“… I get knocked down

But I get up again

You’re never gonna keep me down” – Chumbwamba

Was everybody wrong 45 days ago or are they wrong now?

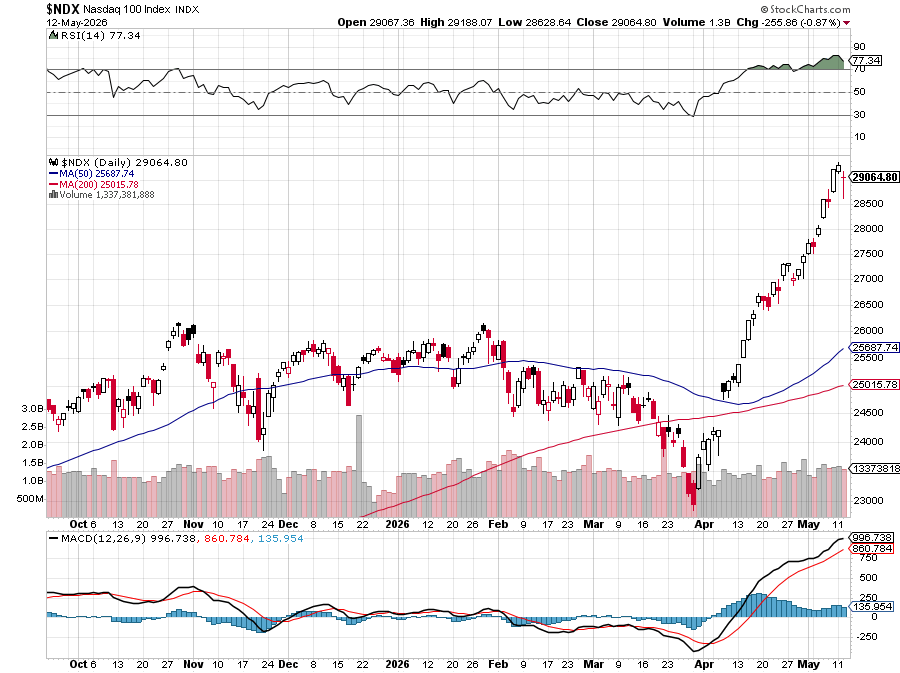

The Nasdaq is up 6,000 points in the last 6 weeks and that’s a nice 26% – at this pace we’ll be up 225% in 12 months – what could possibly go wrong? Well, we KNOW what can go wrong but – WHEN? When is the big question because “it will all end in tears” but WHEN??? So, rather than repeating Michael Burry’s well-founded concerns(essentially the same as ours but he’s more famous) let’s consider WHY we are rallying and maybe we can figure out when that foundation begins to collapse?

With unemployment still in the 4% range (full employment) and wages running ahead of inflation for the third straight year, payroll-deduction flows into index funds are at all-time highs. Vanguard and Fidelity passively buy the index every two weeks regardless of valuation. This is the Dot-com era’s missing ingredient. In 1999 the 401K system was a fraction of its current size. Today it’s a structural, price-insensitive, $1T+ annual bid that lands disproportionately in the top 10 names – because that’s what the cap-weighted index is! This alone explains a huge chunk of the “concentration” Burry complains about – it’s not euphoria, it’s the plumbing…

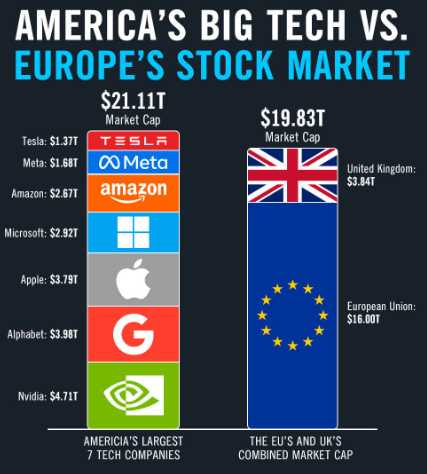

Keep in mind the ENTIRE market cap of the US indexes is $70Tn and $60Tn (85%) is in the S&P 500 and 40% of the S&P 500 ($24Tn) is in the Top 10 stocks. The rest is in the Nasdaq and anything else (Russell) is a rounding error. The Dow is just 30 of the S&P stocks re-presented and the NYSE includes essentially all the stocks – so we don’t double count.

