{kind=link}

What's it going to take to stop the bleeding?

What's it going to take to stop the bleeding?

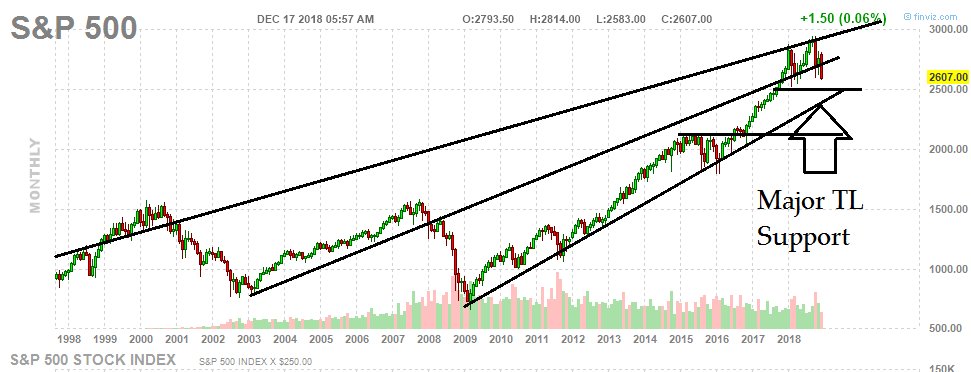

NOW we have a bit of a correction going on as the S&P 500 closes the week at 2,600, more than 10% off the 2,940 high it posted in September, when Shanghai stocks were already down 20% and we were ignoring them and I said:

When people tell you that what happens to the second largest economy in the World doesn't effect the largest economy in the World, those people are idiots and you should never listen to anything they say to you – ever again. Jamie Dimon of JP Morgan, for his part, is doing his best to minimize the concerns of retail investors so he can keep dumping stocks on them:

"If you look at tariffs on $200 billion (worth of Chinese goods), and this may all get passed on to American consumers and they have to pay another $20 billion (on Chinese imports), it's a $20 trillion economy, so the actual economic effect is not dramatic," Dimon said.

"We can add tariffs to more things and the Chinese can retaliate in other ways and I don't think all that's good. It's not a devastating thing, it's not a war, it's a trade skirmish that can have negative economic effects."

Dimon is not going to say what happens in China has no effect but he's mimizing the impact and misleading traders by using the 10% figure that costs $20Bn but that 10% tariff escalates to 25% at the end of the year ($50Bn) and then Trump plans to double the number of goods that are taxed ($100Bn) so a smart reporter would ask Dimon – does $100Bn matter then?

You can nod your head and agree with Dimon (after all, he's a rich guy, so he must know stuff and he would never lie to you, right?) because $20Bn is only 0.1% of our GDP, though that's still enough to knock growth down from 4% to 3.9%. $100Bn, on the other hand, is 0.5% of our entire GDP – it's really kind of hard to find any justifcation to minimize the impact of that other than – "Because I'm an investment banker and my wealthy clients need greater fools to sell their ridiculously over-priced equities too."

This is what "THEY" do to retail investors at the tail end of the rally, they herd all the sheeple into the markets at the WORST possible time, cranking up the propaganda machine and doing whatever it takes to pretty up the indexes to draw as many people as they can into the markets – providing fresh buyers so they can cash out of the stuff they bought when they were telling consumers to stay out of equities.

