Another week another 100 points lower.

Yep, that's all it was, we lost all of 100 points more than last week, when we fell from 10,725 to 10,172 (553 points) and this week we dropped from Friday's Dow close of 10,172 all the way down to 10,067 yet you would think the world had come to an end to hear the media and the traders freaking out. I'm not going to try to explain it, I can't. Maybe it's because going into last week we were very bearish but, starting on the 22nd, we let ourselves finally get a little more bullish AND THE MARKET BETRAYED US!

How could the market not zoom right back up? It always zooms right back up, doesn't it? As I said a week ago Friday: "Boy, when sentiment shifts – it REALLY shifts!" My closing comment on Friday the 22nd was "Back to cash but leaving disaster hedges, which are looking great now as this is shaping up to be some disaster" and our weekend "Global Chart Review" showed us to be at some very key inflection points, letting us go well prepared into this week:

Manic Monday Market Movement

My Jets lost on Sunday so I was not in the best of moods on Monday. My outlook that morning was: "We still have our disaster hedges in case things get worse but, on the whole, we’re expecting a 1% bounce in the very least off our 5% lines (anything less will be a bad sign)." We were pretty much at the 5% rule on Friday's close so we focused on the bounce we wanted to achieve in order to get more bullish.

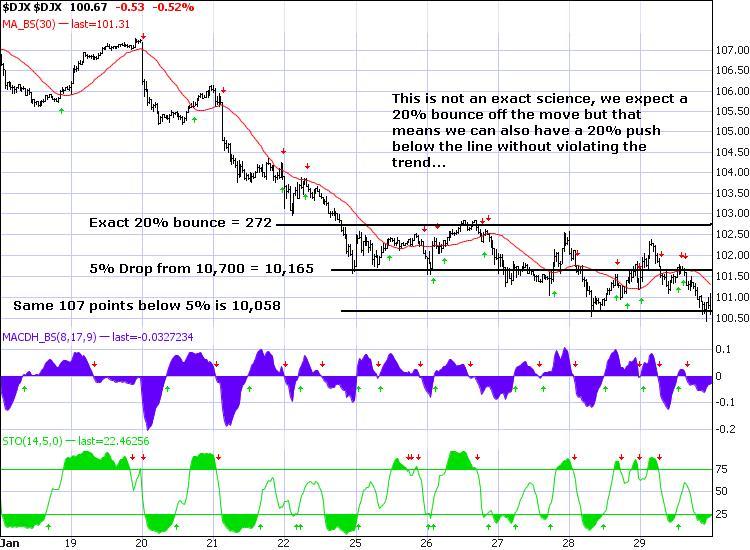

I noted that the levels we were looking for were not exactly 1% retraces (see post for reasons) and our target retraces were: Dow 10,300, S&P 1,105, Nasdaq 2,225, NYSE 7,100 and Russell 625. What were the highs for the week on those indexes? Dow 10,310 (+10), S&P 1,103 (-2), Nasdaq 2,227 (+2), NYSE 7,098 (-2) and Russell 621 (-4). So that's a net of +4 points out of 21,355 points worth of predictions on the retrace, accuracy to within .019% – not a bad showing for our patented 5% rule.

Please, under NO circumstances subscribe to our daily newsletter, where you would have this kind of information every morning and DO NOT get an Alert Membership where we send out our amazingly accurate watch levels to you every day. Having this sort of advanced information on the markets would be unfair to other traders, who thank you for your restraint…

See how I cleverly used reverse psychology there? I'm studying marketing techniques, we'll see if this one gets a good response… Anyway, back to Monday – I warned that things could get ugly and we could see a correction all the way down to 10% but we weren't really expecting anything further than that (Dow 9,650 is our downside target) and that meant it was a good time to consider some bottom fishing using our patented techniques described in "How to Buy Stocks for a 15-20% Discount." My comment was:

See how I cleverly used reverse psychology there? I'm studying marketing techniques, we'll see if this one gets a good response… Anyway, back to Monday – I warned that things could get ugly and we could see a correction all the way down to 10% but we weren't really expecting anything further than that (Dow 9,650 is our downside target) and that meant it was a good time to consider some bottom fishing using our patented techniques described in "How to Buy Stocks for a 15-20% Discount." My comment was:

The simple logic for our bargain hunting is this – if you regretted not buying stocks when the Dow was at 8,200 in July and we can scale into positions that break even on a 20% drop that protects us down to 8,200 – then why not take a chance on what may be the 2nd opportunity of a lifetime in 12 months? We also have over 300 earnings reports so non-stop fun but, for today, we will be seeing what happens and hoping we didn’t get too far ahead of ourselves in our early bottom fishing expedition last week.