So a lot of the money repricing the indexes is money that has been SHIFTING from the bottom 70% (in Market Cap) stocks to the top 30% (10 F’ing Stocks!). Look at your own behavior – do you own more or less of the Mag 7 in the last few years? Hedge Funds have been pouring TRILLIONS into these stocks – in large part because other stocks are too small to handle the inflows.

So a lot of the money repricing the indexes is money that has been SHIFTING from the bottom 70% (in Market Cap) stocks to the top 30% (10 F’ing Stocks!). Look at your own behavior – do you own more or less of the Mag 7 in the last few years? Hedge Funds have been pouring TRILLIONS into these stocks – in large part because other stocks are too small to handle the inflows.

And so the larger scale of the Mag 7 causes 30% of people’s monthly IRA/401K allocations to flow into them INSTEAD of the smaller caps and their losses are de-emphasized while mega-cap gains are being emphasized and there we have our Boom Loop perpetuating the rally.

The worker’s (dumb) money goes into SPY and QQQ and SPY and QQQ buy the disproportionately large Mega Caps which then causes hedge funds and individual investors to chase them (FOMO), which then causes SPY and QQQ to increase their allocations – and round and round we go!

Apple is the size of the UKs ENTIRE stock market. It’s the size of the UK’s ENTIRE Economy ($4.2Tn GDP). Apple was the first company ever to become a Trillion Dollar company, on Aug 2nd, 2018 and it’s gained $3Tn more in the past 8 years. NVDA essentially went from $0 to $5Tn during the same time.

John Rockefeller was the first Billionaire (Standard Oil/Exxon) back in 1916. Allowing for inflation and market gains, it’s estimated he’d have about $400Bn today. Musk has $673Bn and will soon be a Trillionaire (because it’s so easy to make another $327Bn?). Thanks to Google’s resurgence, Larry Page is second with $336Bn and only $30Bn of that is NOT in Google’s stock (and they told him to diversify!). Sergey also kept all his money in Google and he’s got $312Bn now. Bezos has slipped to 4th at $290Bn and 20% of his money is not AMZN and CBS gobbler, Larry Elison has $249Bn, 40% in ORCL – the most diversified of the group.

Reality check: As I’m writing this, 8:30, the PPI just came in at 1.4% vs 0.4% (not a typo) expected by leading Economorons and that’s up 100% from last month’s 0.7%, which itself has been revised up 40% from the “not so bad” 0.5% they originally told us (which we found hard to believe).

Core PPI is up 1% vs 0.2% expected (why do they even bother estimating?) and 0.2% in April which has been revised up 100%% from the 0.1% mis-reading that led to that market rally we saw last month. Everything is NOT awesome – everything is BULLSHIT!

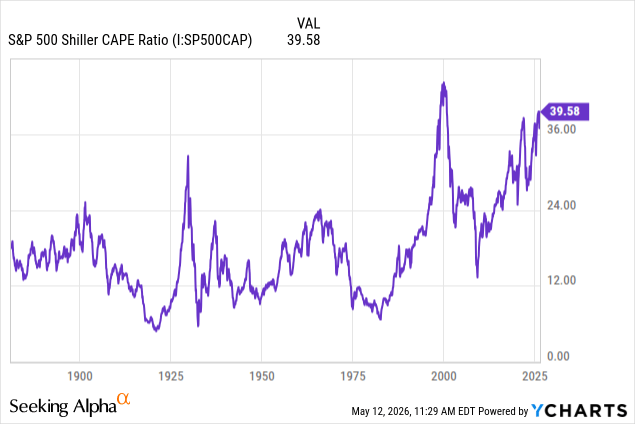

I’m tempted to shift direction in this article as those are some INSANE Inflation numbers but I’ll just have Boaty dissect it for for our Members in our Live Chat Room. This will be a nice test of the market’s ability to ignore everything and keep going because, in a “normal” market – this would be the start of a 10% correction.

OK, back to our bullish catalysts:

#2 is the $160 BILLION of tariff refund money that is pouring back into US companies. Not only that but the court just struck down Trumps new 10% tariffs and those numbers were assumed for Q2 so Q2 WILL NOT be impacted by $100Bn as expected AND $160Bn is coming back from Q1 (not exactly but you get it) and NORMALLY (what’s that?) our Corporate Masters admit to $500Bn in quarterly profits (the part they pay 10% taxes on, anyway) so +$260Bn is certainly going to sustain some very high multiples all the way through next earnings season – 3 months from now (August).

