{kind=link}

By Jacob Wolinsky. Originally published at ValueWalk.

Hidden Value Stocks issue for the fourth quarter ended December 31, 2021, featuring an interview with Lowell Capital Value Partners’ Jim Zimmerman and Abigail Zimmerman. Jim and Abigail discuss their stock idea, Computer Task Group, Inc. (NASDAQ:CTG).

Q3 2021 hedge fund letters, conferences and more

- See Part I here.

- See Part II here.

Stock Idea One: Computer Task Group (CTG)

Computer Task Group is an undervalued information technology (IT) services company in North America, South America, Western Europe, and India. It provides business process solutions, which include strategic advisory, data strategy, digital workplace, enterprise platforms, information disclosure, and regulatory and compliance services. The Company also provides IT and other staffing services, including managed staffing, staff augmentation, and volume staffing services. CTG serves the financial services, healthcare, manufacturing, and energy industries, as well as technology service providers.

CTG has gradually transformed itself from a staffing services company into an IT solutions company with higher margins and more stable performance. Adjusted EBITDA has increased from $9.5m in 2018 to $12.5m in 2019 and $15m in 2020. CTG performed well during the Covid-19 pandemic and its business showed strong resilience as work from home requirements drove increased demand for its technology services.

CEO Filip Gyde ran CTG’s European division successfully for many years and was made CEO in early 2019 and has pursued an aggressive program to exit lower margin staffing services and grow higher margin and more resilient solutions services since taking over. This is the same strategy Gyde executed in Europe for CTG which resulted in profitable growth for nine consecutive years. We believe Gyde has a laser-focus understanding of which specific solutions services are most critical to existing and potential customers and is carefully building a strong and resilient solutions business across all of CTG. Non- GAAP operating income and non-GAAP operating margins have consistently improved as IT Solutions continues to become a larger share of total revenues for CTG. CTG’s European operations currently provide a dominant share of total operating profits even though they are only about 40% of total revenues. This is due to Gyde’s strategy in Europe which has been executed for many years there. Further, CTG is under intense pressure to achieve continued improvements given an aggressive position held by an activist group, which made offers to purchase the company in mid-2019 and early 2020.

CTG’s long-term targets include IT solutions revenue of over $250m and adjusted EBITDA of $35m by 2023. While we are not convinced CTG can achieve these aggressive targets, we believe CTG will move aggressively towards them and, as a result, drive strong shareholder value. CTG has a highly cashgenerative business model with limited capital expenditure requirements and a “Ft. Knox” balance sheet with a net cash position of about $33m at Q1 of 2021, or about 20% of total market value.

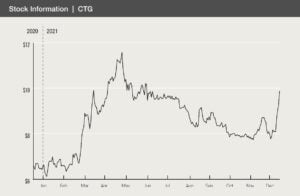

CTG’s shares currently trade at about $8 per share with about 15m shares outstanding for a market cap of $120m. CTG has a “Ft. Knox” balance sheet with net cash position of about $31m as of 9/30/21 for a total enterprise value (EV) of about $90m. LTM EBITDA is about $16m. LTM free cash flow (FCF) is about $10m. CTG is currently trading at about 6x adjusted EBITDA and a 10%+ unleveraged FCF yield.

CTG’s strategy is to grow its IT solutions business to $250m of revenue by 2023. As indicated below, IT Solutions is growing and becoming a larger part of CTG’s overall business, as CTG is concurrently exiting less profitable IT Staffing business. CTG owns or leases a total of 25 facilities throughout the world, including North America, Europe, South America, and India.

CTG has grown EBIT from $6m in 2017 to $11m in 2020. Adjusted EBITDA grew from $8m in 2017 to about $16m for LTM ended 3/31/21. We think adjusted EBITDA can grow significantly by 2023 to $25m or more via modest organic growth in revenues, improved margins due to increased emphasis on IT Solutions, and strategic, targeted acquisitions to add services and geographies required by customers. CTG has completed three small acquisitions recently, one each in 2018, 2019, and 2020, and these have helped to drive growth.

Sign up for ValueWalk’s free newsletter here.