I reminded Members that we expected an "amazing" GDP report on Friday and that led me to think we had a stick save coming by the week's end in the very least. In fact, I actually said at the time that we had a ton of economic data "all leading up to a highly inflated Q4 GDP Report (at least 5% now expected) as bullish inventory builds and rising commodity prices gave our economy quite the apparent boost. If it comes in well and the market flies – we’ll probably sell into it and flip bearish but let’s not get ahead of ourselves." – not a bad call 5 days in advance… Monday's trade ideas went as follows (adjustments, if any, in brackets):

- XOM March $65 puts sold for $1.65, now $2.75 – down 57% (all premium, no change)

- XOM 2012 $60 calls at $11.30, now $10 – down 12%

- AAPL 2011 $190/240 bull call spread at $20, now $17.60 – down 12%

- AAPL 2011 $150 puts sold for $10, now $11.50 – down 12% (pair trade)

- LVS 2012 $12.50/22.50 bull call spread at $3.50, still $3.50 – even

- LVS 2012 $12.50 puts sold for $3.50, still $3.50 – even (pair trade)'

- LVS March $19 puts sold for .63, now .37 – up 41% (pair trade)

- AAPL Apr $155 puts/Feb $180 puts for net .20 credit, out at $1 – up 500%

- AAPL July $185/March $200 net $17.50, now $17 – down 3% (can offer to roll July calls to $175 calls for $5)

It is very important to note that we are entering initial positions here and PLANNING to buy a second round when they are down 20% or more. It's very difficult to time the market perfectly so we scale into positions when we think we MIGHT be hitting a bottom but we generally stick with stocks we REALLY like A LOT and don't mind owning for YEARS in case we get a major downturn. As I said last week (and will keep saying) scaling into positions is ESSENTIAL in this kind of market (see "Stupid Option Tricks – The Salvage Play"). I set targets for Members on Monday evening, saying:

All I see here is a normal market correction (long overdue) as people finally catch up and realize the same stuff I’ve been talking about since November when we clearly moved into over-priced area (to the fundamentals). I’m not going to abandon them now and the fundies tell me that 9,650 is a fair bottom for the markets and we ran up from about 7,500 (I don’t count the spike down) to 10,700 (42%) and the 5% rule says a 10% correction or 12% since we overshot the top. 88% of 10,700 is 9,416 so that’s my bottom call even if we break down here and if we find any support higher than that, then I would consider it more bullish.

So we are buying here, using our classic "How to Buy Stocks for a 15-20% Discount Strategy" knowing full well they may fall another 10% or so. Why do we do this? Well, if we do recover quickly from here, we won't be missing a good buying opportunity and if we do drop, then taking a 20% (read the articles!) position on AAPL at net $185 and doubling to 40% if they drop 20% further to $150 for an average of $168 and then doubling down again if they drop another 20% to $135 puts us in an 80% full position of AAPL at an average of $152. If you don't REALLY want to own a full position of AAPL at $152 then DON'T buy it at $185. If you do REALLY want to own AAPL at $152 – the only way you're going to get your price is if it goes down. The trick is learning to enjoy the ride…

Tightening Tuesday – Global Edition

Tightening Tuesday – Global Edition

Finally China began taking some real steps to reign in the madness. As you can now see, it WAS fake Chinese demand driving commodities and look how fast that bubble has burst (but don't worry, I heard the speculators got right on the phone to Rent-A-Rebel and we can expect attacks in Nigeria this weekend to keep oil over $72.50). Europe was looking to cut back and even Obama gave us a preview of his SOTU proposal saying:

“We are going to have to be serious about the deficit in ways that we haven’t been before,” Obama said yesterday in an interview with ABC News. “We need a smarter government, not a bigger government, not a smaller government, we need a smarter government. And we don’t have one right now.”

Not even my most Republican friends can disagree with that one – no sir, we do not have a smart government right now and the last thing we need is a bigger, dumber government! Speaking of dumb governments, the S&P threatened to cut Japan's credit rating – and their population actually SAVES money! The Nikkei dropped 300 points from Tuesday's open for the week. I think I gave a clear enough warning in Tuesday's post when I said: "Fool me once, shame on you. Fool me twice and I’m a commodities speculator" but I also backed it up with a boatload of statistics and got flamed all over the web by the usual oil apologists who make it their mission to immediately stomp out any unfriendly mention of the giant scam that is the oil trade. Commodities led the rally lower this week and THAT's my favorite kind of market sell-off!