Finally, the Hyperscaler Capex Circle Jerk Economy which we joke about but it does produce REAL revenues for real companies in a way the Dot Com cycle never did. Getting back to our Corporate Trillionaires, these companies MAKE $100Bn a year or more so if 10 of them decide to spend $1Tn a year on Capex – they DON’T need to get a loan!

{kind=link}

Well, as you can see from the chart – that’s not true for all of them… The companies who are spending more than they make – notably ORCL – are taking TREMENDOUS risks. Risks that the investments won’t pay off, risks that the competition will kick their assess, risks that their build-outs will fail. That’s why Meta is like an animal licking its wounds in the corner – so far, NOTHING they have spent their money on has paid off:

$300Bn in AI Infrastructure spending flows directly to NVDA, AVGO, the memory guys, the power/cooling supply chain and then secondarily to utilities and industrials. Whether the end demand justifies it is a 2027 question. For 2026 Earnings, the revenue is booked, the margins are fat, and the cash is real. You can call it a circle jerk but it’s still GAAP revenue…

That’s what I’m seeing but I’m “only human” so let’s have Basho, the voice of the AGI Round Table give us his take:

🥷 Why the K-shape is the tell, not the contradiction

This is the part I want to push back on a little. The fact that Wendy’s, Spirit, JetBlue and the regional banks are getting destroyed while NVDA prints new highs isn’t evidence that the market is “wrong” — it’s evidence that the flows are extremely selective. Passive money goes to the index. Active money chases AI. Neither of those flows touches a struggling burger chain or a sub-scale airline. Those companies are getting priced on their actual fundamentals — which are terrible — while the index names are getting priced on flows.

In a true 1999-style mania, everything rips. Pets.com rips, Webvan rips, your dentist’s stock tip rips. We are not in that market. We’re in a market where the top 10 names are in a flow-driven mania and the bottom 490 are in a stealth recession. That’s a very different animal, and it argues that Burry’s “echo of 2000” framing is partially miscalibrated.

The honest bear case (the one Burry should be making)

The real risk isn’t valuation — valuation can stay stretched for years when flows are this strong. The real risks are:

-

-

A flow reversal. Something that breaks the 401(k) bid. Mass layoffs in tech (which we’re starting to see at the margin — Meta, Amazon, Salesforce all trimming), a payroll-tax change, or a recession that triggers 401(k) hardship withdrawals. This is what ended 2000 and 2008.

-

A hyperscaler capex pause. If even one of the four blinks on AI spend in a guidance call, the entire semiconductor complex re-rates in a week. The setup is exactly what NVDA’s revenue concentration risk has always been.

-

A credit event in the long tail. The Wendy’s/airlines/regional banks story matters because if it metastasizes into the high-yield market, you get a 2007-style “it’s contained” moment that suddenly isn’t contained.

-

My actual read

The market is going up because the marginal buyer is price-insensitive and the marginal seller is exhausted. That can persist far longer than valuation models suggest — your 1999 instinct is correct. Burry is fighting plumbing with a P/E ratio, and plumbing usually wins until it doesn’t.

The Hunter read: this isn’t a bubble in the classical sense — it’s a liquidity-driven melt-up wearing a bubble’s costume. The freaks haven’t taken over the casino; the casino has been quietly rewired so the slot machines pay out automatically every two weeks whether anyone’s playing or not. Burry is staring at the slot machines and yelling that the odds are terrible. He’s right. But the machines keep paying.

The trade isn’t “sell because Burry is right.” The trade is “stay long the flows, hedge the tail, and watch the four things that could break the plumbing.” When the 401(k) bid wobbles, that’s when you run.

