Courtesy of Mish.

Fresh on the heels of my 3:38 AM post Charting Errors in BLS Participation Rate Projections came an interesting speech by William Dudley, president of the Federal Reserve Bank of New York.

Please consider these snips from Dudley’s speech today The Recovery and Monetary Policy.

My remarks will focus on the economic outlook. I do this with some trepidation, of course. In the private sector there are two adages about forecasting that underscore the need to be humble in this endeavor: First, forecast often. Second, specify a level or a time horizon, but never specify both, together.

The disappointing recovery

Turning to the first question, U.S. economic growth has been quite sluggish in recent years. For example, annualized real GDP (gross domestic product) growth has averaged only about 2.2 percent since the end of the recession in 2009. As a consequence, we have seen only modest improvement in the U.S. labor market.

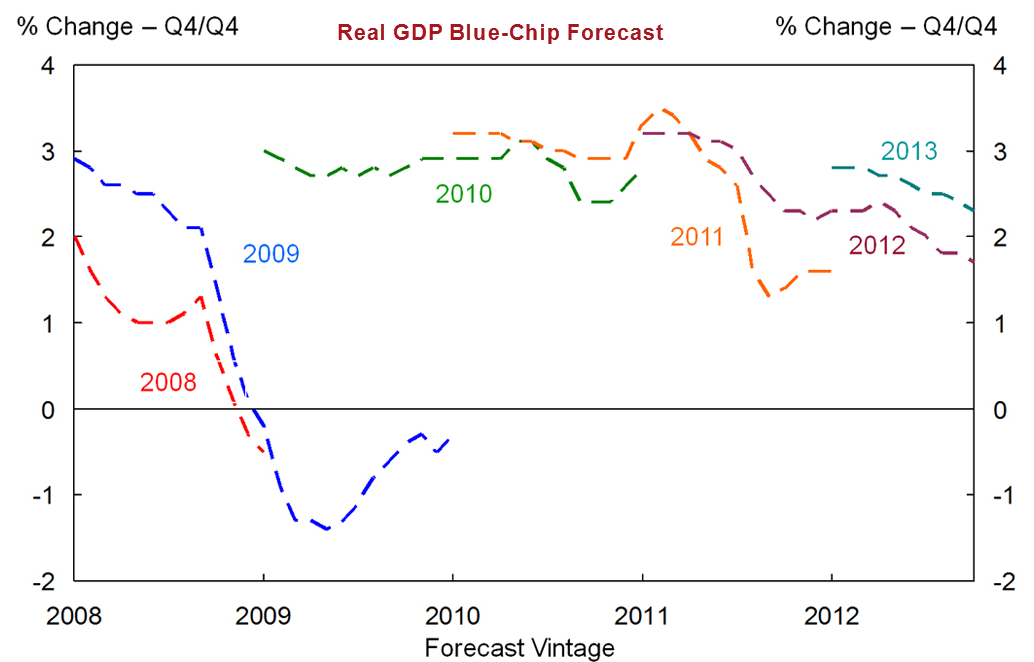

Not only has growth been slow, it has also been disappointing relative to the forecasters’ expectations. For example, the Blue Chip Consensus have been persistently too optimistic in recent years. This is illustrated in Exhibit 1 [following] which shows how private sector forecasts for 2008 through 2013 have evolved over time.

click on chart for sharper image

Two aspects of this exhibit are noteworthy. First, forecasters have consistently expected the U.S. economy to gather momentum over time. Second, with only one exception, the growth forecasts for each year have been revised downward over time, as the expected strengthening did not materialize.

Although I have focused on the private forecasting record here, the FOMC participants’ forecasts show a similar pattern. It is on the growth side where there have been chronic, systematic misses.

In my view, the primary reason for the poor performance of the U.S. economy over this period has been inadequate aggregate demand. There are several explanations for this. Although some were well-known earlier, others have only become more obvious as the recovery has unfolded.

During the credit boom, finance is available on easy terms and the economy builds up excesses in terms of leverage and risk-taking. When the bust arrives, credit availability drops sharply and financial deleveraging occurs. Wealth falls sharply, precautionary liquidity demands increase, desired leverage drops further. In the U.S. case, there were some idiosyncratic elements, such as subprime lending and collateralized debt obligations. But, in the end, the U.S. experience included the major elements of most booms: Too much leverage, too little understanding of risk, too easy credit terms, and then a very sharp reversal.

…

{kind=link}