- VZ March $30 puts sold for $1.10, now $1.25 – down 14%

- VZ 2012 $30 puts sold for $5.40, now $5.80 – down 7.5%

- VZ at $30, now $29.42 – down 2% (waiting to cover with 2012 $30 calls at $5 but will cover with Apr $28 calls if they fall to $1.50)

- GOOG March $520/540 bull call spread at $12, now $11 – down 8% (roll to $510 calls for $6)

- GOOG March $510 puts sold for $12, still $12 – even (pair trade)

- BRK.B Sept $62/$70 bull call spread at $3.80, now $5.70 – up 50%

- GS Feb $150 puts sold for $4.10, now $5.85 – down 43% (no change yet)

- CME June $270/290 bull call spread at $12, now $11 – down 8%

- CME June $250 puts sold for $12., now $11.20 – up 7% (pair trade)

- AMAT July buy/write at net $10.85/11.43 – on track

- FTR Aug buy/write at net $6.22/6.86 – on track

- INTC artificial buy/write, (too complicated to to summarize) – down but fine

- MBI March buy/write at net $3.90/4.45 – on track

- TASR 2011 $2.50/5 bull call spread at $1.70, still $1.70 – even

- TASR 2011 $5 puts sold for .85, now .90 – down 6% (pair trade)

- XOM 2011 $55 calls at $12.85, now $11.40 – down 11% (we'd like to roll down to $50s for $3)

- XOM March $65 calls sold for $2.60, now $1.67 – up 35% (pair trade)

- FDX Apr $75 puts sold for $2.40, now $3.30 – down 38% (not a problem if you REALLY want them for net $72.60)

- T 2011 $30s at .53, now .56 – up 6%

- EDZ March $6 puts sold for $1.05, out at .85 – up 19%

- SDS March $32/36 bull call spread at $1.90, out at $2.60 – up 36%

At 1:36 in Member Chat, I also made the very timely call to get out of AAPL positions, scaling out using trailing stops. Just because we love AAPL (or any stock), doesn't mean we mindlessly ride out the moves down! Check out AAPL's chart and make sure you don't subscribe to our service because it is so much more exciting not knowing what's going on (see, that reverse psychology thing works great!).

That was a busy day! As we had been talking about how Keynesian stimulus policies had created false commodity bubbles that were driving an unhealthy misallocation of resources and I had been channeling my inner Hayek in the morning post, I thought it appropriate to further that discussion that evening in "Hayek vs. Keynes – An Economic Smackdown." The video is really good if you haven't had a chance to view it yet (at least to an economics geek like me!). As the markets dragged us lower during the week, I was looking at it as a sensible rotational move out of bubble stocks as the Global governments eased off on the stimulus pedal (but be careful not to mention politics when discussing the markets, as it makes people upset – better to ignore it so we don't ruffle and feathers, right?).

That was a busy day! As we had been talking about how Keynesian stimulus policies had created false commodity bubbles that were driving an unhealthy misallocation of resources and I had been channeling my inner Hayek in the morning post, I thought it appropriate to further that discussion that evening in "Hayek vs. Keynes – An Economic Smackdown." The video is really good if you haven't had a chance to view it yet (at least to an economics geek like me!). As the markets dragged us lower during the week, I was looking at it as a sensible rotational move out of bubble stocks as the Global governments eased off on the stimulus pedal (but be careful not to mention politics when discussing the markets, as it makes people upset – better to ignore it so we don't ruffle and feathers, right?).

Wednesday – Weakness or Consolidation?

See, there's an odd sort of flow to these thoughts from one post to the next, isn't there? As we expected to be testing the 5% line that day, we had to wonder what was next but the nature of the sell-off, driven by the commodity sectors (and SMH was one of our big hedges, of course) was just what we wanted to see in order to have a proper rally driven by companies that might actually HELP the economy instead of bleeding the consumers dry by overcharging them for gooey black liquids and shiny bits of metal. I made my case for loving a little consolidation for the week but the bulls were having none of it by Friday as they were getting very impatient for the rally that "always" comes. In fact I said at the open of Wednesday's post: "People have gotten so used to immediate rescues off any drop that holding a floor for two days brings out the doomsayers."

