{kind=link}

5% Mortgages are back.

5% Mortgages are back.

30-year notes have dipped from 190 in 2020 to 145 this morning and that's down 23.6% in two years – horrific losses for the long-term bond market but what sort of idiot was lending the Government money for 30 years at 1.25% anyway? Now it's 2.666% but this is just the start of the Fed's tightening cycle with another 2% (at least) to go in the next 8 months and already 30-year mortages are being priced over 5%, up from 3.5% in 2020, with lows all the way down at 2.5% briefly.

And look how fast rates have climbed in 2022 – this is why home-buying has ground to a halt. A $500,000 home with a $400,000 mortgage (assuming you have $100,000 to put down) cost you $1,686 a month at 3% in the Fall but now, in April, it's costing you $2,147 a month – an increase of $461/month (27.3%) in just one quarter. Even if you have a $100,000 job and just got a 10% raise, the take-home is only going to be +$6,000/yr to pay the extra $5,532 so you'd better hope nothing else went up in price or you'll have to cut back on other things.

Of course, once upon a time, we used to EXPECT 10% raises every year so we would stretch on a Mortgage because, after a few 10% raises, $2,147/month would seem like a fantastic bargain – especially if your home's value were also rising 10%, as the leverage you have on your home would make you a winner. That's how our parents were able to retire pretty comfortably but that Social Contract collapsed in 2008.

Of course, once upon a time, we used to EXPECT 10% raises every year so we would stretch on a Mortgage because, after a few 10% raises, $2,147/month would seem like a fantastic bargain – especially if your home's value were also rising 10%, as the leverage you have on your home would make you a winner. That's how our parents were able to retire pretty comfortably but that Social Contract collapsed in 2008.

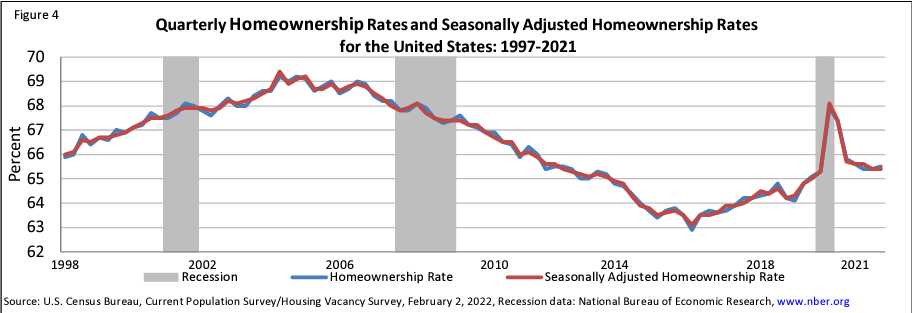

Close to 70% of the people in America owned homes in 2004 but that number has dropped to 65.5% now and that is putting upward pressure on the rental market, where prices have climbed 20% in the past 12 months. In large part, that's due to a surge of people losing their homes during Covid as ownership plunged from 68 to where we are now. You would think 5% is unaffordable but it's only sticker shock as we've gotten used to new rates. I bought a home in 1998 and was very happy with my 6.7% morgage at the time and my Dad bought a house in 1978 with an 8.8% mortgage and we were lucky to get it before the rates really started going up – to 11% in 1979, 15% in 1980 and topping out at 18% in 1981 but they were still 10% in 1987 (and the markets collapsed).

These things are all relative and you can learn to live with anything but it's an uncomfortable adjustment period, to say the least. We also had gas rationing in 1980 and prices were skyrocketing from 0.60 when I got my license in 1978 to $1.35 when I went to college in 1981 – that was shocking and they never went much below $1 again. Anyway, the point is we had inflation, rising gas prices, rising rates and the World did not end – even with Reagan and the Russians squaring off weekly.

Investors and consumers can indeed get used to anything. When I was a kid, my older brothers had draft cards – on any given weekend their "number would come up" and they could be shipped off to Vietnam to run around the jungles killing people and 2M people died over there, including over 60,000 US Troops and people were marching and protesting and talking about it all the time yet we just went through 2 years where 1M Americans died of Covid and look how used to that we got! The markets even rallied…