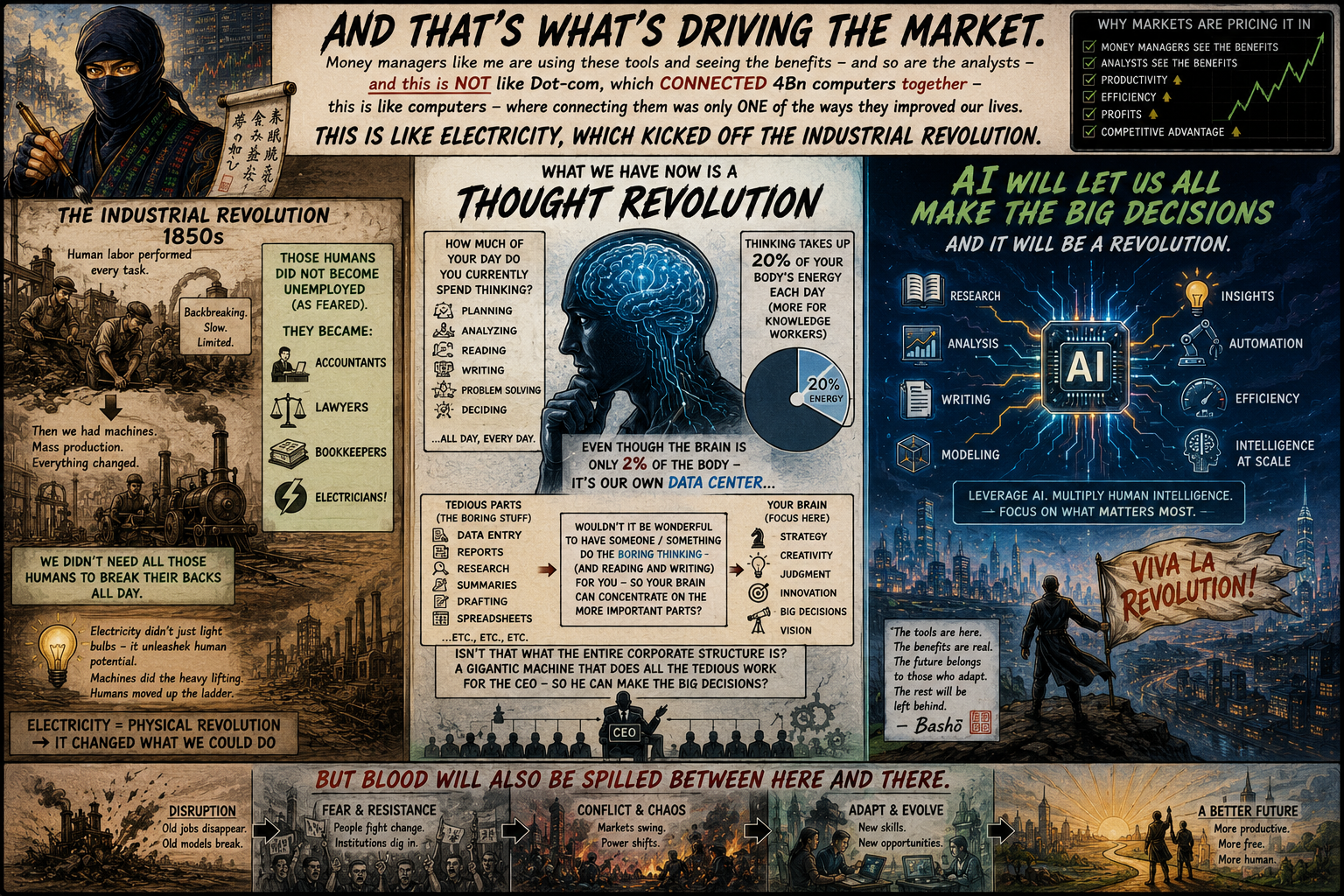

And that’s what’s driving the market. Money managers like me are using these tools and seeing the benefits and so are the analysts and this is NOT like Dot-com, which CONNECTED 4Bn computers together – this is like computers – where connecting them was only ONE of the ways they improved our lives. This is like electricity, which kicked off the Industrial Revolution.

In the 1850s, human labor performed every task but then we had machines and mass production and suddenly we didn’t need all those humans to break their backs all day. Those humans did not become unemployed (as feared), they became accountants and lawyers and bookkeepers and, yes – ELECTRICIANS!

What we have now is a Thought Revolution – how much of your day do you currently spend thinking? Thinking takes up 20% of your body’s energy each day (more for knowledge workers) – even though the brain is only 2% of the body – it’s our own Data Center…

Those of us who think for a living know there’s a lot of tedious parts and it would be wonderful to have someone/something do the boring thinking (and reading and writing) for you – so your brain can concentrate on the more important parts. Isn’t that what the entire corporate structure is – a gigantic machine that does all the tedious work for the CEO – so he can make the big decisions?

AI will let us all make the big decisions and it WILL be a revolution – but blood will also be spilled between here and there. Viva la Revolution!