I pointed out that very rapid rise in ETFs has contributed to the bubbles we're seeing and that those same ETFs can easily be triggered into a frenzy of mindless, panic-selling – which is why I am thrilled with simply not going down as that, in itself, is a victory because things could be much, much worse. You can read my diatribe on ETFs that morning, where I also warned about the uptick in CDS's, which rose 14.2% on 54 governments since Ocober 9th. 14.2% more wagers on government defaults in 3 months – that IS something to be concerned about! Adding fuel to the bearish fire was our pal Nouriel Roubini and, daring to mention politics, I said that I thought Obama's spending freeze was a good sign, especially after looking at this:

But they couldn't get the freeze past the Senate, nor could they get the 60 votes needed to empower a balanced budget commission because, as I said on Wednesday: "Like Lot in Sodom and Gomorrah, we can’t find 60 righteous senators who want to get an honest assessment of this situation – perhaps because we all know what the answer is (cut spending, raise taxes) and now one has the guts to actually say it out loud." We were short from Tuesday's close but expected a big move at 2:15 – kind of like the one pictured HERE.

- GS March $145 puts sold for $5.85, now $6.35, down 10%

- RSX March $33/31 bear put spread at $1 out at $1.30 – up 30%

- RSX March $29 puts at $1.10, out at $1.10 – even

- GOOG artificial buy/write, too complicated to to summarize – down but fine

- AAPL $210 puts sold for $11.60, out at $7 – up 40%

- BRK.B March $66 puts sold for $1.50, now .85 – up 43%

- SYMC March buy/write at $16.37/17.18 – off target (waiting to see next week)

- PBT Sept buy/write at $10.25/12.63 – on target

- SLX March $59/56 bear put spread at $1.50, now $2 – up 33%

- T March $26 calls at .75, out at .95 – up 26%

- AAPL at $202 – now $192 – down 2.5%

- DIA Sept $97/104 bull call spread at $4, now $4.70 – down 10%

The IPad came out at 1:30 and the Fed came out at 2:15 and for no particular good reason the markets flew up into the close. We had a nice, strong-volume day where we didn't go down for a change and I liked that but, sadly, it didn't last. Pharmboy posted a great write-up that evening called "Orphan Drugs Are Good! BioMarin & Illumina" highlighting those picks.

Thrilling Thursday – Obama plus Jobs (Steve, not employment) Boost the Market

Our momentum off of Obama's SOTU Address lasted all of 5 minutes into Thursday's open before we went right off a cliff, quickly breaking our 5% levels. PIMCO was in charge of killing the market rally with Bill Gross releasing his very negative outlook that morning, which put the US, UK, Japan, Italy, Greece, France, Spain and Ireland in a "Ring of Fire" were unsustainable debt to GDP ratios will spell DOOM as we attempt to unwind. As we recovered on Friday morning, Gross' co-PIMP, Mohamed El-Erian said it might be a little soon to talk about "post-crisis" times, expecting instead a slow reset this year: "Too many markets, too many institutions have assumed this would happen quickly." Financial firms need to realize public policy risks and stay ready for a shaky regulatory environment, he told an FDIC conference. See how brilliant they are – Gross sets it up on Thursday and El-Erian drives it home on Friday and PIMCO's bonds gain Billions over the weekend – all in all, a good 2 day's work by Da Boyz.

We had a nice chart outlining the effect that the removal of stimulus might have on the global economy, George Soros joined me in calling gold a bubble and we were getting all kinds of mixed signals from Davos. I warned that if gold and the GDP both fell below 1,088 that is was a bearish signal that should not be ignored along with copper $3.20 and ALL of them failed on Thursday. By 9:38, I had already soured on the market, sending out an Alert to members saying: "Stopped out of DIA $103 calls already at $1.49 (10,200 was the stop line), maybe reload later but expect a sell-off from EU investors as well as quick bull profit taking (which we should be doing too!)."

- MOT July $7 puts sold for $1.10, now $1.32 – down 20%

- MOT 2012 $5 calls at $2.25, still $2.25 – even

- QQQQ $44s at $1.02, out at .90 – down 12%

- T 2012 $30s at $1.02, still $1.02 – even

- T March $26 calls sold for .68, now .58 – up 17% (pair trade)

- QQQQ $45 calls at avg .31, now .18 – down 42%

- DIA $104 calls at avg .60, out at .80 – up 33%

- AAPL March $185 puts sold for $4.75, now $7.25 – down 52% (waiting)

- AAPL 2011 $180 puts sold for $19, now $22.60 – down 19%

- QLD March $50 puts sold for $2.50, now $2.80 – down 12%

- AMZN Apr $110/Feb $120 put spread for .55 credit, now .95 – up 172%

- ABX March $34 puts sold for $1.80, now $1.90 – down 6%

- YRCW $1 puts sold for .50, still .50 – even (must get out ahead of meeting!)

