{kind=link}

Why I Took Money out of My House

Courtesy of Michael Batnick

I can’t believe I’m saying this, but I’m never going to pay off my house. Let me explain.

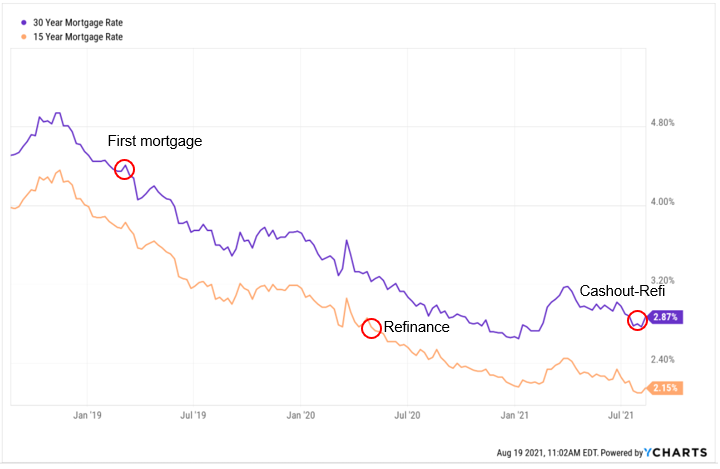

In April 2019, I took out a 30-year mortgage at 4.625%. At the time, I gave little consideration to how I would manage the mortgage. There was no strategy. I just figured I would make the monthly payment, and that would be that. And then the world went and got itself in a big damn hurry.

When interest rates plummeted in 2020, I switched from a 30-year mortgage to a 15-year. I couldn’t believe that I was borrowing money at 2.875%. My new payment would send three times as much principal to the bank. With a little money sprinkled on top of my minimum monthly payment, I could pay this thing off in 13 years. I was ecstatic with the idea that I could own my home outright by the time my kids go to college.

And then I changed my mind.

Not only did rates continue to drop, but they did so while the value of my house kept going higher. In just two years, my home appreciated by 25%. So I got the thinking. Why would I leave all that money sitting in my house earning nothing when I can do something productive with it? And if rates are so low, why wouldn’t I switch back to a 30-year mortgage and give myself more flexibility?

With so many moving parts, you really need to make sure you can get to the bottom line. Lucky for me, my financial planner, Bill Sweet. has a wicked mortgage calculator spreadsheet.

I switched from a 15-year mortgage at 2.875% to a 30-year at 3.375%.* I took a nice chunk of money out of my house and reduced my minimum monthly payment by one-third. I plan to continue with the same payment that I’m making right now but have the flexibility to lower it significantly if I choose to.

Bill plugged in my numbers to get a better idea of whether or not the numbers made sense. If I continue on my current trajectory, I will pay ~$750k in interest and principal over the next 12.5 years. If I continue to make the same payment on my new mortgage, I will extend my mortgage by 3 years and $172k in interest and principal. This is my hurdle.

By paying the same amount each month as before my refi, I will have to earn between 4.5 and 5% on the cash to come out ahead.

How am I going to do that? Honestly, I don’t know. I have a few options, but I don’t know what the future holds. One thing I can do with the money is put it to work in the event of another deep market selloff, should one come to pass. Another route I can go is investing in illiquid assets. Cliché, I know, but it’s nice to be able to take a flier on some of the businesses I believe in, like Quartr and Onramp, for example.

Okay so here’s the deal. My monthly payment goes down by 30%, and I get to take money out of my house. As long as I can make ~5%, then this was the right financial decision. The spreadsheet is important because you have to know whether or not something passes the sniff test. But there is more to this decision than dollars and cents. I’m confident that I will have more money in the future, so dollars today are more valuable to me. I also feel really good about having money in the bank. It gives me options, and it gives me peace of mind. All the other things I can quantify, but I value how I feel more than what the numbers say.

I want to be very clear that this is a risky strategy, and it’s not for everyone. For most people, their house is their largest asset. The forced savings mechanism of a mortgage is a wonderful thing. But I’m reasonably confident that I will come out financially ahead. And even if I don’t, I’ll be okay. I can take this risk because I’m conservative with my savings and investing.

I started this post by saying I’m never going to pay off my house. Allow me to contradict myself. I have no idea where rates will be in 5 years. I have no idea how I’ll feel in ten years. I might change my mind in the future, and if I do, I’ll be sure to let you know. But if you ask me right now, I think rates stay low for a long time and if that comes to pass, I can see myself doing this process again in 5-10 years.

*Cash-out rates are higher than for a traditional mortgage