Huge Battle Looms Over Public Pensions – Who Will (Who Should) Foot the Bill?

Courtesy of Mish

Public pension plans are $1 to $3 trillion underfunded. I think the number is closer to $3 trillion and destined to get worse. However, even $1 trillion is a massive problem.

With so much at stake, a Battle Looms Over Huge Costs of Public Pensions

There’s a class war coming to the world of government pensions. The haves are retirees who were once state or municipal workers. Their seemingly guaranteed and ever-escalating monthly pension benefits are breaking budgets nationwide.

The have-nots are taxpayers who don’t have generous pensions. Their 401(k)s or individual retirement accounts have taken a real beating in recent years and are not guaranteed. And soon, many of those people will be paying higher taxes or getting fewer state services as their states put more money aside to cover those pension checks.

At stake is at least $1 trillion. That’s trillion, with a “t,” as in titanic and terrifying.

Given how wrong past pension projections were, who should pay to fill the 13-figure financing gap?

Consider what’s going on in Colorado — and what is likely to unfold in other states and municipalities around the country. Earlier this year, in an act of rare political courage, a bipartisan coalition of state legislators passed a pension overhaul bill. Among other things, the bill reduced the raise that people who are already retired get in their pension checks each year.

This sort of thing just isn’t done. States have asked current workers to contribute more, tweaked the formula for future hires or banned them from the pension plan altogether. But this was apparently the first time that state legislators had forced current retirees to share the pain.

The state’s case turns, in part, on whether it is an “actuarial necessity” for the Legislature to make a change. To Meredith Williams, executive director of the Public Employees’ Retirement Association, the state’s pension fund, the answer is pretty simple. “If something didn’t change, we would have run out of money in the foreseeable future,” he said. “So no one would have been paid anything.”

Meanwhile, Gary R. Justus, a former teacher who is one of the lead plaintiffs in the case against the state, asks taxpayers in Colorado and elsewhere to consider an ethical question: Why is the state so quick to break its promises?

The changes the Legislature made don’t seem like much: there’s currently a 2 percent cap in retirees’ cost-of-living adjustment for their pension checks instead of the 3.5 percent raise that many of them received before.

Mr. Justus, 62, who taught math for 29 years in the Denver public schools, says he thinks it could cost him half a million dollars if he lives another 30 years. He also notes that just about all state workers in Colorado do not (and cannot) pay into Social Security, so the pension is all retirees have to live on unless they have other savings.

“All I can say is that I am sorry,” said Brandon Shaffer, a Democrat, the president of the Colorado State Senate, who helped lead the bipartisan coalition that pushed through the changes. I am tremendously sympathetic. But as a steward of the public trust, this is what we had to do to preserve the retirement fund.”

Private sector retirees who want their own monthly $2,883 check for life, complete with inflation adjustments, would need an immediate fixed annuity if they don’t have a pension. A 58-year-old male shopping for one from an A-rated insurance company would have to hand over a minimum of $860,000, according to Craig Hemke of Buyapension.com. A woman would need at least $928,000 because of her longer life expectancy.

Who among aspiring retirees has a nest egg that size, let alone people with the same moderate earning history as many state employees?

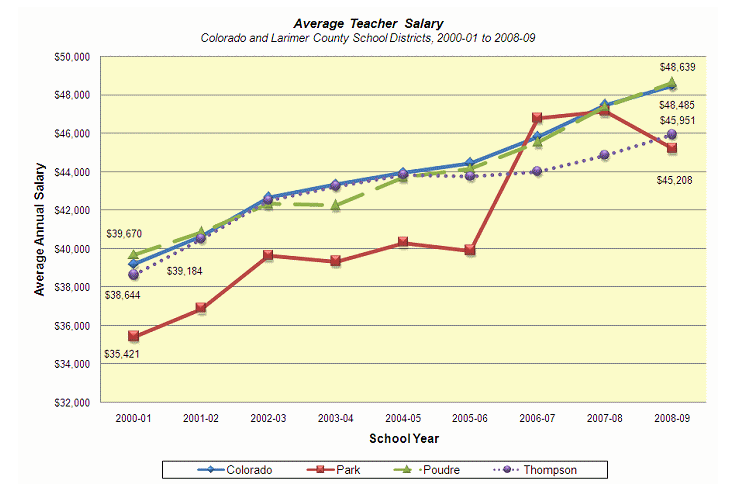

Teacher Salaries and Contributions

Colorado PERA (Public Employee Retirement Association) employees pay 8% of their salary into their retirement plan. Let’s take a look at what that means starting with this chart of Colorado teacher salaries.