- AMZN ratio backspread, too complicated to summarize – huge winner

- LVS June $13 puts sold for $1.25, now $1.30 – down 4%

- LVS 2011 $17.50s at $3.35, now $3.10 – down 6%

- LVS March $17.50s sold for .85, now .70 – up 18% (pair trade)

At 12:52 I went "VERY LONG," killing the disaster hedges and other unhedged bearish positions. As I said at the time: "May be a mistake but you have to gamble once in a while." As I said at 1:09 to Members: "Just the indexes QQQQs and DIA as directional bids (unhedged). I’m pretty determined to see it through to the GDP in the morning but if we don’t get a move up from Bernanke’s confirmation I’m going to probably give up as that would be one leg of my premise shot right there…" What a ride it has been since then already! As I warned at 2:59 into the close:

At 12:52 I went "VERY LONG," killing the disaster hedges and other unhedged bearish positions. As I said at the time: "May be a mistake but you have to gamble once in a while." As I said at 1:09 to Members: "Just the indexes QQQQs and DIA as directional bids (unhedged). I’m pretty determined to see it through to the GDP in the morning but if we don’t get a move up from Bernanke’s confirmation I’m going to probably give up as that would be one leg of my premise shot right there…" What a ride it has been since then already! As I warned at 2:59 into the close:

Yes, I like the Qs ($45s at .38 are good at the moment), this is the same "coiled spring" action we had last time they forced down the big Nas names and of course, MSFT and AMZN earnings tonight. It is still very risky – I’m playing a scenario that has nothing to do with fundies and everything to do with manipulation and sentiment so there’s nothing to fall back on if it fails – keep that in mind!

The problem with Friday's move up is the VIX dropped like a rock and we did not get good prices on our long index plays. With 3 weeks to go to expiration I elected to hang onto my longs and that still may be a mistake – we'll find out next week! It would have been far less stressful to follow through with the plan we had all week, which I reiterated in my comment to Members into Thursday's close at 3:53, saying: "Still a little bit bullish for some fun ahead of GDP (but probably selling into that excitement, if any)."

Thank GDP it's Friday!

Thank GDP it's Friday!

I definitely got too excited in the morning as things were going our way. Had I stuck to the original plan and gone short into the run-up on the over-hyped GDP numbers, we could have done much better. We had gained a nice 150 points from where we flipped bullish on Thursday and I was GREEDY for 10,300 which, of course, never came. I was expecting a much bigger move up than we got but there was a huge volume of selling that came in wave after wave all day, which was very disappointing as we were driven back to cash without really getting a benefit of that very nice run off the bottom.

As I had said in the morning post: "We’re not going to be too cynical but we will be getting back to cash (no unhedged positions) over the weekend because who knows what the pundit patrol will have to say over the weekend." As a junior member of that pundit patrol – I still haven't decided what I want to say and I'll be reading everyone else and attempting to form an opinion in time for it to be useful on Monday. Sadly on Friday, by 11:15 I had to warn Members: "Things are not looking too strong. Time to get out of the short-term plays unless you are willing to ride them out (I’m going to). Certainly if S&P blows 1,088 we need to give up until they get back over." Having stop levels set and taking them seriously does A LOT to keep you out of trouble.

- DIA $104 calls at .67, out at .82 – up 22%

- GOOG June $490/500 bull call spread at $7, now $6.50 – down 7%

- GOOG 2011 $470/570 bull call spread at $52, now $53.60 – up 3%

- GOOG March $590 calls sold for $5, now $3.65 – up 27% (pair trade)

- AAPL March $180 puts sold for $4.50, now $5.60 – down 24%

- AAPL 2012 $160s at $62, now $60 – down 3% (we want to roll down $10 for $5 any time)

- AAPL 2011 $200/230 bull call spread at $11, now $10.50 – down 4.5%

- AAPL March $165 puts sold for $1.80, now $2.33 – down 29%

- TBT March $46 puts sold for $1.10, still $1.10 – even

I must have said "cash" about a dozen times during Friday's Member Chat, to the point where it's now the joke we used to use for gold where I just say "Have I mentioned I like cash lately?" We hate to be in cash, we LIKE to trade but if we don't know what's going to happen next (or at least think we know) then cash keeps us flexible until we gain some clarity.

