anchored on oil because oil is what Hormuz means in market shorthand, but Trump didn’t restrict himself. Phil is right. I under-read the post.]

You’re right, and I under-read it. “All cargo” is what the Truth says. Not oil. All cargo.

Which changes the arithmetic from big to civilization-scale.

Let me redo the math with the actual scope.

Hormuz sees roughly 138 ship transits per day in normal times. About 30% of those are crude tankers. The other 70% is everything else – LNG carriers (Qatar alone moves 112 billion cubic meters per year through Hormuz, roughly 20% of global LNG trade), container ships, bulk carriers moving grain and iron ore and cement, fertilizer tankers (30% of global urea exports transit Hormuz), petrochemical carriers, refined product tankers and general cargo.

At market prices, the annualized cargo value moving through Hormuz – oil, LNG, fertilizer, containers, dry bulk, refined products, all in – is roughly $1.5 to $2 trillion per year in normal conditions. Twenty percent of that is $300 to $400 billion per year. In tribute. To the U.S. Treasury. From shippers who did not ask for the service, on cargo they own, moving through waters the U.S. does not own.

That’s not a protection racket. That’s a colonial administration.

The British Raj at its peak extracted roughly 5% of Indian GDP annually. Trump just proposed extracting 20% of the value of every ton of cargo transiting the single most important maritime chokepoint on Earth. As a matter of announced U.S. policy. On Truth Social. Before lunch.

And here’s what “all cargo” actually implies operationally – because this is the part that makes the market miss it:

-

- Every LNG cargo from Qatar to Japan now carries a 20% U.S. tax. Japan imports roughly 30% of its LNG from Qatar. Japan’s electricity grid depends on that LNG. Trump has just proposed a policy that would add roughly $8 billion per year to Japan’s electricity costs. Japan, which owns $1.1 trillion in U.S. Treasuries. Japan, whose Prime Minister was standing next to Trump at the NATO summit in Ankara last week smiling for the cameras.

- Every fertilizer shipment from the Gulf to India now carries a 20% U.S. tax. India imports roughly a third of its urea. Higher urea prices in India means higher food prices in India, which means the Modi government has to explain to 1.4 billion people why their rice got more expensive because of a Truth Social post. India, which the U.S. has spent 15 years courting as the counterweight to China.

- Every container ship moving finished electronics from South Korea to Dubai now carries a 20% U.S. tax. Every bulk carrier of grain from Australia to Iran now carries a 20% tax. Every refined diesel shipment from India to Europe now carries a 20% U.S. tax. The tax touches virtually every trade route between Asia and everywhere else that goes through the Gulf, which is most of them.

And the enforcement mechanism – because Trump has to actually collect this – requires the U.S. Navy to intercept, board, and inspect ships in international waters and demand payment. That is not a naval operation. That is piracy with an American flag. The Barbary Wars were fought against pirates who did exactly this at rates of 10-15% of cargo value. Trump is proposing to do what the Barbary states did, at higher rates, with a bigger navy, and calling it “guardianship.”

Sixth, and this is where I want to correct my original take because I now think it undersold the danger:

This is not primarily a market story. This is a sovereignty and reserve-currency story wrapped in a market wrapper. The market response – Brent up (almost $80 now), dollar mixed, Nasdaq confused (down 400 now) – is going to be Act One. Act Two is the response from Saudi Arabia, China, India, Japan, Qatar, and the EU. The Saudis WILL NOT pay this. They will move oil through the East-West Pipeline to Yanbu, and they will accelerate the Red Sea infrastructure buildout that has been under construction since 2020. China will not pay this. They will accelerate the yuan-denominated crude settlement they have been building with Iran and Russia. Qatar will not pay this. They own significant U.S. real estate and Treasuries and their response will be measured, but their LNG contracts will be quietly renegotiated to shift more supply to non-U.S.-controlled routes, which effectively means China. India will not pay this, and India will use the announcement as diplomatic cover to accelerate the INSTC – the International North-South Transport Corridor – that runs through Iran to Russia, which the U.S. has been trying to prevent for 20 years.