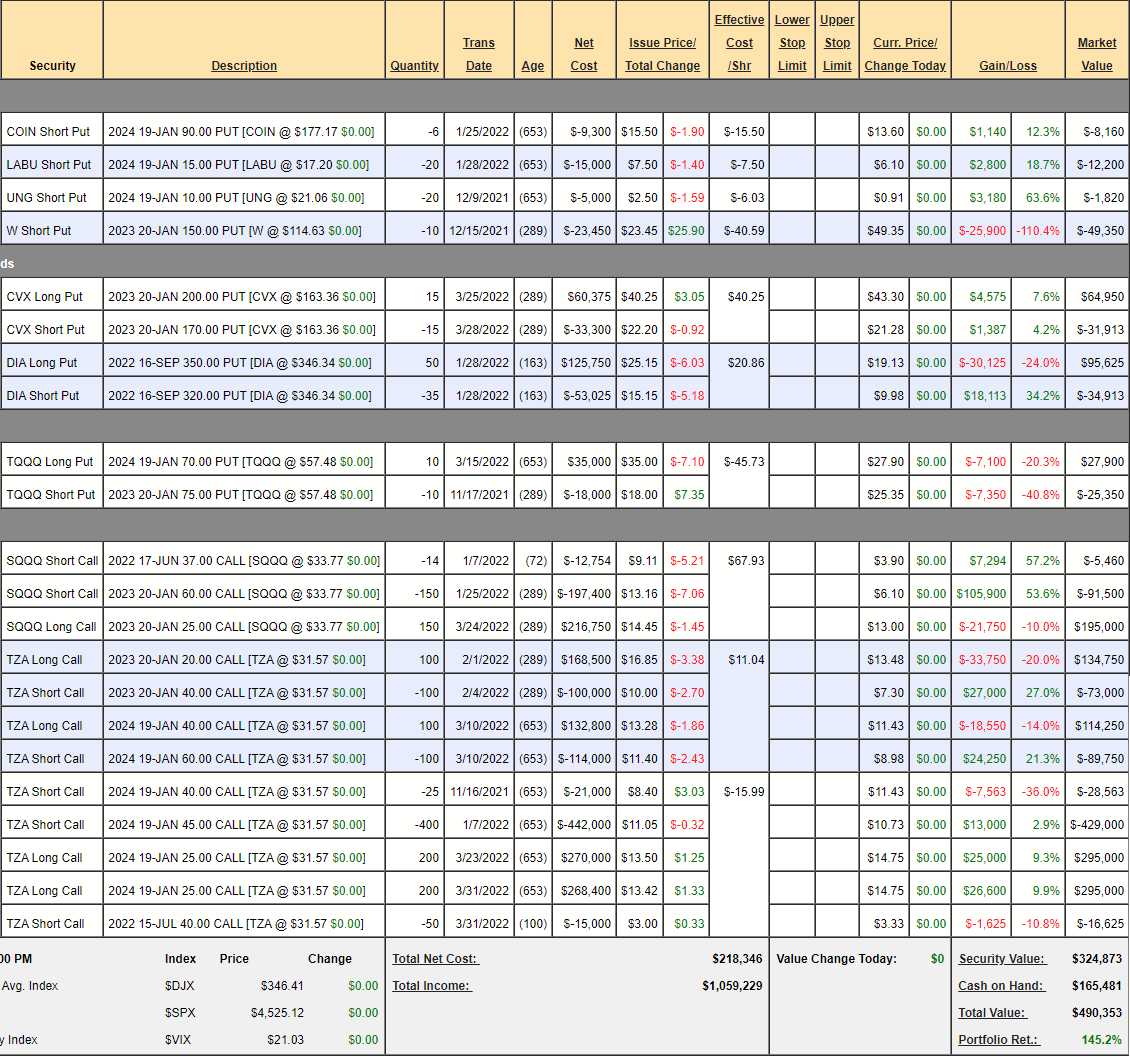

This is not to say we should ignore the weakness – just that we are very well-hedged from last Thursday's Short-Term Portfolio (STP) Review and I'd still rather keep the longs than dump them as – This too shall pass (hopefully). Meanwhile, our protection is working great and the STP is up $49,375 on this little dip:

The S&P 500 is down 120 points (2.6%) since last Thursday and our STP is supposed to give us $1.5M on a 20% correction but, of course, that's if things go down and stay down – we're not expecting an immediate pay-off. $50,000 is about right for 2.5% and if we pick up a quick $500,000 on a 20% drop and the rest comes over time – we can certainly work with that but we'll also be adding some more immediate pay-off hedges along the way if we fall back into our 20% correction zone – which we are once again skirting (see yesterday's Live Member Chat Room for my notes).

The S&P 500 is down 120 points (2.6%) since last Thursday and our STP is supposed to give us $1.5M on a 20% correction but, of course, that's if things go down and stay down – we're not expecting an immediate pay-off. $50,000 is about right for 2.5% and if we pick up a quick $500,000 on a 20% drop and the rest comes over time – we can certainly work with that but we'll also be adding some more immediate pay-off hedges along the way if we fall back into our 20% correction zone – which we are once again skirting (see yesterday's Live Member Chat Room for my notes).

Speaking of fun shorts. TSLA has gotten ridiculous again and I'm worried they won't make $1,200 so our short for the STP will be:

- Sell 2 TSLA July $1,200 calls for $87 ($17,400)

- Buy 5 TSLA Jan $1,000 puts for $175 ($87,500)

- Sell 5 TSLA Jan $900 puts for $128 ($64,000)

That's net $6,100 on the $50,000 spread so as long as we're under $1,200 – it's a very good risk/reward ratio with a potential upside of $43,900 (719%) if TSLA finishes the year below $900. We can also sell some short-term puts along the way – but not when they are this stupidly high.