Meanwhile, what are we doing? Take a look back over the week's trading and you'll see we're selling puts at lower strikes into a higher VIX and hedging spreads that give us 10-20% downside cushions, not on speculative stocks, but on top-shelf listings like XOM, AAPL, GOOG, T, BRK.B, GS, CME, INTC, ABX… When the market is throwing a sale we don't go to the junk shelf, do we? If the market is crashing, then buy the stocks you expect to survive a nuclear war – that's a simple trading premise. Trading for the long haul doesn't mean a month or even a year, when you can get in cheap on a stock like XOM, it doesn't matter if it drops from $65 to $55 because we will own it for many years and make about $1.50 a month selling premium for a 15% annual return on our $65 no matter what the face value of the stock is. While we go for much higher returns with our quick trades and spreads, where our long-term retirement virtual portfolios are concerned – 15% a year is good money!

Also, when you are new to options trading it's very difficult to get over the sticker shock you get selling short puts and calls as they move against you. As you can see we sold a lot of AAPL puts but that's because we are THRILLED to own AAPL at $180 or less after seeing earnings and calculating what we feel the growth will be. We sold, for example, March $185 puts for $4.75 because we WANT to buy AAPL for a net price of $180.25. That was when AAPL was at $202 and AAPL is now at $192 and the March $185 puts are now $7.30 and those puts are down 54%. That sounds awful but the $7.30 is not only 100% premium but it's still $7 out of the money so AAPL has to drop almost 10% more just to get the guy who we sold the puts to even.

Meanwhile, we have "sticker shock" in our virtual portfolio with a 54% loss on that position but we didn't sell the puts because we were sure AAPL was going up (we would have bought calls!). Selling the puts gave us a healthy buffer and an entry to AAPL that was 11% cheaper than $202. If we are buying a first round at $180.25 and then we plan to double down 20% lower at $145 (probably by selling June $150 puts for $5 or more as AAPL falls) then we'd be scaled into round 2 of our AAPL purchases at an average of $162.50 with AAPL at $145 (down 10%) not really that bad considering we decided to buy AAPL at $202 is it?

Meanwhile, we have "sticker shock" in our virtual portfolio with a 54% loss on that position but we didn't sell the puts because we were sure AAPL was going up (we would have bought calls!). Selling the puts gave us a healthy buffer and an entry to AAPL that was 11% cheaper than $202. If we are buying a first round at $180.25 and then we plan to double down 20% lower at $145 (probably by selling June $150 puts for $5 or more as AAPL falls) then we'd be scaled into round 2 of our AAPL purchases at an average of $162.50 with AAPL at $145 (down 10%) not really that bad considering we decided to buy AAPL at $202 is it?

Had we bought the stock at $202 we'd be down $10 while the short puts are only down $2.55 so we're 75% better off already using the options for an entry so don't focus on the 54% paper loss on the puts – concentrate on the plan. Plan the trade, trade the plan and don't let fear and greed drive your trading. It happens to the best of us from time to time and, hopefully, we learn from our mistakes and do a little bit better the next time.

Also, keep in mind that, for a balanced virtual portfolio, we needed to pick up long positions as we cashed out our disaster hedges. We are now bullish without the downside protection, risking the wrath of the market over the weekend but there was pleny of cash to be put to work from our Disaster Plays, last updated with reiterated buys in the weekend post of Jan 10th (see, these things can be worth reading!) and we'll have a new batch ready for Members on Monday Morning, just in case. The old ones finished the week as follows (and we are out):

- SMN Apr $9 calls at .73 average, now $1.55 – up 112%

- DXD Apr $26/33 bull call spread at $2.20, now $3.95 – up 79%

- FAZ July $20/35 bull call spread at $1.60, now $3.30 – up 106%

- FAZ July $15 puts sold for $2.45, now $1.70 – up 31%

- SDS March $34/44 bull call spread at $1.40, now $3.35 – up 140%

So this is the week we took off that round of disaster hedges on the possiblity we find support and this is the week we take that money (over 20% cash to work with, if you hedged just 10% of the portflio originally) and add some long positions. Since we cashed out at the top, they weren't protecting much anyway and now we put that money back to work and we will certainly be adding bear plays next week if things head south but, hopefully, we got some good entries into some market consolidation and the economy isn't going to fall off a cliff. That would be nice – I'll let you know if I still believe it after I get some reading done.