Using the top line on the graph, wages hit $40,000 in about 2000. Bear in mind that does not factor in the fact that teachers get summers off, numerous holidays, and very generous medical benefits.

The chart does not go back as far as I like but let’s assume a teacher in 1980 was making $25,000 with an average salary of $38,000 over that 30 year period. 8% of $38,000 is $3040, or a bit more than $253 a month.

On that scale, a teacher working for 30 years put in about $91,200. Assuming an 8.5% return every year, at retirement, the person would have accumulated roughly $394,000. At a 6.5% rate of return the teacher would only have accumulated about $271,000.

6.5% or so is roughly the historic average.

PERA Employer Contribution Rates

In addition to the 8% put in by PERA employees, the employer (taxpayer) has been putting in 10%, with additions scaling up to 20% of salary to make up for underfunded pensions according to a table of PERA Employer Contribution Rates.

Taxpayers have paid through the nose for absurd teacher pension benefits and it still was not enough thanks to excessive benefits, absurd plan assumptions, and longevity (people live far longer).

Benefits

PERA Benefits are calculated using an average of the highest three salaries.

Someone working 30 years can retire as early as age 50 on 75% of their highest three salaries. In my example, I assumed a teacher started working at age 25. Other PERA employees can easily start out of high school and retire at 50.

Using that teacher salary chart, 75% of the 3 highest years salaries is about $36,000 a year for the rest of someone’s life.

From the New York Times article, a woman retiring at age 58 would need to have accumulated $928,000 for a payment of $2,883. In my example the person retired at age 55 and got $3,000 a month.

It if far worse yet because of the COLAs. The $928,000 annuity assumed fixed monthly payments, not payments that increase 3.5% or even 2% a year.

However, Gary R. Justus is bitching about the cutbacks in COLAs from 3.5% to 2%. They ought to be cut back to 0%. Private employees get no guaranteed adjustment in their 401Ks and they have to take 100% of the risks as well.

Finally, and as I have mentioned before, 8.5% pension assumptions are far too optimistic. Looking ahead 10 years, I think even 6.5% looking ahead is still far too optimistic and I would not be surprised one bit if 2.5% was too optimistic.

Stock market returns were negative for the past 10 years, why can’t they be small or negative for the next 10 years? Japan has proven it can happen.

Colorado vs. New Jersey

Colorado PERA employees put in 8%. In many cities and states, union member put in far less. Some police and fire fighters put in 2%.

For an apples-to apples comparison, please consider the State of New Jersey Teachers’ Pension and Annuity Fund

In New Jersey, the Member Contribution Rate is 5.5 percent of base salary. Base salary does not include overtime, bonuses, or large increases in compensation paid primarily in anticipation of retirement. Nor does it include additional salary for performing temporary or extracurricular duties beyond the regular school day or the regular school year. Your pension contributions are deducted from your salary each payday and reported to the TPAF by your employer.

New Jersey Teacher Salaries are a bit higher than Colorado but the teachers contribute far less. Assuming an average base salary of $42,000 over 30 years (I am sure that is on the high side), a New Jersey teacher working for 30 years contributed a mere $69,300 total, yet they expect a million dollars or more of lifetime pension benefits.

Is this nuts or what?

Who Should Pay for the Trillion-Dollar Pension Gap?

Inquiring minds are investigating attitudes regarding who is responsible for this mess. Please consider comments to the above article on Who Should Pay for the Trillion-Dollar Pension Gap?

Pedrson: Oregon – August 6th, 2010 – 3:03 pm

For years public employees worked for lower wages for 30 years with the promise of more job security and a promised retirement benefit that has always exceeded the private sector overall. Now many public wages have gone down or are frozen (exception federal government) and we the retirement benefits are what public employees still can count on, despite the economic decline. In most cases these employees when they retire will continue to pay state and federal taxes which will still benefit the economy. Seems like jealousy on the part of those who went after the bigger salaries early in their careers in the private sector and now regret their decisions.