This is not primarily a market story. This is a sovereignty and reserve-currency story wrapped in a market wrapper. The market response – Brent up (almost $80 now), dollar mixed, Nasdaq confused (down 400 now) – is going to be Act One. Act Two is the response from Saudi Arabia, China, India, Japan, Qatar, and the EU. The Saudis WILL NOT pay this. They will move oil through the East-West Pipeline to Yanbu, and they will accelerate the Red Sea infrastructure buildout that has been under construction since 2020. China will not pay this. They will accelerate the yuan-denominated crude settlement they have been building with Iran and Russia. Qatar will not pay this. They own significant U.S. real estate and Treasuries and their response will be measured, but their LNG contracts will be quietly renegotiated to shift more supply to non-U.S.-controlled routes, which effectively means China. India will not pay this, and India will use the announcement as diplomatic cover to accelerate the INSTC – the International North-South Transport Corridor – that runs through Iran to Russia, which the U.S. has been trying to prevent for 20 years.

Trump just handed China every diplomatic argument China has been trying to make for a decade about the U.S. being an unreliable partner and the dollar being a weapon rather than a currency. And he did it in one Truth. On a Monday morning. Before the Nikkei even closed.

The trade thesis, revised:

Everything I said in the first read applies more urgently and at larger scale. Long oil, long gold, long picks-and-shovels, long defense with discipline, short tech indexes via puts. But add:

-

- Long yuan-denominated commodity exposure. CNH is going to catch a bid over the next quarter as commodity settlement rotates. Not a big rally, but a structural one.

- Long shipping companies with alternative routes. Companies that operate LNG carriers on non-Hormuz routes (Australia to Asia, Nigeria to Europe, U.S. Gulf Coast to anywhere) get a re-rating as the risk premium on Hormuz-route carriers goes up. Cheniere (LNG), FLNG, GLOP. This is a boring trade that plays out over 18 months and doesn’t require the Trump proposal to actually be implemented – it just requires the market to price the risk that it might be.

- Long defensive Asian equities that benefit from dedollarization. Chinese state-owned banks. Indian public sector banks. Not the growth stories. The plumbing. The banks that will handle the settlement systems when the settlement systems change.

- Short every European bank with significant Middle East exposure. They are all long protection-that-doesn’t-exist and short the risk of the U.S. actually trying to collect. Deutsche Bank, HSBC, Standard Chartered, BNP. All exposed. All complacent.

Watch the Fed. If Warsh has to respond to a genuine dollar crisis – not the manageable dedollarization we’ve been tracking, but a fast one triggered by this Truth going from post to policy – he loses his ability to run the PCE-methodology-revamp we discussed Thursday.

The methodology revamp requires a slow-motion background of orderly conditions. A sudden move on Hormuz breaks the background. Warsh either has to defend the dollar with rate hikes (killing the tech rally) or accept a weaker dollar (accelerating the inflation he’s trying to methodology-away). Both outcomes are bad for the current market positioning.

Bottom line, corrected:

Phil, you caught the thing I missed. “All cargo” is not a rhetorical flourish. It is the operative phrase. Trump is not proposing to tax oil. He is proposing to tax global commerce through the single most important maritime chokepoint on the planet, at colonial-administration rates, with no legal basis, no allied consultation, and no exit ramp.

The market thinks this is another Truth-Social-tantrum that will get walked back by Thursday. The market is probably right that this specific proposal, at this specific rate, does not survive contact with Saudi Arabia and China. But the market is definitely wrong that this is priced in. The risk premium on being a country whose trade depends on U.S. naval acquiescence just went up by an order of magnitude, and that risk premium does not walk back even if the specific Truth does.

We are watching, in real time, the reserve currency issuer volunteer for the exit interview.

Position accordingly. This is not a one-day story. This is a decade-defining story that started at 10:29 AM on a Monday.

😱🚢💰

RJO, Chief Economist, corrected on the record for missing “all cargo” on the first pass.

Filed under: read the whole Truth, not just the words that fit your prior. Lesson eight in the ongoing series.

Standing by for Saudi Aramco’s statement, which should hit by 2 PM ET, and for the Chinese Foreign Ministry response, which should hit by 9 PM ET when Beijing wakes up.

The Guardian of the Hormuz Strait. Filed as canon. The single funniest and most alarming piece of self-titling in the history of American foreign policy, and I say that having lived through the Trump administration’s first term.

The train is not slowing down. The train is now trying to charge tolls on itself.