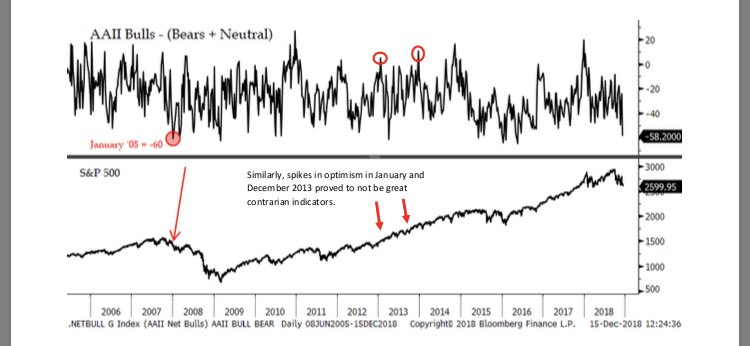

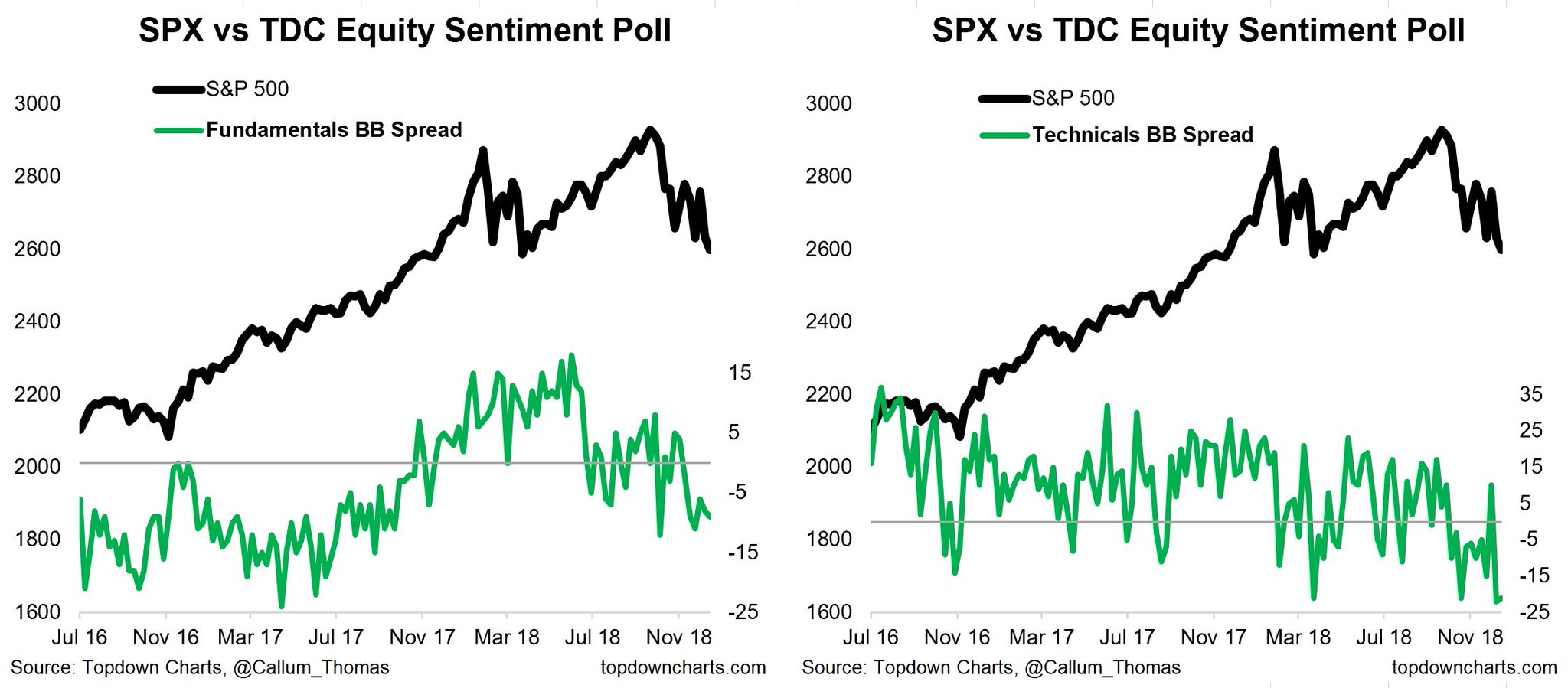

It didn't take long for us to see the effects of those initial tariffs begin to wreck havoc with the Global Economy and now the sentiment has turned completely negative, lower now than it was in 2007, before the great crash so I think we have to move forward very carefully here and that's what we did last week with our Portfolio Reviews – resisting the temptation to BUYBUYBUY at the "bottom" until we can get a bit more evidence confirming that this is, indeed, the bottom.

At the moment, the Fundamentals are ugly and the technicals are ugly and Trump is still President and it's anybody's guess which of those 3 conditions is cured first. For now, we're simply continuing last week's slide lower and there haven't been any more BS trade announcements or Fed predictions to tip the scales bullish and Monday volume is notoriously low (and meaningless) so we'll simply have to sit back and see if the 1,400 line holds on the Russell (/TF) but, if it doesn't – we could be looking at a test of the 10% line on the Dow (/YM) at 23,100 and that's still 750 points down from here so a cross below 23,850 could give us a short play (with tight stops above) that pays $3,750 per contract!

Of course, I've said this before, our call to short the Nasdaq (/NQ) below 7,000 has been good for over 400 points, which is $8,000 per contract and our call to short the S&P (/ES) below 2,800 has been good for over 300 points and that's a whopping $15,000 per contract on that index. Using the futures to enhance our hedges is a very good way to stay balanced if we're not sure it's time to add more hedges – yet.

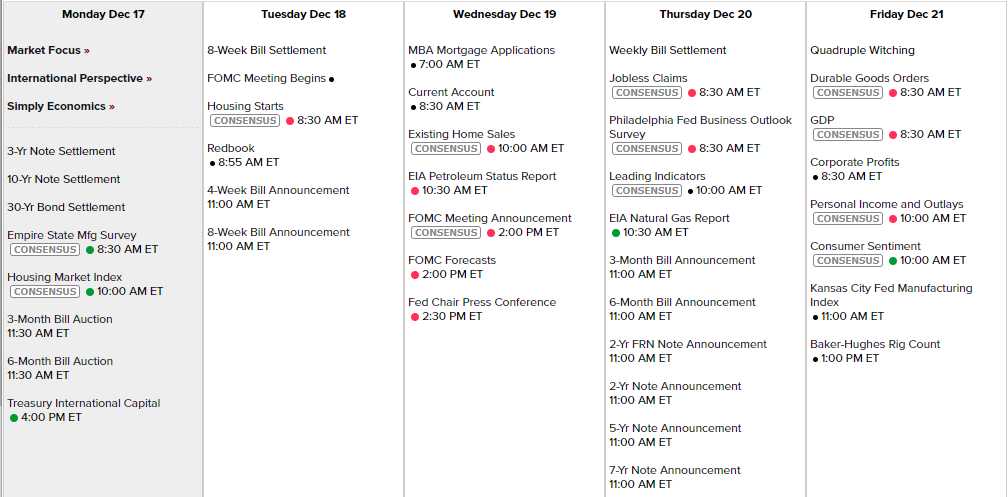

The Fed will be silent this week other than Powell's press conference on Wednesday after what is now a toss-up meeting as to whether or not the Fed hikes rates. I was leaning they would but, if the markets stay this low – I doubt they have the balls to do what's needed to stabilize things as lower and stable would be better than boosted and shakey.

Other than that, we have GDP Friday and a few Fed Reports scattered through the week but nothing more market-moving than the Fed Announcement itself on Wednesday so, until then, "nothing really matters…."