Mish:

That is complete nonsense. Not only are public union workers overpaid relative to the private sector, the union members have the gall to bitch about it. Prison guards and bus drivers with no more than high school educations are walking away in some instances with pensions approaching $100,000. With police and firefighters in major cities, $100,000 or close to it is norm. By the way, education is in and of itself a meaningless argument. Jobs are worth what the free market says they are worth, not what someone with a useless degree in sociology, history, or English thinks they should be worth. The problem is public unions have nothing to do with a free market.

Terry Podmore: Fort Collins CO – August 6th, 2010 5:45 pm

I am a recent retiree of Colorado PERA, having served 30 years as a faculty member at Colorado State University. What the state has done is a travesty to all existing retirees, having broken the promises of retirement security. As an individual, you make the best decisions you can based on the conditions prevailing. To have these conditions changed after the fact puts all current retirees at risk at a time of life where there are few options.

Mish:

Terry’s attitude is typical of the attitude of those who could not or would not consider the risks of what they were doing. It is not the fault of taxpayers if the faculty at Colorado State University is not bright enough to figure out the system is unsustainable. Besides, did Terry take the job because that is what he wanted to do, or because of benefits? Either way, Terry has no complaint. In one case Terry would have done the job anyway, in another case he was not bright enough to figure out what was happening. Taxpayers have no responsibility to bail out people who cannot think.

Melissa: Chicago, IL – August 6th, 2010 – 3:44 pm

I’m still trying to figure out how anyone ever thought that allowing someone else besides themselves handle their retirement would be a good idea.

Mish:

Melissa is one of the few who gets it. Melissa has more on the ball than at least one 30-year faculty member of Colorado State University.

JRTC3: Upstate, NY – August 6th, 2010 – 4:28 pm

I am a retired member of the New York State Teacher’s Retirement System. The money that I receive monthly is not a gift from the state or the taxpayers. It is money that I earned in my thirty years of service. It seems to me that taking that away from me would be stealing. That is wrong.

Mish:

No JR, you are mistaken. The money is a gift, and you did not do a single thing to earn it. Instead you joined a union ….

1. A union that got into bed with corrupt politicians

2. A union that stacked the school boards who fought for property tax hikes after property tax hikes – not for the kids – but to pad your greedy pocket

3. A union that threatened politicians if you did not get your way

4. A union that protects incompetent teachers from dismissal, even sexual predators who now sit in "black rooms" at full pay for doing nothing

5. A union that is supposed to consist of public servants but whose only concern is serving itself

Bribery, fraud, extortion, and coercion are the tactics of unions. Agreements "won" by such methods were not in any conceivable manner "earned". The amount of money you put in towards your retirement is peanuts compared to your benefits. All you really earned is what you put in (minus any accrued benefits won by bribing politicians).

Taxpayer money goes to union dues which in turn is used to elect corrupt politicians who are willing to suck every last drop of taxpayer blood just so they can get elected. Quite frankly the setup is disgusting.

Yes JR, you earned something alright: taxpayer contempt, for stealing taxpayer money.

Peter: New York – August 6th, 2010 – 5:40 pm

The deal that public unions have is fundamentally corrupt. Politicians playing with taxpayers’ money promising never ending employment, wage increases regardless of performance and ever improving benefits. Why? To get political contributions from the unions and votes from the members who have permanent job security.

Mish:

Peter certainly gets it

Linda C: San Francisco – August 6th, 2010 – 5:41 pm

Younger workers absolutely should NOT be responsible for the fiscal mismanagement and over-entitlement of previous generations.

Mish:

BINGO. Neither younger workers nor taxpayers on general should have to foot the bill for absurd promises that anyone with an ounce of common sense knew could not be met. If the public unions workers were too stupid or too greedy to figure that out and act on it, it should be their problem, and their problem alone to fix it.

The solution for cities is bankruptcy. If unions will not agree to major changes, then union members can see what their plan looks like after bankruptcy. States cannot declare bankruptcy, however, they can and should default if unions do not agree to major concessions.